CALGARY, Alberta (May 2, 2023) — Enverus Intelligence Research (EIR), a subsidiary of Enverus, the most trusted energy-dedicated SaaS platform, is releasing its summary of 1Q23 upstream merger and acquisition (M&A) activity. In Q1, U.S. upstream M&A saw $8.6 billion transacted in 16 deals, with more than $5 billion in the Eagle Ford for a surprising resurgence in that mature play. While deal value is down about 20% versus the first quarter average since 2016, deal volume also continued its multi-year collapse with a disclosed volume of 80% less than the Q1 average. That resulted in an average deal size of more than $500 million.

“Last quarter was an outlier in terms of the deal targets and types for upstream transactions,” said Andrew Dittmar, director at Enverus. “Rather than public E&Ps focusing on buying undeveloped inventory in the Permian Basin from private companies, most of the deals targeted mature assets in the Eagle Ford and included more public-to-private transactions plus a corporate merger.”

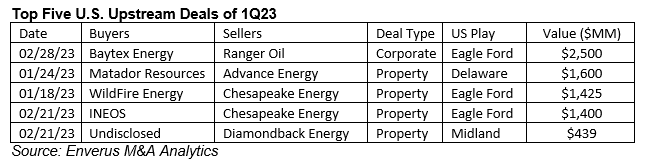

Leading off for deal size was the acquisition of Houston-headquartered Eagle Ford pure-play Ranger Oil by Calgary-based Baytex Energy. This deal, the first merger involving a U.S. operator E&P since Oasis Petroleum and Whiting Petroleum combined one year ago, brought Baytex into the Eagle Ford. Baytex was the second new entrant to buy its way into the Eagle Ford (and the second from outside the U.S.), as U.K.-based INEOS also made its debut as a North America shale operator with its purchase of Chesapeake’s South Texas assets for $1.4 billion.

“The Eagle Ford has a lack of home-grown consolidators and has remained fragmented,” added Dittmar. “Over the years, it has also been a reliable target for buyers from outside the U.S. drawn by its established production and ease of access to Gulf Coast markets. That is continuing with a modest gas acquisition by Mitsui already in April. We view the Eagle Ford as an optimal place to buy production-heavy assets, and some inventory, but it is generally not the ideal play for companies needing a big chunk of undeveloped acreage to be looking.”

For undeveloped land, companies will need to turn to the Permian Basin. Matador Resources was among the E&Ps looking to expand in the Permian and paid $1.6 billion for EnCap’s Advance Energy Partners with holdings in the Delaware Basin. The deal is part of a rush of private equity (PE) exits, with EnCap among the most active sellers. That also includes the early April divestment of three EnCap portfolio companies in the Midland Basin to Ovintiv for more than $4 billion.

“Most public companies are in need of inventory, and the land held by private E&Ps is where they can find it,” said Dittmar. “However, adding these locations comes at an increasing cost. Top-tier locations in the Permian nearly always garner more than $2 million each now, and some deals have approached the $3 million per location mark. We anticipate core locations will break the $3 million mark this year as the inventory situation for operators isn’t getting any better.”

The recent major Permian deals have gone to large operators with Matador, a sizable company with a market cap of nearly $6 billion, among the smaller buyers. These companies have the cash and favorable stock valuations to afford higher priced acreage. However, many smaller companies are in even more need of extending drilling inventory to satisfy investors. “It’s a catch-22,” Dittmar said. “Small operators need inventory to improve investor sentiment and get a higher multiple on their stock, but without the higher multiple they really can’t afford these deals and keep them accretive to cash flow. The solution lies in targeting tier 2 and tier 3 M&A opportunities, plus smaller bolt-on transactions that tend to be cheaper.”

Another potential, though not widely used, option is mergers of equals among SMID-caps. Corporate M&A, outside of the Baytex and Ranger deal mentioned above, has been a relatively minor part of the market since the end of 2020. While two SMID-cap E&Ps merging may not solve inventory issues, it would increase scale in a market where investors view bigger as better and potentially produce operational and administrative synergies that could help their stock price.

While public companies shop for private E&Ps to acquire, the remaining PE teams are also looking for non-core assets shed by public operators. WildFire Energy, backed by Warburg Pincus and Kayne Anderson, was among those PE buyers in Q1 when the team purchased Chesapeake’s Eastern Eagle Ford or Brazos Valley assets for $1.425 billion. More PE teams have been doing their buying outside the crowded Permian where rising prices for undeveloped land has made it hard to compete. By contrast, assets in plays like the Eagle Ford and Bakken can often be purchased for the value of existing production alone without having to pay anything for acreage. That was the case in the WildFire deal, and in a purchase of Ovintiv’s Bakken assets by EnCap-sponsored Grayson Mill that coincided with EnCap’s Midland sale in early April.

“M&A may have slowed, and shale may be in its later innings, but there are still opportunities to be had,” concluded Dittmar. “The scramble for dwindling inventory is on, and oil prices are in a good place for M&A where both buyers and sellers feel comfortable transacting. Gas deals are likely to remain challenged as pricing is low and volatile, a murderous combination. However, gas may be poised to pick up the slack in the future when buyers start eying recovering prices driven by increasing U.S. LNG exports and offer buyouts that are acceptable to sellers.”

Members of the media can contact Jon Haubert to request a copy of the full report or to schedule an interview with one of Enverus’ expert analysts.

Additional resources

- Royalty M&A 2023 debut: Kimbell’s Midland Basin $143M buy

- Upstream M&A falls 13% year-over-year in 2022 to $58B

About Enverus

Enverus is the most trusted, energy-dedicated SaaS platform, offering real-time access to analytics, insights and benchmark cost and revenue data sourced from our partnerships to 98% of U.S. energy producers, and more than 35,000 suppliers. Our platform, with intelligent connections, drives more efficient production and distribution, capital allocation, renewable energy development, investment and sourcing, and our experienced industry experts support our customers through thought leadership, consulting and technology innovations. We provide intelligence across the energy ecosystem: renewables, oil and gas, financial institutions, and power and utilities, with more than 6,000 customers in 50 countries. Learn more at Enverus.com.

About Enverus Intelligence Research

Enverus Intelligence Research, Inc. is a subsidiary of Enverus and publishes energy-sector research that focuses on the oil and natural gas industries and broader energy topics including publicly traded and privately held oil, gas, midstream and other energy industry companies, basin studies (including characteristics, activity, infrastructure, etc.), commodity pricing forecasts, global macroeconomics and geopolitical matters.

Media Contact: Jon Haubert | 303.396.5996