[contextly_auto_sidebar]

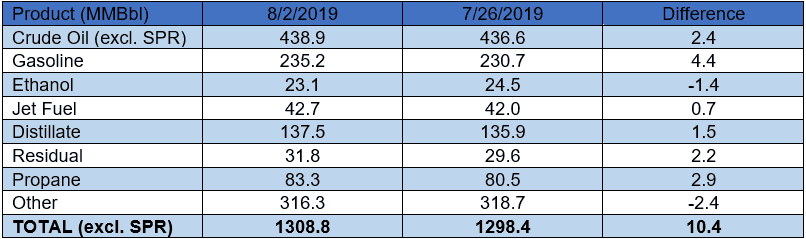

US crude oil stocks posted a increase of 2.4 MMBbl from last week. Gasoline and distillate inventories increased by 4.4 MMBbl and 1.5 MMBbl, respectively. Yesterday afternoon, API reported a crude oil draw of 3.4 MMBbl, while reporting a gasoline draw of 1.1 MMBbl and a distillate build of 1.2 MMBbl. Analysts were expecting a crude draw of 2.8 MMBbl. The most important number to keep an eye on, total petroleum inventories, posted a very large increase of 10.4 MMBbl. For a summary of the crude oil and petroleum product stock movements, see the table below.

US crude oil production increased by 100 MBbl/d last week, per the EIA. Crude oil imports were up 0.49 MMBbl/d last week, to an average of 7.1 MMBbl/d. Refinery inputs averaged 17.8 MMBbl/d (0.79 MMBbl/d more than last week’s average), leading to a utilization rate of 96.4%. Prices sharply fell due to larger-than-expected crude oil and significant total petroleum stocks. Prompt-month WTI was trading down $2.82/Bbl, at $50.81/Bbl, at the time of writing.

Oil prices crashed 8% last Thursday, the largest daily drop since February 2015, in reaction to the US President Donald Trump’s announcement that the US would impose 10% tariffs on $300 billion of additional Chinese goods and products on September 1. The news came in as the market was skeptical yet optimistic about the outcome of the meeting between the US and China in Beijing in an attempt to discuss the faith of trade disputes. The trade tensions between the US and China increased even further this week, as China let its currency, the yuan, drop to a nearly 10-year low and told its state-run companies to halt the imports of US agricultural products in retaliation for the US tariffs, which then was followed by the US branding China as a currency manipulator. China also pledged to impose new “necessary countermeasures” to protect its interests after the tariff announcement last week.

The recent trade escalations between the US and China further increased worries about the global economic and demand growth, and now have the market speculating about what could happen if China were to stop importing oil from the US and reinitiate crude purchases from Iran. This move by China could help Iran increase its production and flood the market, which is already expected to be oversupplied in 2020. The trade disputes and demand worries have now taken the main stage for prices, and the tensions in the Strait of Hormuz and declining production by OPEC at best will try to prevent prices from spiraling down below $50/Bbl levels. Increasing production from the US also is another factor that will keep the pressure on prices.

WTI has traded in a range between $50/Bbl and $61/Bbl this summer, and without additional substantive aggression by Iran forcing a conflict, it is unlikely that prices will garner the support to trade up to the higher side of the range. The market has defined the global economic slowdown as the most important element to trade. Due to the focus on the tariff issue and slowing global growth, the market should drift down, with brief rallies on Middle East news. Prices will test the major support zone at around $50.00/Bbl that held the market in May, as concerns around economic and demand growth intensifies.