Your free guide to navigating the North American and international energy landscape in 2026.

Select “Learn About Enverus Intelligence” below if you would like to unlock Enverus Intelligence® Research’s (EIR) entire collection of in-depth reports, including the unredacted report on 2026 Energy Outlook and Trends, available exclusively for EIR members.

Research written by:

Gibson Scott, CFA, Senior Vice President

Dane Gregoris, CFA, Managing Director

Ian Nieboer, P.Eng., CFA, Managing Director

Dai Jones, Senior Director

Andrew Gillick, Managing Director

Enverus Intelligence® Research, Inc., a subsidiary of Enverus, provides the Enverus Intelligence® | Research (EIR) products. See additional disclosures.

As we head into 2026, the global energy story is shaped by four intersecting forces: repriced oil and gas markets, power systems under strain from AI and electrification, an upstream sector working harder for new molecules and increasingly selective capital. Underpinning all of this are the wildcards from dynamic and ever changing regulatory and geopolitical environments.

Brent and Henry Hub (HH) are resetting lower yet remain constructive over the long term. Power markets are wrestling with how to turn ambitious load forecasts into firm capacity. Upstream activity is moving beyond easy rock. Investors are quietly reshaping who owns both hydrocarbons and low-carbon projects. Combined, these dynamics frame a year in which reliability, cost and decarbonization all matter but are not always aligned.

Against this backdrop, Enverus Intelligence® Research (EIR) organizes the 2026 Global Energy Outlook around the following themes:

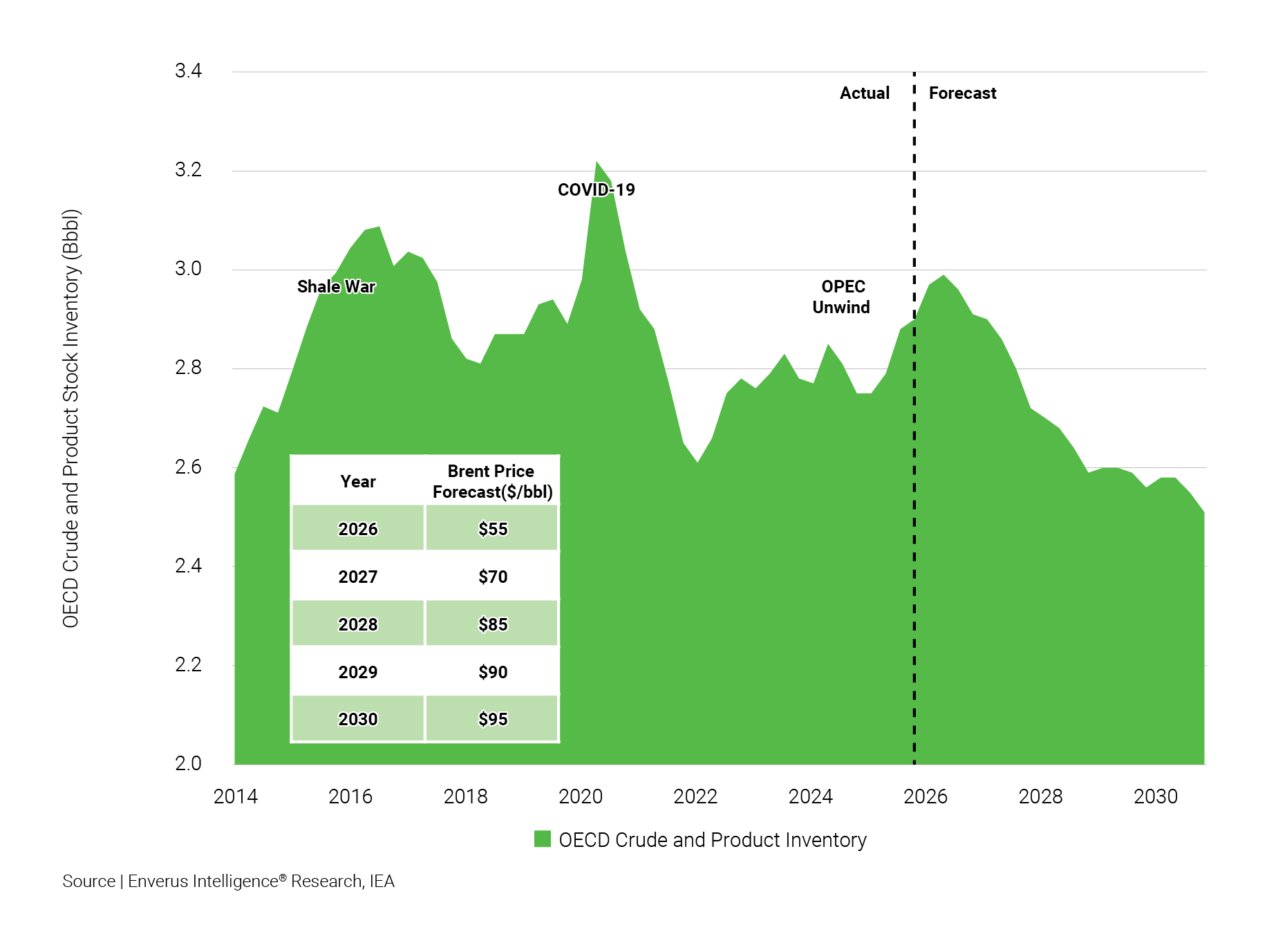

2026 is likely to be characterized by contrasting market dynamics. In the first half, notwithstanding upside risk from increasing geopolitical tensions, oil prices are expected to decline further as global inventories swell to levels not observed since the COVID-19 era and the U.S. shale price war. Global demand in the second half is projected to outpace supply, initiating stock draws and supporting a price recovery. Against this backdrop, Brent crude is forecast to average $55/bbl for 2026, reflecting the combined effects of early-year weakness and late-year stabilization.

