[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories increased 1.4 MMBbl last week, according to the weekly EIA report. Gasoline inventories increased 1.8 MMBbl while distillate inventories decreased 1.0 MMBbl. Total petroleum inventories posted a decrease of 5.0 MMBbl. US crude oil production was flat to the previous week, per EIA, while crude oil imports were up 0.22 MMBbl/d to an average of 6.0 MMBbl/d.

- WTI prices had little additional news during the week with the market starting the week lower on skepticism over whether OPEC and allied non-OPEC producers will be able to agree on additional cuts next week. Rumors in the market later in the week suggested that OPEC+ would extend the cuts into 2020. However, it is still not confirmed whether Russia’s participation in the cuts will occur.

- The roller coaster ride associated with the US and China “phase 1” tariff deal continued to push the market around. The discussions last week seemed to hit a wall with President Trump refusing to lift existing tariffs on Chinese goods and the Chinese expecting those reductions. It is unclear how driven the Chinese are to cut a deal with the ongoing impeachment issues in Washington and the potential effects on the relationship.

- The CFTC report released Friday (dated November 19) showed a small shift in the speculative community, with the Managed Money long sector dropping 13,204 contracts and the Managed Money short position adding 12,245 contracts. This action was likely a result of the December contract expiration on Wednesday, the day after the positions report.

- Market internals last week were neutral with a slightly bullish bias, with prices rebounding up at the end of the week on rising open interest but declining volume during the expiration process. The high range at $58.74 was met with selling, while support found buyers at the recent low end of the range ($54.76). Prices have traded around the commonly traded 200-day moving average ($57.42 on Friday) for the past two weeks. The inability of the market to extend the gains or losses beyond this average for a period of time is likely why the speculative sector is not significantly shifting positions.

- Similar to last week, rallies will challenge the highs from September between $58.49 and $59.39. Should the tariff stalemate continue this week, it’s likely prices will test the low end of the range at $55.

NATURAL GAS

- Natural gas dry production increased 0.32 Bcf/d last week, while Canadian imports decreased 0.79 Bcf/d.

- Res/Com demand decreased 7.46 Bcf/d, as temperatures moderated from the previous week. Power and Industrial demand decreased 2.12 Bcf/d and 0.96 Bcf/d, respectively. LNG exports gained 0.52 Bcf/d, while Mexican exports decreased 0.14 Bcf/d.

- These events for the week have the market decreasing 0.47 Bcf/d in total supply while total demand decreased by 10.48 Bcf/d.

- The storage report last week showed the first withdrawal of the season with a draw of 94 Bcf. Total inventories are now 506 Bcf higher than last year and 60 Bcf below the five-year average. The current weather forecasts from NOAA in the near term (coming week) show below-average temperatures from the West through the Northern Plains to the Northeast. The 8- to 14-day forecast has below-average temperatures throughout the northern half of the US, with no above-normal zones.

- The CFTC report released last week (dated November 19) provides an interesting element to upcoming trade as prices fell at the beginning of the week. The Managed Money short position took advantage of the declines by adding 41,816 contracts as prices tested the support at $2.50. The Managed Money long positions sold off 8,831 contracts with the declines. The speculative short position is extending positions to levels that may induce a covering rally similar to what happened earlier this month.

- The market internals developed a more neutral bias as prices rallied off of support on higher open interest but lower volume.

- Prices have defined the area at the island gap ($2.724), which will continue to find sellers on challenges. With expiration coming this Tuesday, it is likely that the gap will hold as a cap during expiration, regardless of the bullish history of expirations. For the past two-plus years, the expiration process has provided some sort of rally during the process. On the bearish side, the behavior last week challenged the major area of support (around $2.50). That area is likely to hold declines during expiration.

