Guide to Permian Basin Oil and Gas Data – Maps – Geology – Facts

The Permian Basin is renowned for vast oil and gas reserves and record-breaking daily production levels that established the United States as the largest producer in the world. The following sections provide details about the Permian Basin’s production capacity, major geological structures, market activity, and most recent news.

The Permian Basin is a large, hydrocarbon rich sedimentary basin located beneath West Texas and southeastern New Mexico. It is the most productive oil-producing basin in the world and has been a cornerstone of U.S. energy supply for more than a century.

The basin is named after the Permian geologic period (approximately 299–252 million years ago), during which repeated cycles of marine deposition created thick sequences of organic rich shales, carbonates, and sandstones. These rock layers generated and trapped enormous volumes of oil and natural gas, forming one of the most extensive stacked hydrocarbon systems on Earth with shales, carbonates, and sandstones.

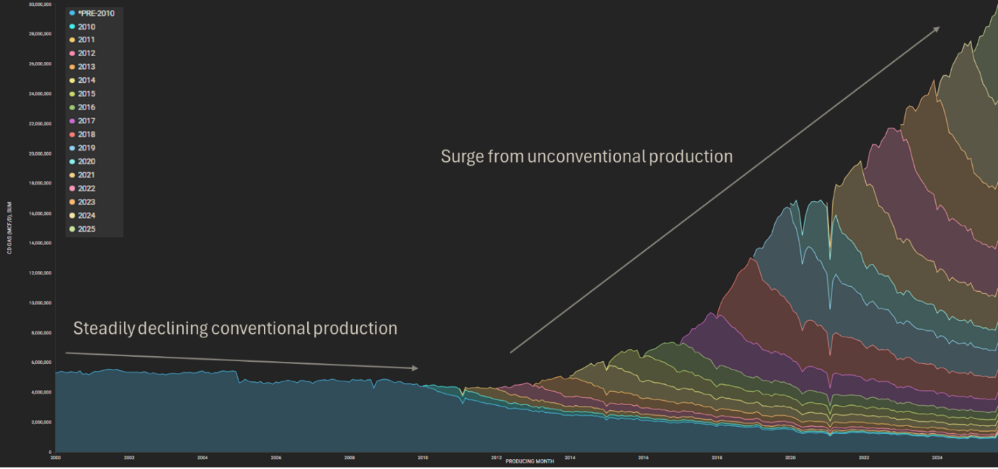

Oil and gas production in the Permian Basin began in the early 1920s and initially focused on conventional vertical wells targeting carbonate and sandstone reservoirs. Production from these conventional fields peaked in the 1970s and declined for several decades as reservoirs matured. Beginning in the late 2000s, advances in horizontal drilling and multistage hydraulic fracturing unlocked large volumes of oil and gas from low permeability shale reservoirs, reversing the basin’s decline and driving a sustained resurgence in production.

Today, the Permian Basin is developed primarily through unconventional horizontal wells targeting multiple stacked formations from the same surface location. This development style, combined with extensive infrastructure and relatively low breakeven costs, has enabled the basin to scale production more rapidly and flexibly than most other oil provinces globally.

The Permian Basin is commonly divided into three primary structural components:

Together, these sub-basins host dozens of producing formations and remain the focal point of U.S. upstream investment and innovation.

