Calgary, Alberta (July 23, 2025) — Enverus Intelligence Research (EIR), a subsidiary of Enverus, the most trusted energy-dedicated SaaS company that leverages generative AI across its solutions, is releasing its summary of 2Q2025 upstream M&A activity and outlook for the rest of the year.

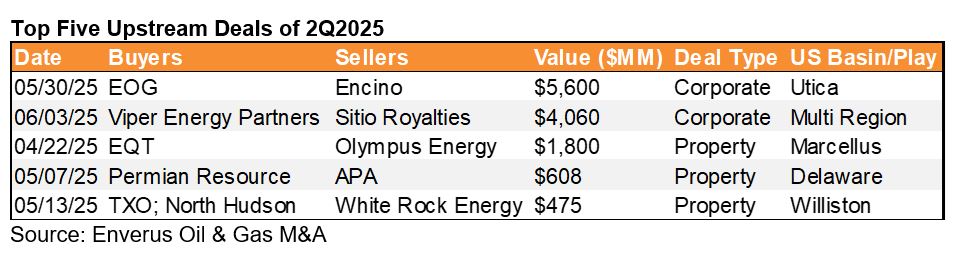

Upstream M&A decelerated in the second quarter of 2025, with value falling 21% quarter-over-quarter to $13.5 billion. That is the second lowest quarterly deal value since the start of 2024 and placed 1H25 M&A value at $30.5 billion, a 60% drop compared to the first half of 2024. Value was heavily driven by just two large transactions – EOG’s purchase of Encino Acquisition Partners in the Utica and Viper Energy Partners rare public mineral merger with Sitio Royalties. Combined, these two transactions accounted for over 75% of second quarter deal value. The lack of breadth in deal markets was reflected in the count of transactions over $100 million with just eight deals topping that benchmark, a tie for the lowest total since 2020.

“Volatility in commodity and equity markets raised a major yellow flag for M&A, slowing the pace of dealmaking,” commented Andrew Dittmar, principal analyst at EIR. “That added an additional barrier to a market that was already challenged by the lack of remaining attractive opportunities for public E&Ps, especially in the Perman Basin. The engine of M&A over the last few years has sputtered and stalled, given there are just a few remaining targets and, outside the rare opportunity like APA’s deal with Permian Resources, it is not a region public companies are likely to pick for non-core asset sales.”

With the Permian and other major unconventional plays increasingly locked down by large public operators, buyers are taking more creative maneuvers to secure undeveloped inventory. EOG supercharged its exposure to the Utica liquids window, adding it as a third pillar of the company’s business along with the Delaware Basin and Eagle Ford. Its acquisition of Encino for $5.6 billion cemented EOG’s frontrunning position in the liquids play. Encino, backed by the Canada Pension Plan Investment Board, held the most remaining liquids-focused remaining inventory among non-family private E&Ps. EOG also added substantial exposure to the gas window of the Utica with the acquisition.

“After having a Permian-centric market for the last few years, the race to add economic locations is pushing buyers into a more geographically diverse set of deals,” said Dittmar. “The challenge for larger public operators is that only a few of the emerging regions, like the Utica and Uinta, offer the scale of resource they need. While companies have so far been reluctant to look outside the U.S., eventually that will likely need to include assets in Canada or other international areas like Argentina’s Vaca Muerta.”

While public companies contend with the lack of remaining attractive private acquisition targets, private equity firms themselves are looking to refuel portfolios following a frenetic pace of exits over the last few years. In contrast to public operators, private capital has more flexibility in the types of deals and assets pursued as well as not needing the same scale as public companies. Some are returning to the Permian Basin, where firms have clocked many of their biggest wins, picking up small assets or focusing on extensional areas not yet consolidated by large operators. However, the biggest opportunities are likely to be in areas off the radar of public companies. The SCOOP | STACK in Oklahoma is one such region where public companies are more likely to be sellers than buyers and a key candidate for non-core asset sales by the large buyers of the last few years like ConocoPhillips. Private firms may also look at secondary plays including other parts of the Permian like the Central Basin Platform or the older Rockies regions like the Piceance and San Juan basins.

“Recharging portfolio companies is going to be more challenging for private firms as well, particularly those that want to pursue a resource delineation strategy that often generates the highest returns,” said Dittmar. “The basic challenge for many buyers in the U.S. whether public or private is that there is too much existing production and not enough remaining inventory. That changes acquisition strategies and expected returns on deals.”

For a few types of buyers though, the opportunity set in the market is expanding rather than shrinking. Those would be groups and companies that primarily target production-heavy assets like upstream master limited partnerships (MLPs). Mach Natural Resources and TXO Partners, both upstream MLPs, have been active consolidators of mature assets. TXO teamed up with North Hudson to acquire Williston assets from White Rock Energy for $475 million during the second quarter while Mach announced $1.3 billion worth of deals early in 3Q, adding assets in the San Juan Basin and Central Basin Platform. The TXO deal was particularly interesting because the company plans to focus on redevelopment or “refrac” opportunities on the legacy wells. “Redevelopment to extend the life of existing production is one of the more important emerging stories in the industry,” said Dittmar. “You are going to see that considered more frequently when evaluating acquisition opportunities.”

Another buyer group that may not mind production-heavy assets are international firms looking to gain exposure to U.S. hydrocarbons. Asia-based companies with LNG import commitments are an emerging force for buying Gulf Coast area gas assets. These firms may not mind a large base of existing production that lessens development risk. The combination of accelerating international interest in gas linked to Gulf Coast LNG plus emerging datacenter demand in Appalachia has the potential to rev up gas M&A. “While gas E&Ps don’t have the same urgency to add inventory as their oil-focused counterparts, companies are still willing to undertake financially accretive deals with clear operational synergies,” said Dittmar. “EQT is one example, buying Olympus Energy for $1.8 billion in a deal that boosted shareholder return metrics and allowed it to tie more of its southwestern Pennsylvania asset base into an emerging datacenter and industrial corridor outside Pittsburgh.”

One type of deal that has been notably absent this year is public company consolidation, a key component of the market in 2023 and 2024. The one exception is Viper’s merger with Sitio, which was also just the second major public company merger Enverus has tracked in the relatively niche mineral and royalty market. Viper, which has emerged as the most active consolidator of Permian royalties, was able to leverage its premium valuation to strike a financially accretive deal for Sitio. “The case for continued corporate consolidation is sound,” said Dittmar. “These types of deals should be easier to negotiate in a volatile environment given they are generally stock-for-stock swaps that limit commodity price risk, and the valuations on some public names are compelling for a buyer. The most obvious and willing sellers just got taken out earlier in the consolidation cycle, and it’s going to take some time for more companies to come to the table.”

You must be an Enverus Intelligence® subscriber to access this report.

About Enverus Intelligence Research

Enverus Intelligence ® | Research, Inc. (EIR) is a subsidiary of Enverus that publishes energy-sector research focused on the oil, natural gas, power and renewable industries. EIR publishes reports including asset and company valuations, resource assessments, technical evaluations and macro-economic forecasts; and helps make intelligent connections for energy industry participants, service companies and capital providers worldwide. EIR is registered with the U.S. Securities and Exchange Commission as a foreign investment adviser. Enverus is the most trusted, energy-dedicated SaaS company, with a platform built to create value from generative AI, offering real-time access to analytics, insights and benchmark cost and revenue data sourced from our partnerships to 95% of U.S. energy producers, and more than 40,000 suppliers. Learn more at Enverus.com.