NATURAL GAS LIQUIDS

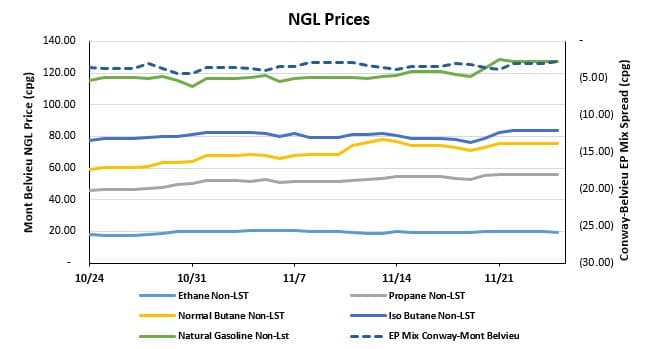

- NGL price movements were mostly up last week, with the exception of butane. Ethane was up 2.5% to average $0.198/gal for the week, propane gained 1.6% to average $0.546/gal, and natural gasoline increased by 4.1% to average $1.23/gal. In contrast, normal butane averaged $0.735/gal compared to $0.760/gal the week before (down 3.3%) and isobutane lost 1.2% to average $0.798/gal.

- Propane has remained supported due to increased demand for residential heating and late-season crop drying, but pre-holiday buying likely also played a role with last week’s price increases. Despite being down on average for the week, normal butane also clawed back most of its losses by the end of trading on Friday. Tight supply and increases in Asian prices were the key drivers behind the rebound.

- The EIA reported a large draw in propane/propylene stocks of nearly 3.5 MMBbl last week, which came on the back of another large stock draw reported the week before. Stocks now stand at 94.2 MMBbl, which is roughly 12 MMBbl higher than the same week in 2018 and 20 MMBbl higher than the same week in 2017.