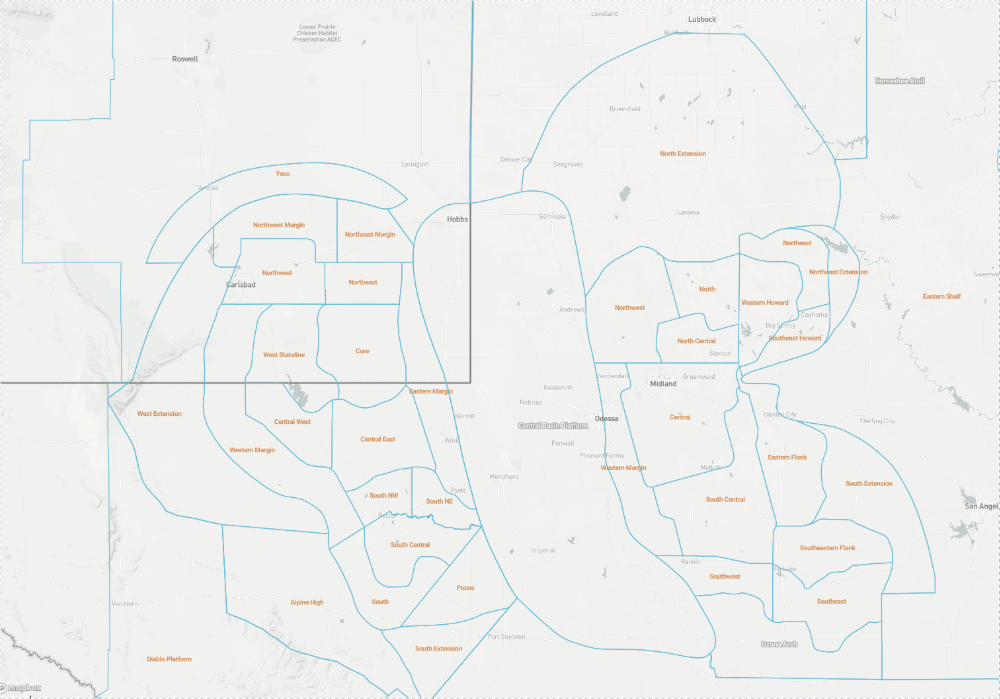

The Permian Basin spans a vast area of West Texas and southeastern New Mexico, covering roughly 86,000 square miles. The Permian Basin extends from just south of Lubbock and Midland-Odessa in Texas to the outskirts of Carlsbad and Hobbs in New Mexico. The basin is traditionally divided into 3 main subregions: the Midland Basin to the east, the Delaware Basin to the west, and the Central Basin Platform that separates them.

Figure 1: Major shale plays in U.S and Canada (Source: Enverus)

Figure 2: Permian Basin sub-plays (source: Enverus)

The Permian Basin is the world’s most prolific basin in terms of oil and gas production from unconventional reservoirs due to multiple stacked pay zones, abundant infrastructure, and low breakeven costs for development.

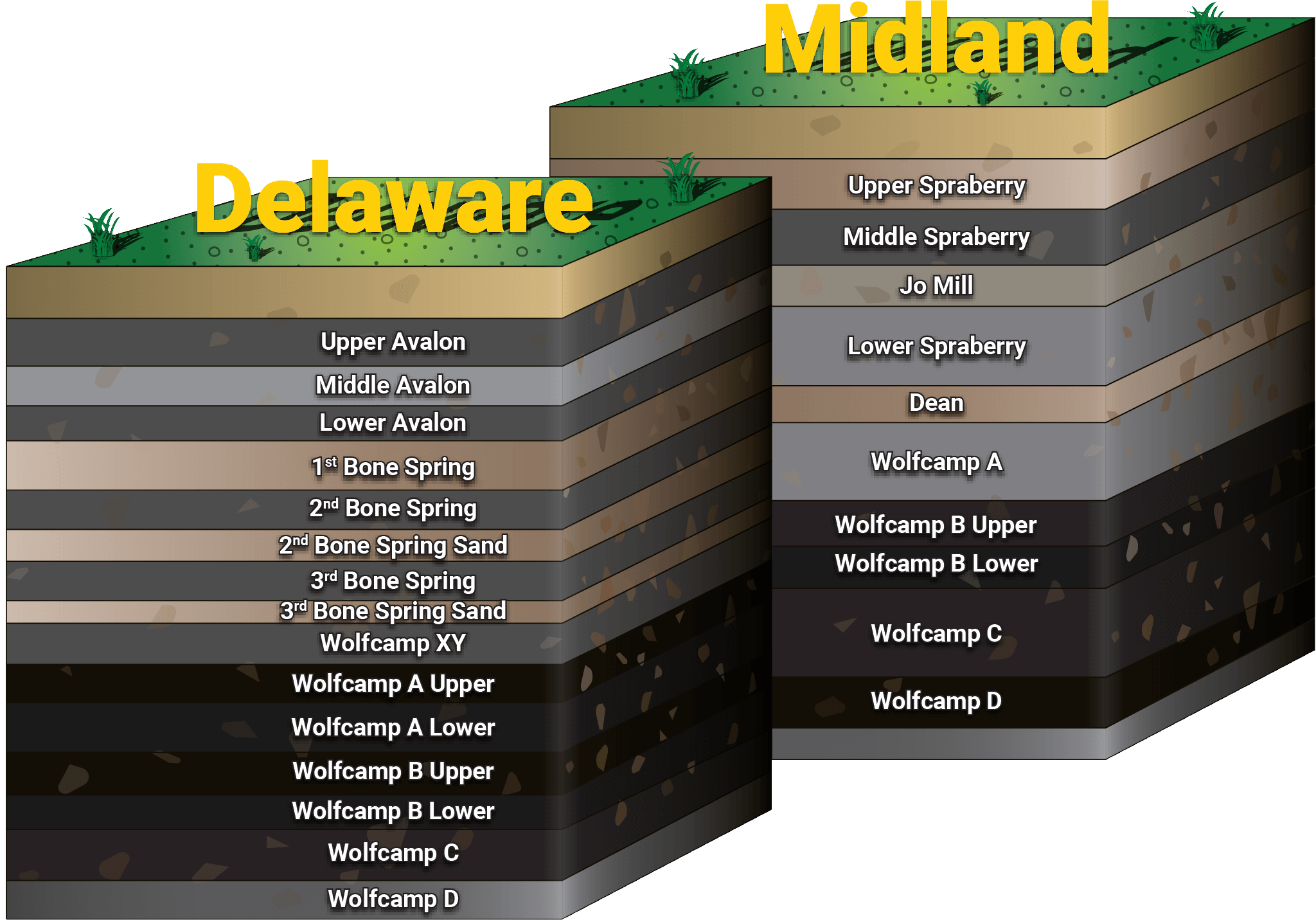

The term stacked pay refers to the number of commercially viable landing zones that are available on a single surface location. The Permian Basin’s defining characteristic is its scale of stacked pay. While this quality is not exclusive to the Permian, its magnitude of stacked pay is considerably greater than what is seen in most other unconventional plays in North America. To provide context, the thickness of the hydrocarbon column being currently developed is over 2,000 feet in the Midland and Delaware basins, compared to 300 feet and 500 feet in the Williston Basin in North Dakota and Eagle Ford trend in South Texas.

