[contextly_auto_sidebar]

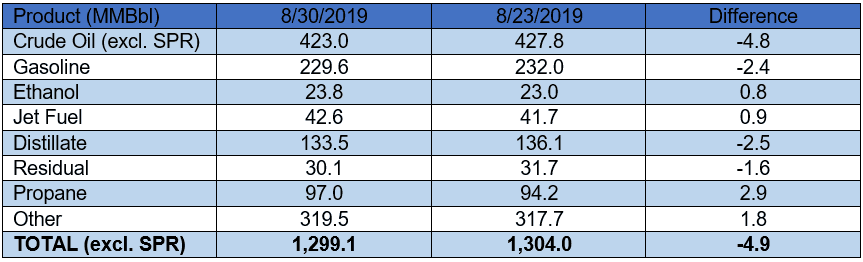

US crude oil stocks posted a decrease of 4.8 MMBbl from last week. Gasoline and distillate inventories decreased by 2.4 MMBbl and 2.5 MMBbl, respectively. Yesterday afternoon, API reported a crude oil build of 0.4 MMBbl, while reporting gasoline and distillate draws of 0.88 MMBbl and 1.2 MMBbl, respectively. Analysts, to the contrary, were expecting a crude oil draw of 3.5 MMBbl. The most important number to keep an eye on, total petroleum inventories, posted a decrease of 4.9 MMBbl. For a summary of the crude oil and petroleum product stock movements, see the table below.

US crude oil production decreased 100 MBbl/d last week, per the EIA. Crude oil imports were up 0.9 MMBbl/d last week, to an average of 6.9 MMBbl/d. Refinery inputs averaged 17.4 MMBbl/d (27 MBbl/d less than last week’s average), leading to a utilization rate of 94.8%. Prices extend gains due to larger than expected crude draw and total petroleum stocks withdrawal. Prompt-month WTI was trading up $1.18/Bbl, at $57.44/Bbl, at the time of writing.

Prices had a busy week and continued their volatility as the market kept its focus on the developments and news regarding the US-China trade tensions, global economic health and data, and eroding crude demand led by a weakening economic growth. Prices bounced up to their highest of the week last Thursday, only to give up most of their gains before the long weekend due to strengthening of the US dollar. The decline in prices continued as crude futures sank more than 2% on Tuesday, due to the US starting to impose 15% tariffs on some Chinese imports Sunday, while China began placing new duties on US crude oil. Also supporting bearish sentiment and bringing prices down was the US manufacturing data showing activity in August falling for the first time in three years and the lingering fears about a global recession.

Although the overall gloomy economic outlook and the ongoing trade war between the world’s largest economies still persists, the positive news from China’s services sector caused a surge in prices on Wednesday. Oil prices rose more than 4% on Wednesday along with global markets after a private survey showed that activity in China’s services sector grew at the fastest pace in three months in August. Also supporting prices was a possible sign of easing tensions from the Middle East, as Iran stated that Tehran would free seven crew members from the detained British-flagged tanker that was seized by Iran in retaliation for Britain’s previous detention of an Iranian tanker.

Despite the brief support provided by positive news from China’s services sector, the overall global economic outlook remains dim and troublesome as the trade tension between the US and China continues to linger and progressively worsen due to tit-for-tat tariffs imposed by both countries. The supply side unfortunately does not provide too much support to prices either, despite the historical low productions from Iran and Venezuela and the OPEC+ countries’ continuing efforts to reduce supply. OPEC is set to meet on September 12 in Abu Dhabi. Although the market is very much focused on the impact of the US-China trade war on the economy and oil demand, developments from this meeting will be closely watched, as the IEA has already given signals that without further supply reductions, an oil supply glut could resurface again in 2020.

The recent range between $53.00 and $58.00 may hold in the coming week without developments in the US and China trade war, while the long-term range between $50.00 and $61.00 will likely hold without similar developments. China’s attempt to bring tariffs on US crude imports may indicate a shift to utilize Iranian imports. Prices would be pressured if Iran were to increase output because of demand from China or a nuclear deal with France. The market will trade around the news event or Twitter feeds in the coming week, but also will keep an eye out for any news regarding supply cuts from the OPEC meeting.