On the supply side, OPEC-12 liquids production is currently ~1.2 MMbbl/d below all-time highs. Production at such heights would require OPEC to utilize spare capacity that has never been deployed before. To contextualize, a Y/Y change of 1.2 MMbbl/d is roughly equivalent to one full year of global oil demand growth based on the average pace observed over the past decade. This underscores the scale of potential supply adjustments and the strategic implications for OPEC’s production policy.

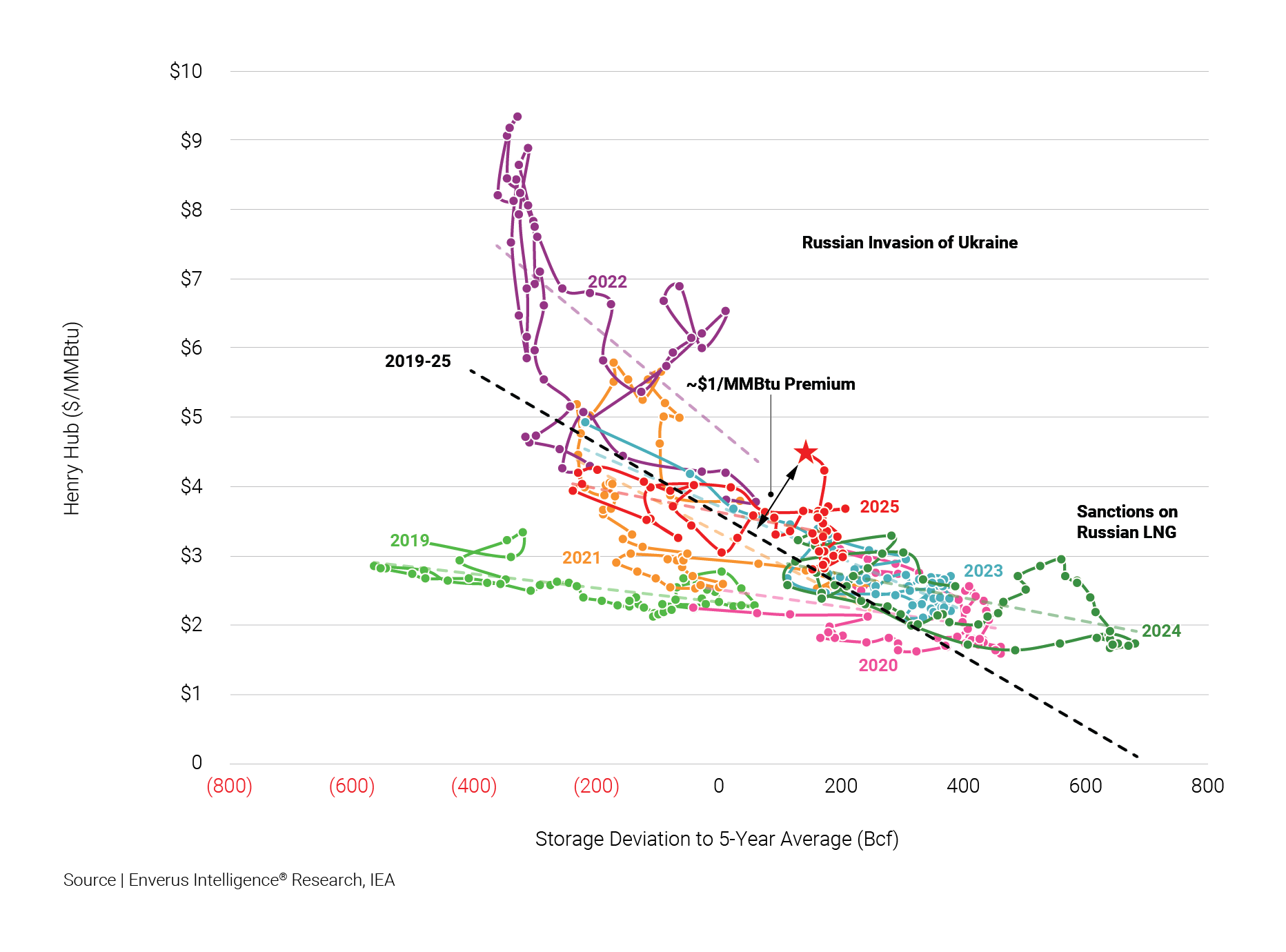

EIR projects HH prices to average $3.80/MMBtu through the winter months and $3.60/MMBtu during the summer, before gradually increasing to $4.00-$4.50/MMBtu by the end of the decade.

This outlook reflects several structural factors expected to limit the sustainability of recent price strength. Although prices at the trading hub surged by about $1.00/MMBtu in late October, driven by colder weather forecasts and record LNG export volumes, multiple dynamics point to ongoing market softness. L48 production remains highly elastic, with output growth exceeding expectations in response to price signals.

At the same time, gas-fired power generation is losing market share to coal at current elevated price levels, indicating demand-side weakness.

Additionally, weekly storage withdrawals have been lighter than weather patterns would suggest, and the current storage surplus of roughly 150 Bcf versus the five-year average is unlikely to be materially reduced given robust supply and muted demand.