While the resource potential of the Permian Basin’s stacked pay is undeniable, development of this resource is challenging in practice as flow barriers between zones are not always present. As many operators have prioritized development of their most productive landing zones, sub-optimal resource recovery of the commercial hydrocarbon column is observed throughout the basin due to parent-child well dynamics.

Figure 3: Delaware and Midland stacked pay targets (Source: Enverus)

The Santa Rita #1, a cable-tool drilling rig, discovered oil near Big Lake in 1923, transforming a remote region of west Texas into a cornerstone of U.S. energy production. In the early decades, wells were drilled one at a time with manual equipment and wooden derricks, often taking months to reach target depth.

By the 1950s through the 70s, mechanized rotary rigs and improved mud systems enabled faster and deeper vertical drilling. The basin entered a period of large-scale field development as operators mapped stacked formations like the Spraberry and Wolfcamp, drilling thousands of vertical wells that tapped only a fraction of the shale rock’s potential.

In the late 2000s, the combination of horizontal drilling and multi-stage hydraulic fracturing brought new life to the basin. By steering wells laterally through thin, hydrocarbon-rich zones and unlocking the flow of oil with hydraulic fracturing, the Permian Basin became the epicenter of the Shale Revolution and the most productive basin in the world.

Today, remaining inventory in the Permian Basin is the key driver of long-term value, as top-tier shale plays are becoming more depleted and expensive. Undeveloped locations support long-term cash flow visibility, asset valuations, and acquisition strategies. Balancing current production with maintaining future value of the asset is a challenge for all operators. In some cases, operators are turning to secondary basins to protect their dwindling inventory.

The Permian Basin remains one of the most resource-rich oil provinces in the world due to its extensive stacked pay zones and long history of continuous technological improvement. While the basin has already produced tens of billions of barrels of oil, large volumes of hydrocarbons remain technically recoverable across multiple formations. The ultimate volume of oil that will be produced depends not only on geology, but also on economics, infrastructure, and development strategy.

Figure 4: Permian Basin Calendar Day Gas Rate = Monthly Gas Volume / Days in Month

(Source: Enverus)

The Permian Basin contains multiple hydrocarbon-bearing formations stacked vertically across the Midland and Delaware basins, including the Wolfcamp Shale, Bone Spring, and Spraberry Trend. These stacked intervals create one of the thickest hydrocarbon columns currently under development, exceeding 2,000 feet in many core areas, with formations stacked vertically across the Midland and Delaware basins.

According to U.S. Geological Survey assessments, the Wolfcamp and Bone Spring formations alone contain an estimated 50 billion barrels of technically recoverable oil and nearly 300 trillion cubic feet of natural gas. Continuous testing of additional intervals has expanded the recognized resource base over time, pushing development toward the outer extents of the basin as economic viability is proven.

While the Permian Basin’s geological endowment is vast, the volume of oil that can be economically recovered is governed by a range of non-geologic factors. Commodity prices, takeaway capacity, regulatory conditions, and development costs all influence whether technically recoverable resources become commercial reserves.

Forecasting oil and gas production accurately in the Permian can be a challenge, as there are many factors at play that influence well performance. Subsurface complexity, parent‑child interactions, and spacing decisions further complicate forecasting remaining recoverable oil. As a result, accurately forecasting production requires integrating geologic, engineering, and macroeconomic variables rather than relying solely on volumetric resource estimates.

The Permian Basin is not a single uniform structure, but a complex system of subbasins formed by differential subsidence and tectonic activity. The basin is traditionally divided into three primary components: the Delaware Basin, the Midland Basin, and the Central Basin Platform. Each has distinct geology, depth, and development characteristics that influence drilling strategy and economic outcomes.

The Delaware Basin is the westernmost and deepest subbasin of the Permian, spanning West Texas and southeastern New Mexico. It covers approximately 6.4 million acres and contains some of the thickest sedimentary packages in the basin. Historically developed with vertical wells, the Delaware has been transformed by horizontal drilling targeting the Wolfcamp and Bone Spring formations.

The basin extends from Lea and Eddy counties in New Mexico southward into Pecos County, Texas. Portions of the northern Delaware lie on federal land, which typically carries lower royalty rates but also includes surface access constraints related to potash mining. Structurally, the Delaware Basin is heavily faulted and exhibits complex pressure and maturity trends, with oilier, overpressured zones toward the eastern side adjacent to the Central Basin Platform.

The Midland Basin forms the eastern half of the Permian Basin and has a long history of oil production dating back to the 1940s. It extends roughly 14,000 square miles from northern West Texas to Crockett County in the south and is home to the Midland, Odessa metropolitan area, the largest population center in the region.

