[contextly_auto_sidebar]

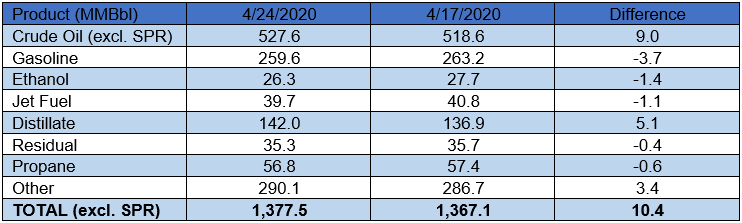

US crude oil stocks posted an increase of 9.0 MMBbl. Gasoline inventories decreased by 3.7 MMBbl and distillate inventories increased by 5.1 MMBbl. Yesterday afternoon, API reported a crude oil build of 9.98 MMBbl alongside a gasoline draw of 1.1 MMBbl and a distillate build of 5.5 MMBbl. Analysts were expecting a crude oil build of 10.6 MMBbl. Total petroleum inventories posted an increase of 10.4 MMBbl.

US crude oil production decreased by 100 MBbl/d, per EIA. Crude oil imports were up 0.4 MMBbl/d last week, to an average of 5.3 MMBbl/d. Refinery inputs averaged 12.8 MMBbl/d (0.31 MMBbl/d more than last week’s average).

The rate of commercial inventory builds appears to be slowing, but stocks in Cushing continue to trend woefully higher, reaching 63.4 MMBbl (roughly 80.6% of working storage capacity) last week. Higher exports and crude runs as well as an increase in SPR fill were major contributors to slowing rate of commercial inventory fill. Refined product demand was also reported higher on the week, with notable gains in gasoline product supplied (up 549 MBbl/d versus the prior reported week). Increased weekly gasoline demand and lower net imports were also instrumental in driving the 3.7 MMBbl draw on gasoline stocks. Nevertheless, the 5.1 MMBbl build in distillates is concerning. After the past few weeks of horrible inventory reports, we were bound to get one that was “less bad”. But make no mistake, physical markets are not out of the woods yet.