Global upstream investment has fallen short of funding future oil and gas developments, leaving current projections pointing to significant supply shortages by the middle of next decade. Unlocking resources in Canada, Venezuela and Russia, currently constrained by geopolitical factors, will help ease this pressure. EIR expects these regions to make meaningful progress this year, improving supply expectations and partially mitigating future imbalances, though not enough to alter our bullish long-term outlook.

EIR identifies several catalysts likely to reset expectations in 2026, signaling long-term oversupply that will pressure independent power producers (IPPs) and utilities. We project that load growth in ERCOT and PJM will fall short of ISO estimates, forcing them to downgrade their inflated long-term forecasts. Utility reforms are crushing on-grid demand, and high barriers to entry, such as AEP Ohio’s policy change that reduced its queue ~55%, pushing data centers behind the meter. As a result, the market is effectively building new on-grid generation for load that has already moved off-grid.

While demand softens, PJM, MISO and SPP are fast-tracking dispatchable assets, and this influx of firm generation will likely result in higher reserve margins by 2030 than exist today . Meanwhile, investor pressure will cap demand. Hyperscalers are pushing the boundaries of cash flow-funded expansion, but we expect investors to resist overspending cash flow.

Demand for new baseload capacity, driven by accelerating load growth from data centers and electrification trends, has increased interest in both new-build and existing gas-fired generation assets. However, recent IPP earnings calls highlight significant cost inflation for new-build projects, with construction costs rising to $2-$3 million/MW, creating steep barriers to entry. Coupled with turbine delivery lead times of ~2.5 years and an additional two years for construction, new-build gas economics have become increasingly challenging for developers seeking to capitalize on near-term load growth.

As developers and IPPs face constraints in building the “bridge fuel,” M&A has emerged as a central theme in power markets, with existing assets positioned to benefit from wholesale price inflation. 2025 M&A activity underscores a clear trend: public IPPs, under investor pressure to monetize the load growth narrative, are acquiring assets from private owners seeking exits at elevated multiples.

EIR expects this trend to persist into 2026, supported by recent private equity transactions and IPP commentary on quarterly earnings calls. Deal values are likely to remain inflated at or above $1 million/MW, reflecting scarcity premiums for operational baseload capacity. However, we anticipate gas-fired acquisitions will play a diminishing role in driving IPP equity performance. Instead, investor focus is expected to shift toward the ability of IPPs to secure long-term power offtake agreements for their existing baseload fleets, positioning contracted assets as the primary determinant of valuation.

Recent policy shifts and tax credit repeals create a challenging environment for renewable project development, with solar and wind levelized cost of energy (LCOEs) doubling across certain regions. Pine Gate’s bankruptcy filing marks the first domino in what we expect to be a series of developer bankruptcies and divestiture announcements, signaling systemic stress in the sector. Financial liabilities for development projects are mounting, leaving renewable portfolios particularly vulnerable to policy volatility and shifting investor sentiment.