Historically, development focused on vertical wells in the Spraberry formation. With the adoption of horizontal drilling, activity shifted toward the Wolfcamp and Lower Spraberry intervals. Compared to the Delaware, the Midland Basin is generally shallower, less over-pressured, and less faulted. Modern development is concentrated in the northern, oil-prone portion of the basin, while higher gas‑oil ratios have limited activity in the southern areas, which are less over‑pressured and less faulted.

The Central Basin Platform (CBP) is a shallow subsurface structural feature separating the Delaware and Midland basins. It has been one of the most prolific conventional oil-producing regions in the Permian, accounting for approximately 45% of total historical production from the basin.

Development on the CBP has historically relied on vertical wells targeting carbonate reservoirs such as the San Andres, Grayburg, Clear Fork, and Devonian formations. While smaller in areal extent than the adjacent basins, the CBP is known for low well costs and consistent returns. Operators are increasingly applying horizontal drilling and modern completion techniques to unlock additional value from mature conventional fields.

Modern Permian Basin development reflects the industrialization of shale operations. Advances in horizontal drilling, multi-well pad development, and subsurface analytics have transformed the basin into a highly optimized manufacturing environment, enabling operators to extract more hydrocarbons with fewer rigs and lower unit costs.

In unconventional development, well spacing refers to the subsurface distance between horizontal wellbores targeting the same or adjacent reservoirs. In the Permian Basin, wells within a drilling spacing unit may target multiple stacked benches, with laterals commonly spaced 500 to 1,000 feet apart, depending on geology and operator strategy.

Parent-child well interactions are a defining challenge in the basin. Parent wells are the first producers in a reservoir, while child wells drilled later may experience reduced performance due to pressure depletion and fracture interference. Vertical and horizontal communication between stacked zones further complicates spacing decisions, requiring operators to consider the full four-dimensional evolution of the reservoir over time.

Cube development refers to drilling and completing multiple stacked horizontal wells across several formations in a coordinated pattern, treating the reservoir as a single three-dimensional system rather than developing zones sequentially. This approach aims to optimize drainage efficiency and reduce parent-child degradation.

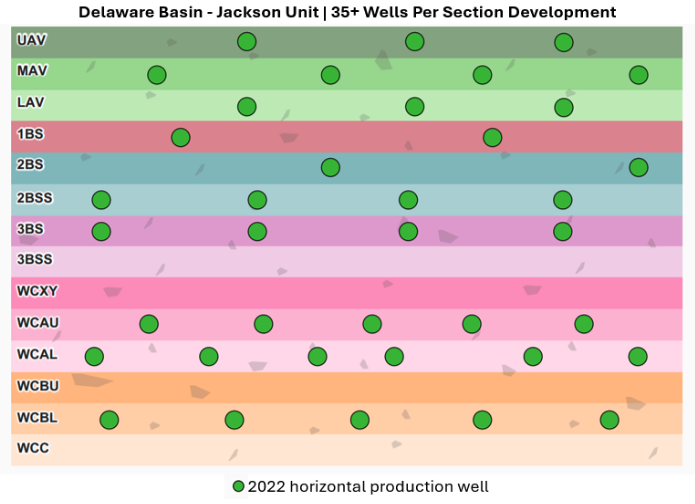

Extended-reach laterals exceeding 4 miles are increasingly common, while 2 to 3 mile laterals represent prevailing best practice on cube-style pads. Early pilots featuring more than 20 wells per pad demonstrated both the potential and the limits of dense development. Many operators now favor 4 to 8 well pads to balance productivity, cost efficiency, and reservoir interference.

Figure 5: Example of near full-stack co-development of all reservoir intervals in the core of the Delaware Basin – Jackson Unit at 35+ wells per section density. (Source: Enverus)

Despite rising production, the Permian Basin rig count has trended lower as drilling and completion efficiency has improved. Modern operations rely on super spec rigs, batch drilling, and pad walking techniques that allow a single rig to drill multiple wells with minimal downtime.

Completions are increasingly executed in continuous sequences, with higher stage counts, longer laterals, and optimized proppant and fluid designs. This factory style approach has reduced cycle times and capital intensity while enabling sustained production growth even in periods of capital discipline.

