[contextly_auto_sidebar]

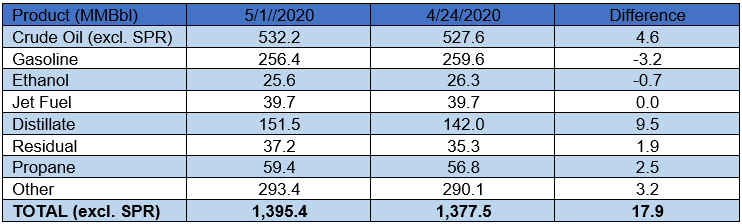

US crude oil stocks posted an increase of 4.6 MMBbl. Gasoline inventories decreased by 3.2 MMBbl and distillate inventories increased by 9.5 MMBbl. Yesterday afternoon, API reported a crude oil build of 8.4 MMBbl alongside a gasoline draw of 2.2 MMBbl and a distillate build of 6.1 MMBbl. Analysts were expecting a crude oil build of 8.1 MMBbl. Total petroleum inventories posted an increase of 17.9 MMBbl.

US crude oil production decreased by 200 MBbl/d, per EIA. Crude oil imports were up 0.41 MMBbl/d last week, to an average of 5.7 MMBbl/d. Refinery inputs averaged 13.0 MMBbl/d (0.22 MMBbl/d more than last week’s average).

Crude oil prices continued its five-day rally through to yesterday’s close, with the June WTI contract settling at $24.56/Bbl. Futures have since trended lower in early morning trading. Nevertheless, further easing of the prompt contango structure is a promising sign that OPEC+ production cuts, shut-ins, and firming demand conditions are doing their part to rebalance the market. The slowing pace of commercial crude oil inventory builds in the United States is indicative of this, but there is still a lot of work to be done on the demand side of the balance before anyone can say with confidence that the market is completely out of the woods. As today’s EIA report shows, refiners could end up swelling product inventories if they ramp up crude runs faster than end-use demand is able to recover. While most of the oversupply focus to-date has been on gasoline and jet, the reported 9.5 MMBbl build in distillates raises concerns about broader macroeconomic weakness.