[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories increased by 7.9 MMBbl last week, according to the weekly EIA report. Gasoline and distillate inventories decreased 2.8 MMBbl and 0.6 MMBbl, respectively. Total petroleum inventories posted an increase of 3.9 MMBbl, generated primarily by the crude build. US crude oil production was unchanged from the previous week, per EIA, while crude oil imports were down 0.62 MMBbl/d to an average of 6.1 MMBbl/d.

- WTI prices extended the gains from the previous Friday, showing some strength early in the week on continued optimism from the US economy, the expected confirmation of a Phase 1 deal between the US and China in the tariff disputes, and the upcoming OPEC+ meeting coming in early December. Prices also got support from the third-quarter earnings reports from the US E&P companies, which have been pointing toward lower capex plans in the coming year.

- Over-supply concerns continue as the OPEC World Oil Outlook report provided a grim forecast of non-OPEC production (led by the US) outstripping demand over the next five years. The upcoming IEA World Energy Outlook (scheduled release November 13) should shed more light on the upcoming supply and demand situation in 2020.

- The optimism early in the week was muted by the inventory release on Wednesday with the large gains in crude. This capped the gains from early in the week, but prices recovered most of the declines by the end of trade on Friday, in spite of the bullish recovery of the US dollar during the week.

- Internal price relationships continue to show the prompt month maintaining a significant premium to the 2020 strip, confirming concerns regarding the supply and demand balance in the future.

- The CFTC report released Friday (dated November 5) showed a support in the movement between the speculative expectations, with the Managed Money long sector increasing positions by 9,335 contracts, while the Managed Money short positions reduced by 9,414 contracts. This provided enough buying to maintain the strength early in the week.

- Market internals last week brought a neutral with a slightly bullish bias, with prices closing up on the week with higher volume and gains in open interest.

- Prices continued in the recent range between $53 and $57 while expanding the higher end of the range. Further extensions of support will take prices above the commonly traded 200-day moving average ($57.24 today), and a breakout above that level on a daily closing basis will send prices toward the highs from September between $58.49 and $59.39. It was this moving average zone that limited last week’s gains and where sellers were found. Bearish input from concerns about the global economy or hold-ups in the US/China trade deal could bring another test at the low end of the range at $53, which will likely find buyers.

NATURAL GAS

- Natural gas dry production increased 0.07 Bcf/d last week as production came back from the weather-related issues. Canadian imports increased 0.12 Bcf/d on the week.

- Res/Com demand increased 6.04 Bcf/d, while power demand decreased 1.33 Bcf/d and Industrial demand increased 0.56 Bcf/d. LNG exports declined 0.39 Bcf/d, while Mexican exports decreased 0.03 Bcf/d on the week.

- These events left the totals for the week with the market gaining 0.20 Bcf/d in total supply while total demand increased by 5.09 Bcf/d.

- The storage report last week showed the injections for the previous week at 34 Bcf. Total inventories are now 530 Bcf higher than last year and 29 Bcf above the five-year average. Current weather forecasts from NOAA in the near term (coming week) have below-average temperatures from the Midwest to the East, including eastern portions of Texas, with above-average temperatures in the West. The 8- to 14-day forecast shows warmer temperatures from the central Midwest and the Eastern Seaboard with normal temperatures in the Mississippi Valley.

- The CFTC report released last week (dated November 5) showed a continuation of the short covering process by the Managed Money short position, as positions were reduced by 72,718 contracts, while Managed Money long positions increased by 10,777 contracts.

- The market internals now have a neutral to slightly negative bias as prices rallied to a new high (only to correct lower) on higher volume, but open interest and remained relatively flat for the week. The week ended just about where it started; after trading to a new high, it is not bullish.

- The extension of the previous week’s advances sent prices to the highest level since the end of February ($2.905). From that advance there was a steady amount of selling, and with the large gap opening today ($2.755-$2.716) offsetting the large gap last Monday, the trade has developed an “island top” for traders to consider. With the flip in the weather forecasts, declines between $2.575 and $2.52 should occur in the coming weeks. Any reversals stronger than that will run into sellers at the gap formed today between $2.716 and $2.755.

NATURAL GAS LIQUIDS

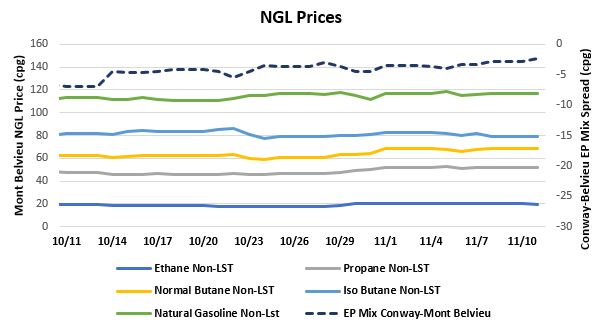

- NGL prices were up week-over-week. Ethane was up $0.010 to $0.203, propane up $0.023 to $0.516, normal butane up $0.038 to $0.679, isobutane up $0.007 to $0.813, and natural gasoline up $0.012 to $1.167.

- US propane stocks gained ~320 MBbl for the week ending November 1. Stocks now sit at 100.17 MMBbl, roughly 15.64 MMBbl and 22.97 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

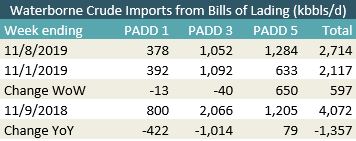

- US waterborne imports of crude oil rose for the week ending November 8, 2019, according to Enverus’ analysis of manifests from US Customs & Border Patrol. As of November 11, aggregated data from customs manifests suggested that overall waterborne imports increased by nearly 600 MBbl/d from the previous week. The increase was driven by higher imports into PADD 5, which were up 650 MBbl/d from the prior week. PADD 1 and PADD 3 both fell slightly, down 13 MBbl/d and 40 MBbl/d, respectively.

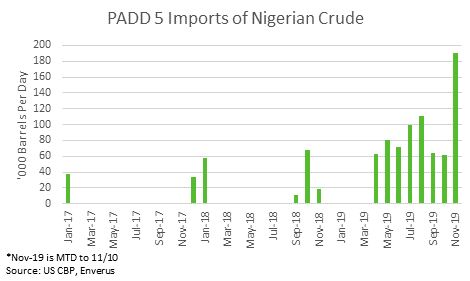

- West Coast imports of Nigerian crude have been strong in 2019, averaging more than 60 MBbl/d ytd. The highest month so far was August, when imports were over 110 MBbl/d. November looks like it will be a strong month as well, with imports over the first 10 days nearing the monthly totals for September and October, closing in on 2 MMBbl for the month. On a per-day basis, they are at 190 MBbl/d. This has been roughly split between Erha and Bonga grades, both medium sweets. The Bonga cargo appears to have been taken by Marathon’s Carson refinery while the Erha was split between Phillips 66 Los Angeles and Phillips 66 Ferndale. Vessel tracking data analyzed by Enverus shows that this might be the last Nigerian cargo received on the West Coast this month. The next tanker from Nigeria headed to the West Coast appears to be the Pentathlon, a suezmax capable of holding 1 MMBbl of crude, which departed the Agbami terminal 18 days ago and is showing an ETA to Richmond, CA, of December 1, 2019. Chevron took the last cargo of Agbami to Richmond in late June.