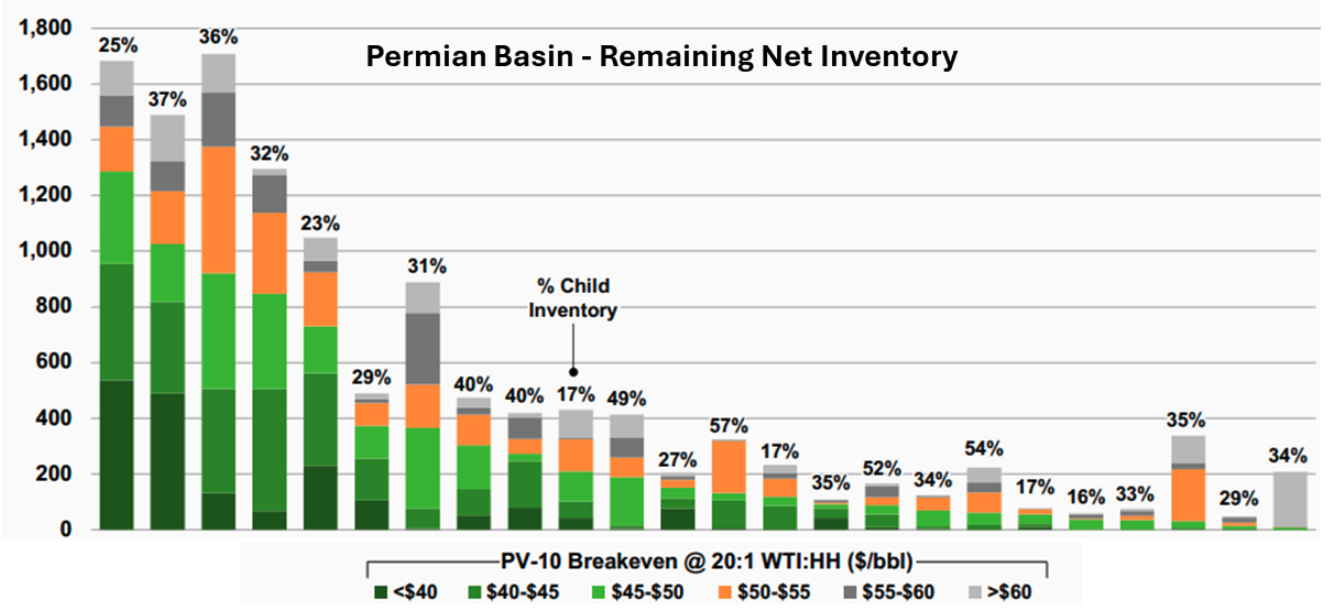

Remaining drilling inventory is one of the most important long-term value drivers in the Permian Basin. As shale plays mature and multi-well pad development accelerates, operators and investors increasingly focus on how many high-quality undrilled locations remain, where they are concentrated, and how efficiently they can be developed. Inventory underpins asset valuations, M&A strategy, and long-range production planning because it is the clearest indicator of future cash flow visibility.

Figure 6: Remaining net inventory for the Permian Basin from 2025 Enverus Permian Play Fundamentals.

Note: Location count normalized to 10,000 ft lateral length.

In the Permian, “inventory” is not just a location count. Quality varies materially based on geology, landing zone, spacing, and development constraints. The draft highlights that remaining inventory has been pressured by the widespread shift toward multi-well pads and stacked development, which can reduce future spacing optionality and accelerate depletion of top-tier benches in core areas.

As core locations become more competitive and more drilled up, some operators increasingly look beyond the most developed areas to bolster runway, including turning to secondary basins and areas to extend inventory life. At the same time, the basin’s stacked pay means inventory is often evaluated by bench, not just by surface acreage, because multiple landing zones can exist within the same development footprint.

Inventory is a strategic balancing act: maximizing current production while preserving future value. With capital discipline tightening, stakeholders tend to scrutinize not only how much inventory exists, but whether it can be developed economically under realistic assumptions and without degrading returns through interference or suboptimal sequencing.

This primary goal of capital efficiency is why modern Permian strategy increasingly blends development optimization with portfolio actions. Operators work to protect inventory value through disciplined spacing, cube development design choices, and sequencing decisions, while also using acquisitions, trades, and bolt-ons to maintain a high-quality runway where organic inventory is thinning.

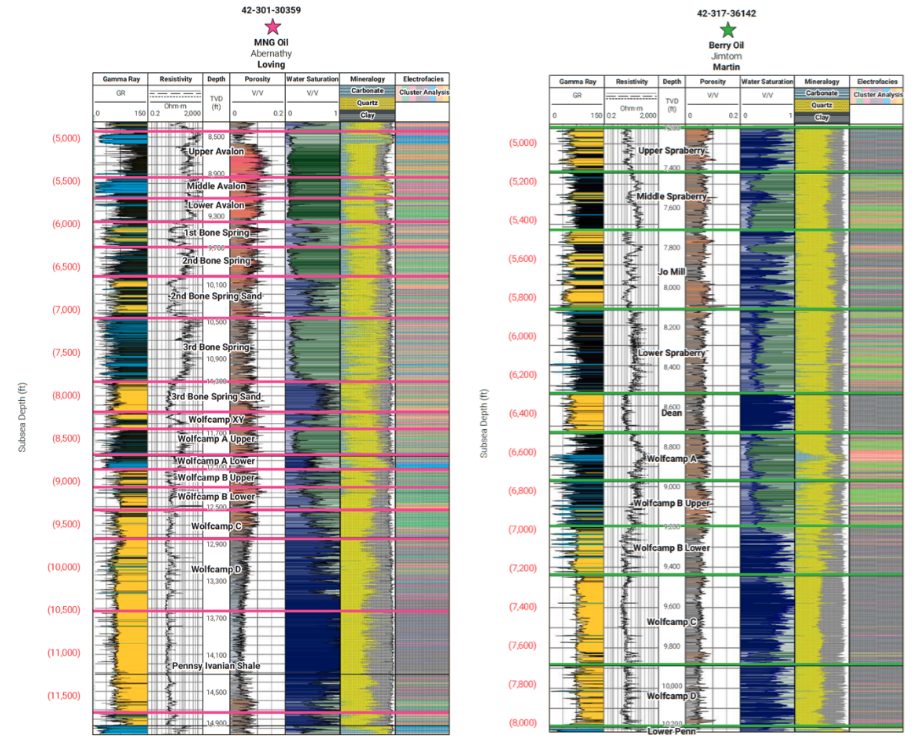

Figure 7: Two type wells, showing the primary intervals in each basin, Delaware (left) and Midland (right). (Source: Enverus)