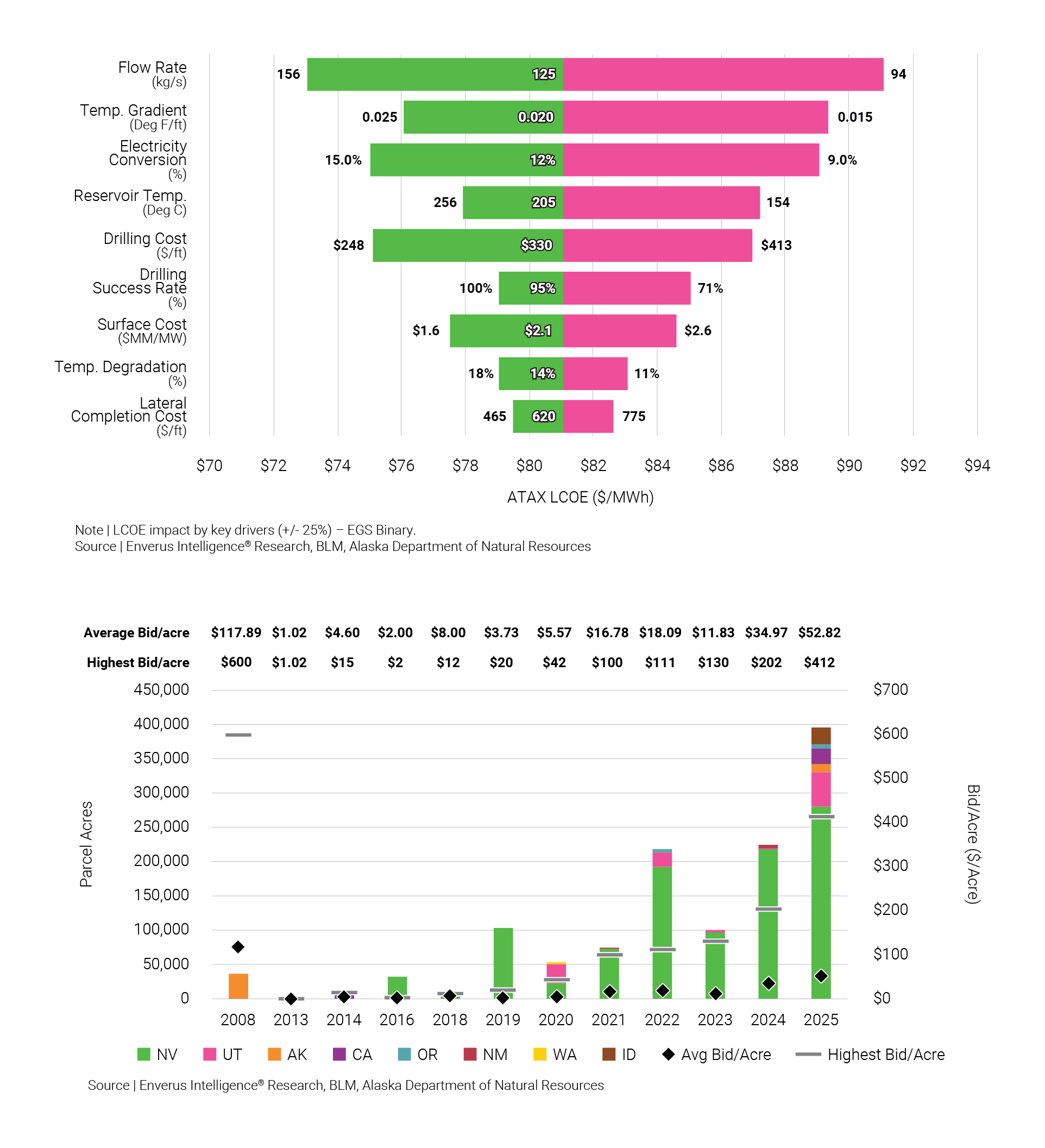

2026 will mark a pivotal transition for enhanced geothermal systems (EGS) and advanced geothermal systems (AGS), as commercial-scale projects are announced and others, like Fervo Energy’s Cape Station project, come online. This inflection point is driven by two converging factors: unprecedented load growth from AI data centers, creating a need for scalable, clean and reliable power; and key technological breakthroughs expanding the geologic and geographic viability of geothermal energy.

Supermajors will also announce involvement in EGS, with some exploring their own pilot projects, fueled by a significant overlap between their core competencies and EGS requirements. Oil and gas skills like advanced drilling techniques, subsurface characterization and large-scale project execution position these companies to capitalize on geothermal opportunities. Given the ability to leverage existing assets and expertise, EGS represents a complementary growth avenue for supermajors.

