[contextly_auto_sidebar]

CRUDE OIL

- Crude oil futures ended last week at a 14-month low, with April WTI settling at $44.76/bbl on Friday. The rapid spread of COVID-19 outside of China and the rising likelihood of a global economic slowdown sent financial markets around the world into a selloff, and oil futures trading has not been immune to the selling pressure. With China’s economy weakened by the COVID-19 outbreak, market participants for several weeks had been expecting a significant reduction in China’s petroleum demand growth outlook for this year. Now it appears that almost every major economy in the world is threatened by the spread of the disease, raising the grim prospect of an even weaker price environment than we’ve seen thus far. Nevertheless, hopes of another round of production cuts by OPEC and allied non-OPEC countries later this week have bolstered prices in early morning trading today. Ministers from OPEC+ countries will meet this Thursday and Friday to discuss increasing current production cuts by another 0.6-1.0 MMbbl/d in the second quarter. Russia has been resisting further curbs on production, with President Vladimir Putin recently commenting that the country’s finances could live with current prices and even stomach Brent at $42.40/bbl. This may be just pre-negotiation posturing, as Russia has been known to do ahead of past OPEC+ meetings; it is apparent that a very large production cut is going to be required, and Moscow likely knows Russia will need to carry some of the burden.

- The US Energy Information Administration last week reported a crude oil inventory build of 0.5 MMbbl for the week that ended Feb. 21. While that is relatively unexciting news, gasoline and distillate inventories drew 2.7 MMbbl and 2.1 MMbbl, respectively, as crude runs fell close to 200,000 bbl/d week-on-week and demand posted modest gains. Total petroleum inventories fell by 2.1 MMbbl.

- The Commodity Futures Trading Commission reported a 7,515-contract drop for managed-money long positions in NYMEX light sweet crude futures last week, taking the total number of long positions to 215,912 contracts. Managed-money short positions in futures also decreased, dropping by 36,625 contracts to stand at 81,481 contracts in total.

NATURAL GAS

- US Lower 48 dry natural gas production increased 0.39 Bcf/d last week, based on modeled flow data analyzed by Enverus, largely due to a 0.53 Bcf/d production increase in the East, while Canadian imports decreased 0.47 Bcf/d. Res/Com saw the biggest drop in demand on the week, falling 5.39 Bcf/d, while power and industrial demand decreased 1.08 Bcf/d and 0.33 Bcf/d, respectively. LNG export demand increased 0.55 Bcf/d on the week as Sabine Pass and Cameron completed maintenance, while Mexican exports gained 0.12 Bcf/d. Weekly average totals show the market dropping 0.08 Bcf/d in total supply while total demand fell by 6.31 Bcf/d last week.

- The storage report for week that ended Feb. 21 showed a draw of 143 Bcf. Total inventories now sit at 2.200 Tcf, which is 637 Bcf higher than at this time last year and 179 Bcf above the five-year average for this time of year. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a weaker draw next week. The ICE Financial Weekly Index report currently expects a draw of 110 Bcf for week that ended Feb. 28.

- Current weather forecasts for the six- to 14-day period from the National Oceanic and Atmospheric Administration’s Climate Prediction Center show normal to above-average temperatures throughout the Lower 48, with the only below-average temperatures seen in Florida and along the West Coast.

- The March 2020 contract closed last week at $1.821/MMbtu, which was $0.008 lower than when it took over as the prompt month contract. April 2020 now sits as the prompt month contract and closed Friday at $1.684/MMbtu, its lowest close since the beginning of the contract life. The contract gained a few cents of traction over the weekend and is trading at $1.732 at the time of writing. However, market sentiment is overwhelmingly bearish, and the market could see a test to the 2016 intraday low of $1.611, which was nearly tested on Friday when prices dropped to intraday lows of $1.642. Continue to monitor weather forecast changes to understand price movement.

NATURAL GAS LIQUIDS

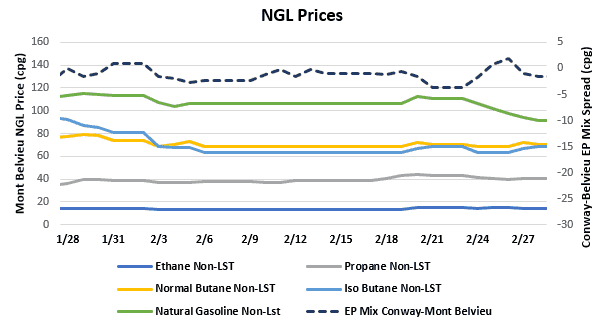

- Purity product prices went both up and down last week depending on the product. Ethane saw a gain of $0.008/gallon to $0.146, while normal butane gained $0.010/gallon to $0.697 and isobutane jumped $0.016/gallon to $0.653. Propane saw a decline of $0.015/gallon to $0.405 and natural gasoline fell $0.102/gallon to $0.984. The large drop in natural gasoline is largely due to the decline in crude.

- The EIA reported December 2019 NGL production last week at 4.971 MMbbl/d, remaining relatively flat to November production of 4.972 MMbbl/d. PADD 3 saw a 20,000 bbl/d decline in December, but was offset by gains in PADD 1 and PADD 2.

- The EIA reported a draw of propane/propylene stocks for week that ended Feb 21, showing inventories decreasing 688,000 bbl. Stocks now stand at 73.57 MMbbl, which is 20.16 MMbbl higher than the same week in 2019 and 19.29 MMbbl higher than the five-year average. The five-year average draw for next week’s report is 3.12 MMbbl, while the same time last year saw a draw of 2.04 MMbbl.

SHIPPING

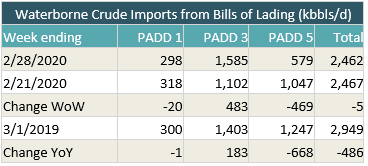

- US waterborne imports of crude oil fell for last week according to Enverus’ analysis of manifests from US Customs and Border Patrol. As of this morning, aggregated data from customs manifests suggested that overall waterborne imports fell by 5,000 bbl/d from the prior week. The decrease was driven by a 469,000 bbl/d drop at PADD 5, partially offset by a 483,000 bbl/d PADD 3 increase. PADD 1 imports fell by 20,000 bbl/d.

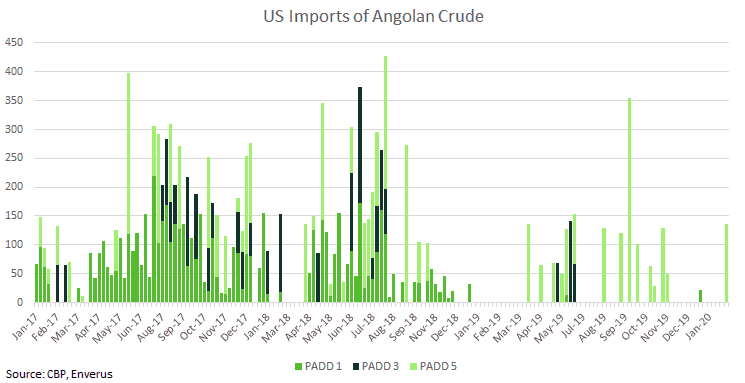

- The US imported crude from Angola for the second time this year as Par Pacific’s Kapolei refinery on Oahu imported a cargo of Cabinda aboard the Suezmax tanker Christina. Phillips 66’s Bayway refinery in New Jersey imported Angolan Hungo crude oil at the beginning of January. US imports of Angolan crude have declined significantly from 2017. Back then, PADD 1 was a consistent importer of Angolan crude, but imports to that region have declined significantly. The most consistent regional importer now is PADD 5.