The Wolfcamp is the most prolific unconventional play in the Permian and a foundational target in both the Delaware and Midland basins. Deposited during the Lower Permian in a deepwater basin setting when sediment input was limited and organic matter accumulated under low oxygen conditions.

The formation consists of a thick succession of organic-rich mudstones interbedded with carbonate debris flows and siliceous sediments, creating a highly resource dense system capable of generating and retaining large volumes of hydrocarbons. This depositional environment preserved the organic material required to source the basin’s extensive oil and gas accumulations.

The Wolfcamp is commonly divided into multiple development benches, including:

Thickness varies significantly across the basin. In the Delaware Basin, the Wolfcamp can exceed 3,000 to 4,000 feet, reaching maximum thicknesses greater than 6,000 feet in parts of Reeves, Loving, and Eddy counties. This exceptional thickness allows operators to develop multiple horizontal targets stacked vertically within the same drilling unit.

In the Midland Basin, the Wolfcamp is thinner, generally ranging from 1,000 to 3,000 feet, with development focused primarily on the Wolfcamp A and B benches. Differences in subsidence history and thermal maturity result in variations in fluid composition, pressure, and optimal landing zones between the two basins.

The Wolfcamp scale, thickness, and resource density make it uniquely suited to modern stacked and cube development strategies, but these same characteristics also introduce challenges related to well interference, spacing optimization, and parent-child interactions that continue to shape development outcomes across the Permian.

The Spraberry is a major target in the Midland Basin and historically carried the reputation of being highly resource-rich but challenging to develop economically before modern shale techniques. It is a stacked system of alternating siltstones, fine-grained sandstones, and organic-rich mudstones deposited as submarine fan packages during the Middle Permian.

The Spraberry is commonly divided into:

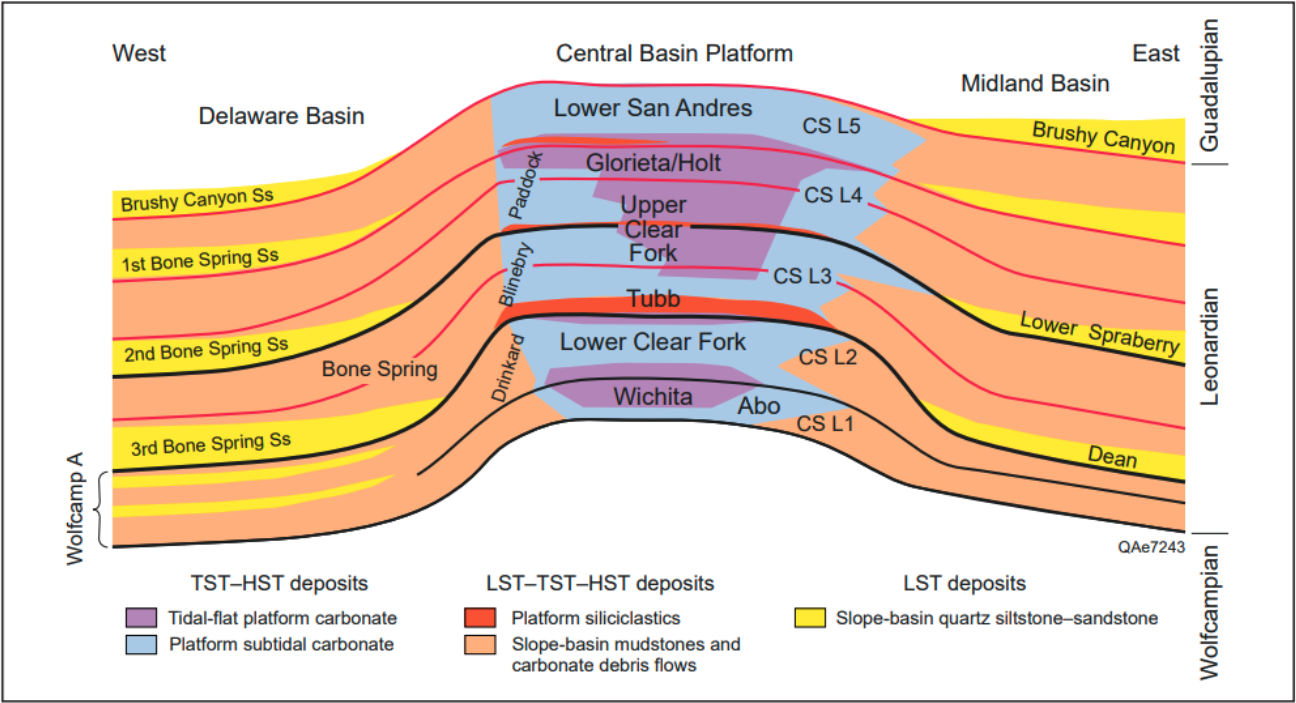

Figure 8: The Permian Basin geology (Source: Ruppel, S. C. (Ed.). (2020). Anatomy of a Paleozoic Basin: The Permian Basin, USA (Vol. 1). Bureau of Economic Geology, The University of Texas at Austin, Report of Investigations No. 285.)