SHIPPING

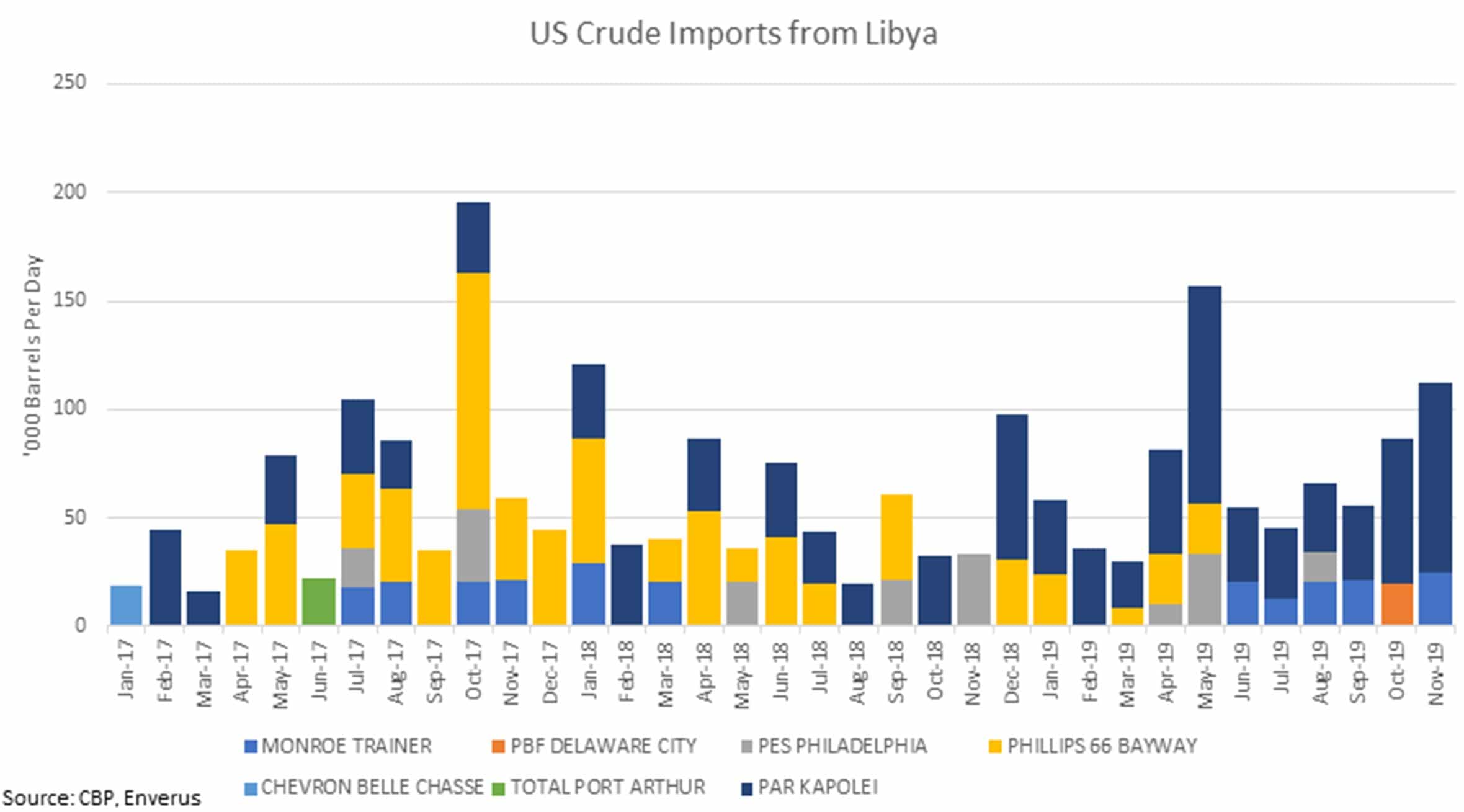

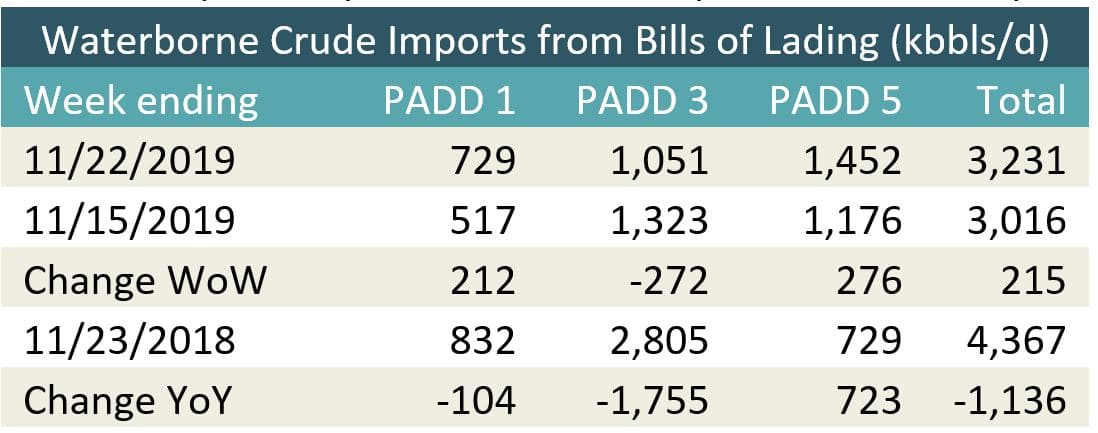

- US waterborne imports of crude oil rose for the week ending November 22, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of November 25, aggregated data from customs manifests suggests that overall waterborne imports increased by 215 MBbl/d from the previous week. The increase was driven by higher imports to PADDs 1 and 5, which rose 212 MBbl/d and 276 MBbl/d, respectively. PADD 3 crude imports fell, down 272 MBbl/d.

- PADD 5 imports of Libyan crude oil have been strong this month and are on pace to be the second highest since at least 2017. The highest month for PADD 5 imports of Libyan crude oil was May 2019. All of these barrels have been destined for the Par Refinery in Kapolei, Hawaii. Libya produces mostly light, sweet grades, and all of the barrels imported so far this month have been Mesla Sarir, a light, sweet grade. The increasing imports of Libyan crude could face some competition as the refinery has recently received a cargo of US crude from the Jones Act tanker Houston. This tanker should deliver barrels to the refinery for the next several years.