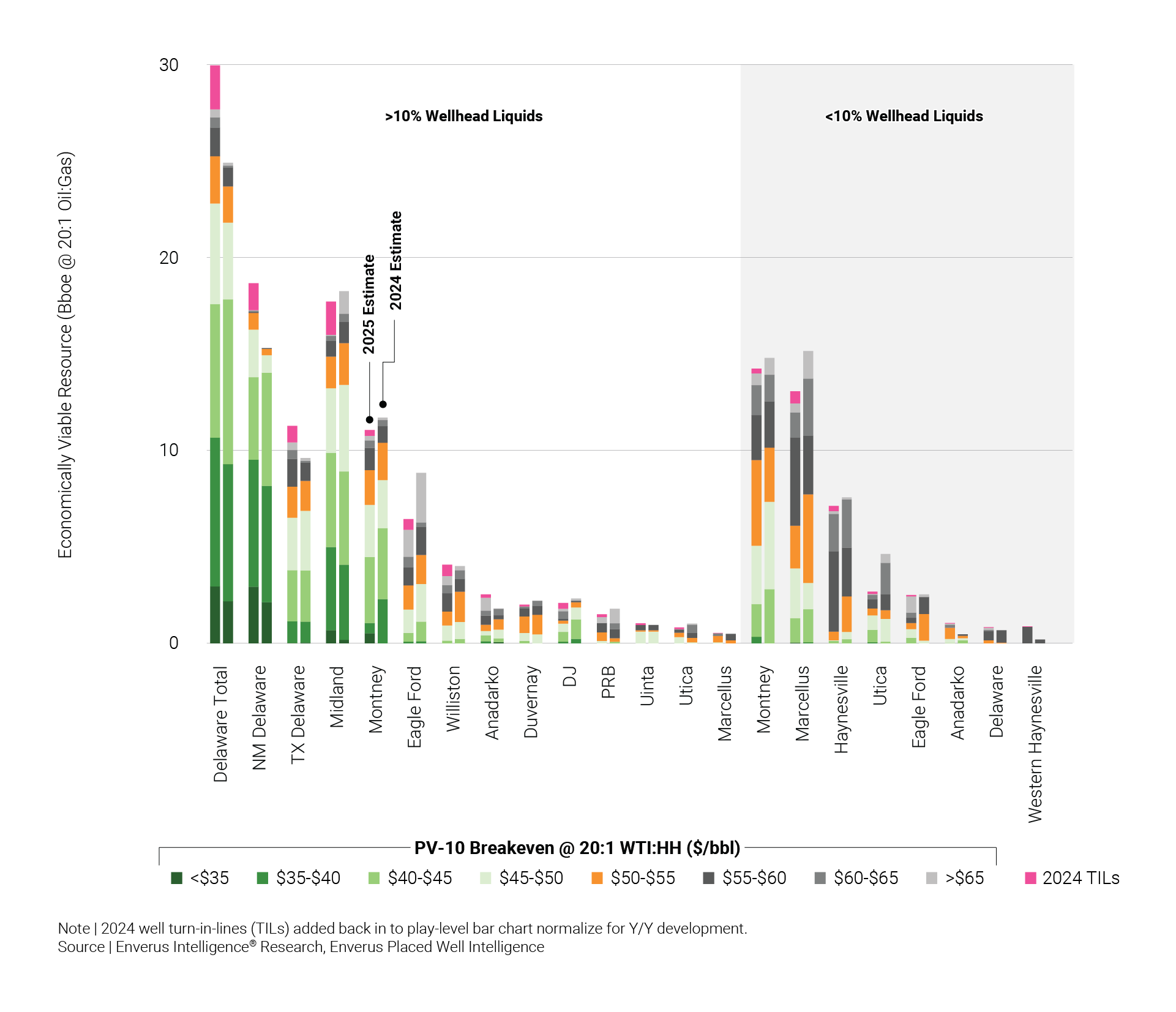

North American E&Ps are expected to accelerate the adoption of extended-reach drilling (ERD) in 2026 as a primary lever to preserve capital efficiency amid ongoing inventory quality erosion. Since 2022, performance data indicates minimal degradation in per-foot productivity for 3- and 4-mile laterals compared to 2-mile wells. This trend has driven a structural shift in development strategies: laterals of 3 miles or longer have increased from just 12% of total activity in 2022 to 29% in 2025, with WIPs suggesting further growth to 34%. This evolution underscores industry confidence in longer laterals as the most reliable mechanism for incremental recovery and cost optimization. In contrast, redevelopment activity remains stagnant at 2%-3%, offering little relief to the broader challenge of declining Tier 1 locations.

While chemical treatments and unconventional EOR have drawn recent headlines, their practical impact remains limited. Active unconventional EOR pilots are scarce, constrained by high capital requirements and scalability challenges. Chemical treatments are gaining traction as a low-capital optimization tool but remain largely confined to pilot programs. These technologies may eventually complement large-scale development strategies; however, they are unlikely to displace the dominance of ERD in the near term. Operators will require a diversified portfolio of technology levers to mitigate inventory degradation, but ERD stands out as the cornerstone for sustaining returns and operational efficiency.

Oil resource expansion through continued step-out delineation is expected to be most significant in the north-central Delaware Basin (Figure 25), with development focused on the Bone Spring, Upper Wolfcamp and Avalon benches. The recent increase in drilling island approvals has unlocked development opportunities across the Known Potash Leasing Area. This regulatory shift enables access to previously untapped acreage in these intervals, pushing development farther north and reinforcing the Delaware Basin’s role as a key growth engine.

In the Midland Basin, deep bench development is positioned for a breakout in 2026. About 20% of WIPs target these intervals, marking a 10 percentage point increase from 2025. Notably, the Barnett and Woodford formations delivered oil recoveries near 60 Mbbl/1,000’ in 2025, exceeding the play average by more than 35%. Key areas to monitor include elevated activity in Crane County and farther extensions into the Midland Basin proper, signaling a structural shift toward deeper, largely unimpaired zones.

Gas resource expansion will concentrate in deep, productive Gulf Coast areas. The Western Haynesville will lead economic inventory additions, followed by West Eagle Ford and South Haynesville operators. Drilling efficiency in these regions surged in 2025 with cycle times improving 20%-30% from high- horsepower rigs and insulated drill pipe. These advancements will continue to drive down well costs and breakevens, converting previously high-risk, capital-intensive prospects into scalable, economic inventory.