The Bone Spring is developed in the Delaware Basin and is one of the primary targets in Eddy and Lea counties in New Mexico. The Bone Spring represents the slope-basinal equivalent of the shelf carbonates found on the Northwest Shelf. Overlying the Wolfcamp, the Bone Spring records the transition to a time of active sediment influx, where pulses of clastic sands and silts were transported by submarine fans and turbidites into the deep basin during sea level lows, and alternated with carbonate debris flows that shed off the shelf margins during sea level highs. This complex depositional history created a system where organic-rich source rocks are interstratified with permeable reservoirs

The Bone Spring is generally divided into three primary stratigraphic intervals known as the First, Second, and Third Bone Spring, with each interval typically containing a carbonate member (top) and a sandstone member (bottom). First, Second, & Third Sands: The sandstone members of each interval serve as the primary reservoirs for horizontal development. Avalon Shale: A distinct, organic-rich mudstone unit known as the Avalon Shale exists within the First Bone Spring Carbonate interval and is targeted as a separate unconventional play.

The Second and Third Bone Spring Sands are the most targeted, due to their high-quality reservoir characteristics.

Conventional vertical drilling initiated the development of these zones. However, horizontal drilling has expanded the play. The complex submarine channel depositional environment of these formations adds complexity to optimizing the reservoir target across the basin. The carbonate and shale intervals between the sands are more recently being assessed and proven out for their economic resource potential.

Conventional Permian development historically relied on vertical wells targeting higher permeability reservoirs in stratigraphic or structural traps. Major conventional plays discussed include platform carbonate reservoirs such as the San Andres and Grayburg on the Central Basin Platform and Northwest Shelf, including legacy fields and long life waterflood and tertiary recovery projects.

Unconventional Permian development centers on horizontal wells completed with multistage hydraulic fracturing to produce from low permeability shales and tight intervals. This modern phase of development, driving the Shale Revolution, is concentrated in formations like the Wolfcamp, Bone Spring, and Spraberry, where stacked pay enables multiple landing zones and high-density development from multi-well pads.

Driving U.S. energy independence, the Permian Basin is powered by a mix of supermajors, independents, and midstream operators supported by an expanding network of pipelines, processing facilities, and water infrastructure. Together, they enable the region’s unmatched scale of production and growth.

The Permian Basin has attracted significant attention and investment from many supermajors, including Chevron, ExxonMobil and ConocoPhillips. Other large operators include Diamondback, Occidental, EOG, Mewbourne Oil, Permian Resources, Devon, SM Energy and Coterra Energy. Despite steady consolidation and the majority of core acreage held by a few large operators, Permian Basin oil companies are still dominated by hundreds of medium and smaller independent producers. Together, these operators drill and operate in the remaining core acreage, CBP, and Permian shelves.

The Permian Basin has seen significant consolidation over the past decade. At the peak in 2015, there were roughly 1,660 operators holding leases across Texas and New Mexico. Today, that number has fallen to fewer than 400. As consolidation continues driven by remaining drilling inventory, this number is expected to shrink further.

The Permian Basin’s scale and longevity are enabled not only by geology, but by one of the most extensive energy infrastructure networks in North America. A dense system of pipelines, processing facilities, and water infrastructure allows operators to move large volumes of oil, natural gas, and produced water efficiently across a remote region, reducing development risk and supporting continuous production growth.

The Permian Basin pipeline system consists of thousands of miles of gathering and transportation pipelines that move crude oil, natural gas, and natural gas liquids (NGLs) from well sites to downstream markets. As production surged during the shale era, midstream investment expanded to address takeaway constraints and improve connectivity between the basin and refining, petrochemical, and export hubs.

While geographically distant from Gulf Coast markets, the Permian plays a critical role in domestic and international energy supply. Dedicated crude and gas transmission pipelines have increasingly connected Permian production to U.S. refineries and LNG export facilities, enabling associated gas volumes that were once stranded or flared to reach global markets. Continued midstream buildout has helped stabilize pricing differentials and reduce bottlenecks during periods of rapid growth.

Water infrastructure is as critical to Permian operations as hydrocarbons pipelines. Permian wells produce enormous volumes of water alongside oil and gas, creating a parallel system of pipelines, disposal wells, and treatment facilities dedicated to managing produced water.