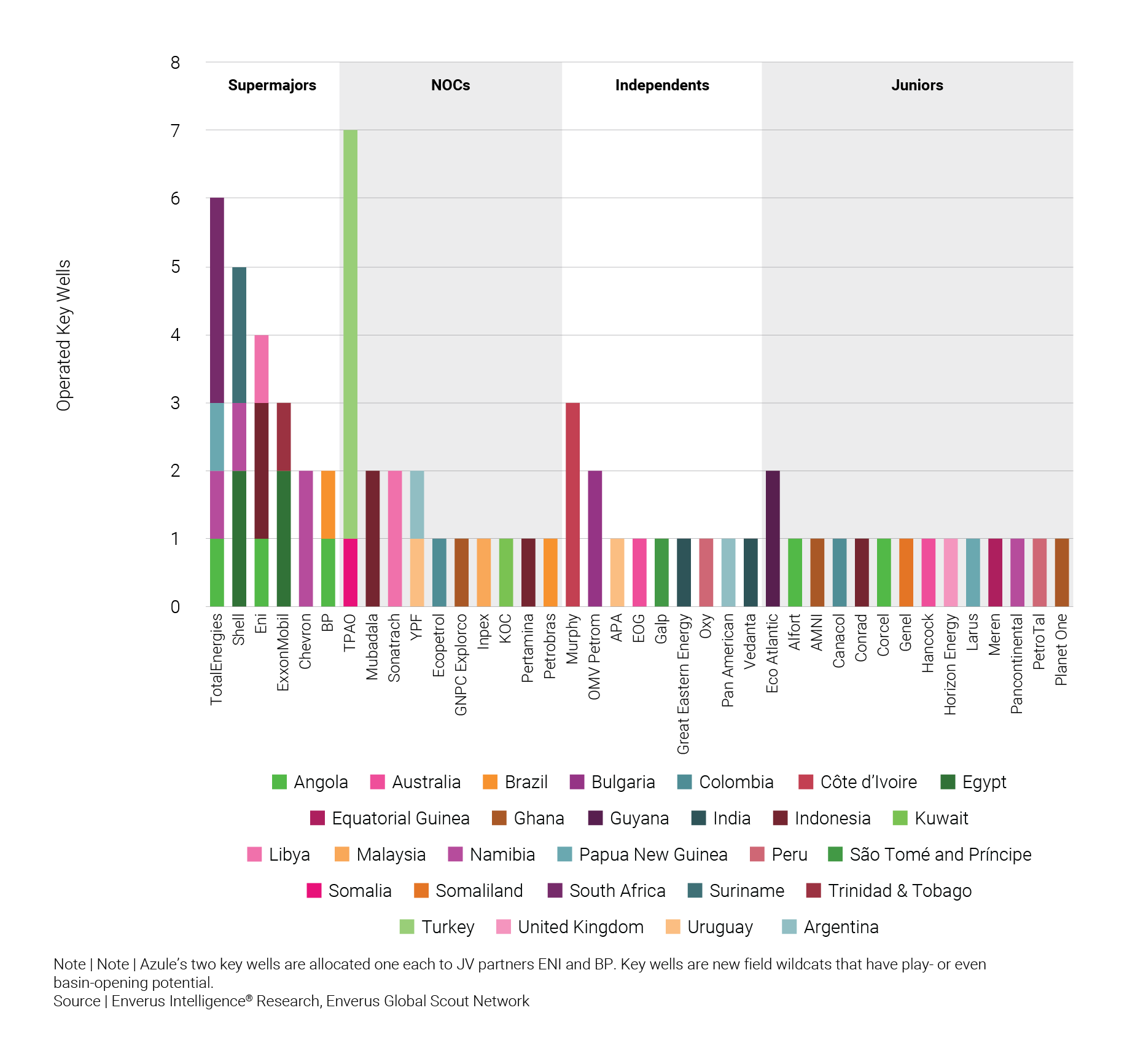

Planned high-impact exploration drilling activity for the upcoming year remains broadly consistent with last year’s levels, signaling continued commitment to frontier and deepwater opportunities. The portfolio is dominated by prospects in Angola, Egypt, Namibia, Indonesia and Turkey, underscoring the strategic importance of African basins in frontier exploration programs.

If activity proceeds as scheduled, we anticipate the long-awaited return of exploration capital to independents and junior operators. This shift marks a notable departure from recent years, in which supermajors led most high-impact campaigns. In fact, supermajors account for only 30% of planned key wells, down from 40% in our 2025 and 2024 outlooks, highlighting their relative decline.

However, supermajors should not be discounted. We expect them to rebuild high-impact exploration drilling inventories over the next several years, leveraging significant acreage acquisitions in new countries in 2025. These moves position them to reassert leadership in frontier exploration as global energy demand evolves.

We expect private capital to increase its share of North American upstream acquisitions in 2026. From 2023-25, only $17 billion of public company assets transitioned into private hands, compared to more than $100 billion in acquisitions of private E&Ps by public operators. This imbalance is expected to shift as U.S. oil-focused E&Ps lead a wave of asset divestments amid strong M&A pricing that continues to outpace equity market valuations. Recent transactions, such as Stone Ridge-ConocoPhillips, demonstrate upside value underwriting despite inventory averaging breakevens above $50/bbl. Paying for inventory that is less competitive for capital allocation reflects a broader effort to mitigate resource scarcity concerns in a lower crude price environment.

Private capital is well positioned to exploit these opportunities. In addition to 14 new private equity portfolio companies funded in 2025, the emergence of asset-backed securitization has expanded the buyer pool. The Anadarko and Williston basins screen as the most likely targets for liquids-focused divestments. While Permian inventory is expected to remain tightly held, potential non-core asset sales cannot be ruled out.

In Canada, the case for non-core asset sales is less compelling because deal valuations remain aligned with equity market pricing. Activity is expected to be driven by corporate consolidation rather than asset-level transactions. Similarly, U.S. gas deals are pricing closer to equity valuations, although strong buyer interest from both domestic and international groups may exert upward pressure on values.

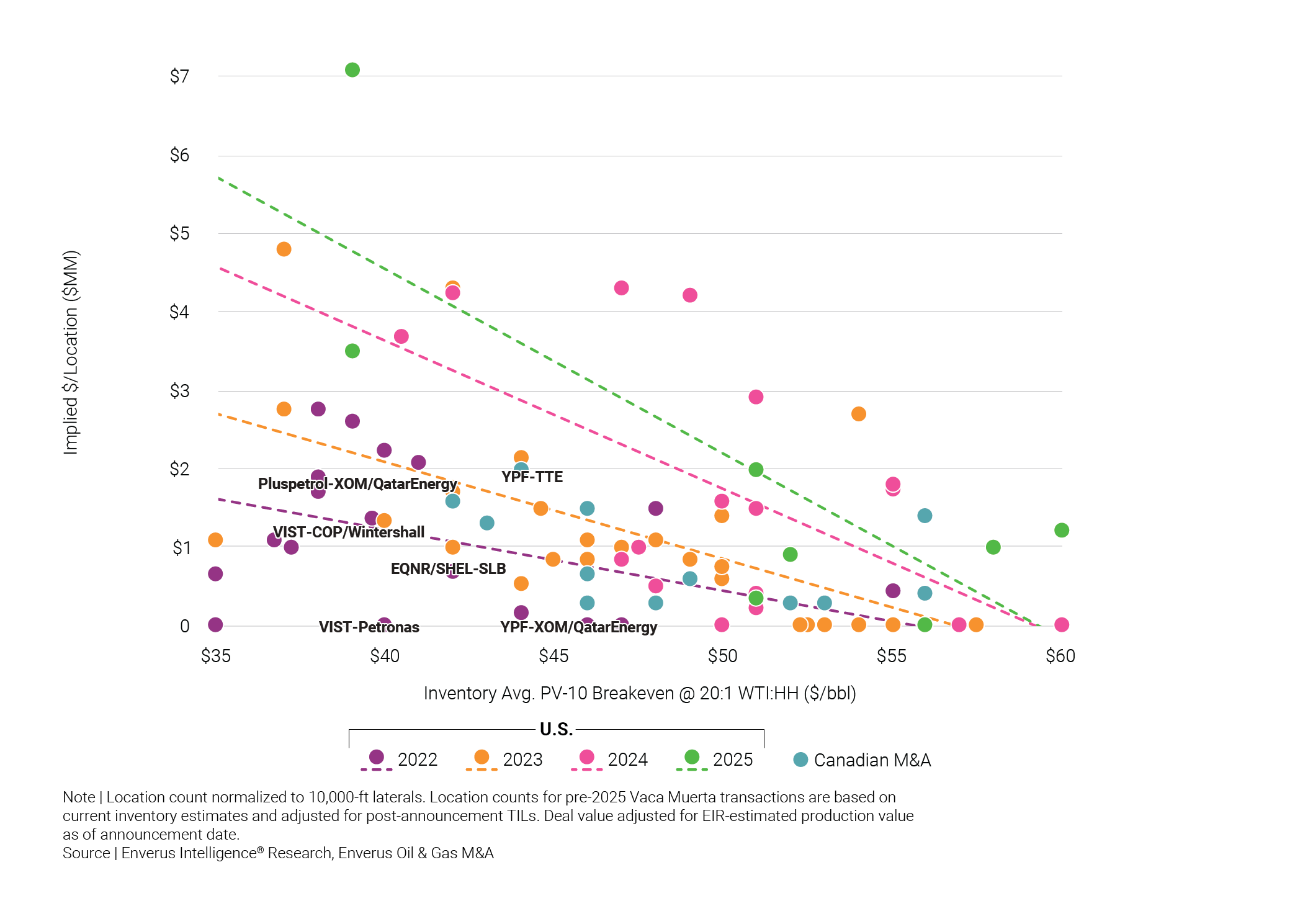

Recent transactions in Argentina’s Vaca Muerta shale play have screened at surprisingly low valuations. Across six major deals completed over the past two years, we estimate none traded for more than $2 million per undeveloped location. This stands in sharp contrast to North American shale transactions, where low-breakeven inventory has consistently commanded significantly higher valuations in recent years.

The most common explanation for this discount is perceived above-ground risk in Argentina. The recent announcement by Continental Resources of its first Vaca Muerta acquisition marks the entry of a U.S.-focused shale company into the play and signals growing interest from North American E&Ps seeking inventory diversification. Although transaction terms were not disclosed, this development suggests the Vaca Muerta is increasingly viewed as a strategic growth opportunity.

Looking ahead, we expect deal activity to accelerate, supported by three key factors: rising demand from inventory-constrained North American producers, pro-industry regulatory tailwinds in Argentina and early exits from some of the play’s more willing sellers. These dynamics point to upward pressure on valuations and a narrowing of the gap with economically comparable North American inventory. Specifically, sellers are likely to seek more than $0-$2 million per location for sub-$45 breakeven inventory, reflecting improved market confidence and competitive bidding.