Historically, most produced water was disposed of through saltwater injection wells. However, rising disposal costs, regulatory scrutiny, and seismicity concerns have driven increased investment in recycling infrastructure. Operators now increasingly transport produced water by pipeline to centralized treatment facilities, where it can be reused in hydraulic fracturing operations or shared among neighboring operators. Water infrastructure is as critical to Permian operations as hydrocarbon pipelines are. The draft also highlights emerging interest in beneficial reuse and technologies such as direct lithium extraction, which could transform produced water from a liability into a strategic resource.

Despite its scale and productivity, the Permian Basin faces a set of structural and operational challenges that influence development strategy and long-term sustainability. These challenges are closely tied to the basin’s success, as high activity levels amplify pressures on water systems, infrastructure, and regulatory frameworks.

Produced water management is one of the most significant challenges in the Permian Basin. The draft notes that operators collectively produce tens of millions of barrels of water per day, with volumes expected to continue rising as wells mature and water-to-oil ratios increase. In some areas, particularly the Delaware Basin, water-to-oil ratios can reach double digits as water-to-oil ratios increase.

Large-scale disposal of produced water through injection wells has been linked to increased seismicity risk in certain areas, prompting regulatory limits and operational adjustments. These pressures are forcing operators to rethink historical disposal-only models and accelerate investment in recycling, reuse, and alternative water management strategies to mitigate risk while maintaining development pace.

Regulatory frameworks and infrastructure availability continue to shape Permian development outcomes. Portions of the basin, particularly in southeastern New Mexico, include federal lands that carry different permitting timelines and surface access restrictions compared to private leases in Texas. Additional constraints, such as potash mining areas in the northern Delaware Basin, can further complicate surface development and well placement.

Takeaway capacity has historically lagged production growth during periods of rapid expansion, creating pricing volatility and operational challenges. While major investments have improved oil, gas, and water takeaway in recent years, maintaining alignment between production growth and infrastructure expansion remains a persistent challenge for the basin as development continues to evolve.

The Permian Basin is more than an energy powerhouse; it’s home to a diverse network of communities that have grown alongside the region’s oil & gas industry. From historic ranching towns to thriving urban centers, and the world-renowned University of Texas Permian Basin, these communities form the social and economic backbone of west Texas and southeastern New Mexico.

The Permian Basin spans an area approximately 300 miles in length and 250 miles wide in west Texas and southeastern New Mexico. The surface acreage of the basin encompasses more than 50 counties in this region whose population is approximately half a million residents.

The cities of the Permian Basin support a rapidly growing regional economy that spans west Texas and southeastern New Mexico. These communities support a large oil & gas workforce, including drilling and production operations, myriad oilfield support services, and an extensive supply chain.

Whether you’re looking to better understand the M&A market, dive deep into the subsurface or understand trends in oil production, the Enverus Intelligence Research team is your source of truth. As an oil and gas operator, having the right data to decode the Permian Basin can make all the difference between a successful well or not. Enverus is the largest energy-only focused software company in the world, with more than 6,000 businesses relying on our solutions. As your strategic technology partner, Enverus empowers you to make smart, informed decisions, ensuring your assets perform optimally and tackle market challenges head-on.

The Permian Basin is the largest oil producing basin in the world, located in West Texas and southeastern New Mexico. It is known for its stacked hydrocarbon formations and large-scale horizontal shale development.

The basin spans approximately 86,000 square miles across West Texas and southeastern New Mexico, extending from the Midland Odessa area in Texas to the Carlsbad and Hobbs regions of New Mexico.

The Permian Basin contains multiple stacked oil and gas bearing formations that can be developed from the same surface location. This stacked pay, combined with modern drilling technology and extensive infrastructure, allows operators to produce large volumes at competitive costs.

The three primary subbasins are the Delaware Basin, the Midland Basin, and the Central Basin Platform. Each has distinct geology, depth, and development characteristics.

The Permian Basin contains tens of billions of barrels of technically recoverable oil, primarily within the Wolfcamp and Bone Spring formations. The amount that can ultimately be produced depends on technology, commodity prices, and development strategies.

Stacked pay refers to the presence of multiple commercially viable hydrocarbon zones layered vertically within the subsurface. In the Permian Basin, stacked pay can exceed 2,000 feet, enabling multizone development from a single pad.

Key formations include the Wolfcamp, Bone Spring, Spraberry, and San Andres. These formations account for the majority of modern oil and gas production in the basin.

A small group of supermajors and large independent producers including Exxon, Diamondback, Occidental, EOG, Mewbourne Oil, ConocoPhillips, Permian Resources, Devon, Chevron. SM Energy and Coterra Energy have drilled the most wells ins 2024-2025, and control much of the remaining high-quality drilling inventory, among others.

Development is dominated by horizontal drilling, multi-well pads, and cube development strategies that target multiple stacked formations simultaneously to optimize recovery and reduce interference between wells.

Key challenges include produced water management, induced seismicity, infrastructure constraints, and managing remaining drilling inventory as core areas mature.

Let’s get started!

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Ready to Subscribe?

Ready to Get Started?

Ready to Subscribe?

Sign Up

Power Your Insights