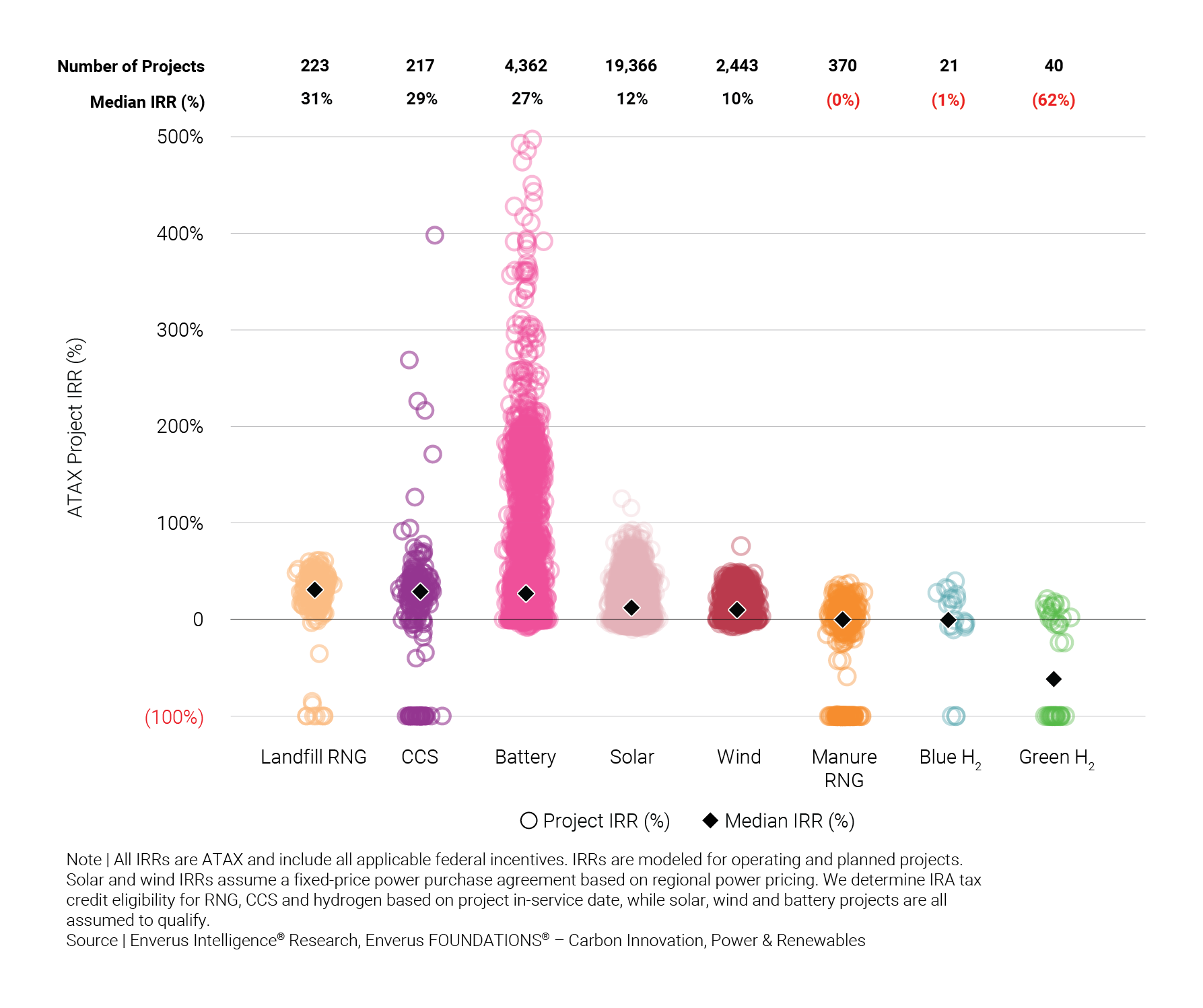

Oil and gas companies are recalibrating transition strategies as capital shifts back toward higher-return fossil fuel projects. Earlier in 2025, BP reduced annual transition spending by $5 billion, while XOM cut its 2025-30 low-carbon budget by one-third to $20 billion. These reductions are expected to redirect remaining capital toward proven, higher-margin segments such as landfill RNG and CCS projects, while slowing investment in costlier or less mature technologies like hydrogen and manure-based RNG.

Landfill RNG projects currently deliver median after-tax (ATAX) IRRs of 31%, supported by a stable D3 RIN pricing outlook through 2028. Recently introduced feedstock restrictions are expected to have minimal impact on biogas economics, in contrast to biomass-based diesel, where imports account for roughly half of all volumes. Renewable diesel and biodiesel operators with strong domestic feedstock positions remain well positioned, while those reliant on global supply chains face mounting headwinds.

CCS projects in the U.S. generate a median IRR of 29%, with variability driven by geological quality and capture processes. Permanent sequestration is projected to reach 11.5 mtpa by the end of 2026, split between 8 mtpa from Class VI wells and 3.5 mtpa from Class II wells, as the OBBBA enhances certainty, primacy accelerates Class VI permitting and CCS policy frameworks continue to solidify.

By contrast, hydrogen and manure-based RNG face a weaker outlook. Unclear demand signals and rolled-back incentives are likely to accelerate hydrogen project cancellations into 2026. Manure RNG operators contend with fragmented supply chains and heightened exposure to volatile LCFS pricing, which in some cases drives returns below zero. We expect investment in these segments to remain muted until credit markets stabilize.

The 2026 energy landscape, as explored in this outlook, is undeniably complex and dynamic, marked by repriced oil and gas markets, power systems grappling with the demands of AI and electrification, an upstream sector innovating to maximize resources, and capital flows becoming increasingly selective. Navigating these multifaceted forces requires deep, data-driven insights. To fully unlock the comprehensive analysis and strategic intelligence presented in this report, along with our entire collection of in-depth energy research, we invite you to discover the benefits of subscribing to Enverus Intelligence® Research (EIR).

Advanced grid insights with accurate load forecasts and extensive monitoring enhance trade execution and profitability.

Quickly identify grid opportunities and risks with high-quality mid-term forecasts, expert analysis and streamlined grid analysis.

Confidently shape your investment strategy, identify optimal power asset locations and optimize utility scale PV project profitability—all in minutes.

With Enverus Instant Analyst™, you receive answers you can trust, delivered in seconds. Sourcing from 25+ years of vetted data and research on the most trusted SaaS platform designed exclusively for energy.

Confidently shape your investment strategy, identify optimal power asset locations and optimize utility scale PV project profitability—all in minutes.

Arm yourself with the knowledge to inform strategic decisions and grow your business with one source for insights across oil and gas, renewables, carbon capture and ESG.

Design PV Plants & Battery Storage Systems 90% Faster with Our Advanced Solar & Battery Software.

SUGAR™ helps grid operators and utilities manage increasing interconnection queue volumes by accelerating modeling and simulation studies, with up to 2x reduction in time-consuming study processes.

Unlock returns of electron and molecule-based energy transition technologies with deal insights, from power generation assets to CCUS and hydrogen.

Tune out the noise, get unbiased evaluations and uncover hidden opportunities with advice you can trust from experienced energy and power intelligence advisors.

Comprehensive coverage of power markets and insights into emerging energy technologies and project economics.

Interconnect offers developers certainty throughout the interconnection lifecycle, providing scenario analysis and risk assessment capabilities to improve the chances of deploying new projects.

Let’s get started!

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Ready to Subscribe?

Ready to Get Started?

Ready to Subscribe?

Sign Up

Power Your Insights