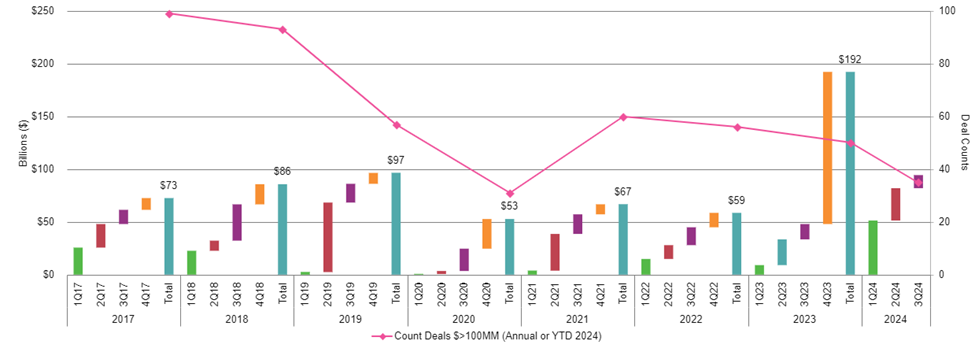

The third quarter of 2024 saw a modest $12.4 billion in U.S. upstream M&A activity, reflecting a cooling-off period in the energy market. This figure marks a significant slowdown in deal value compared to recent years and highlights shifting dynamics across the energy landscape. However, despite this decline, the quarter also unveiled exciting new trends that could reshape the upstream sector in the future.

Deal Value and Geographic Diversity

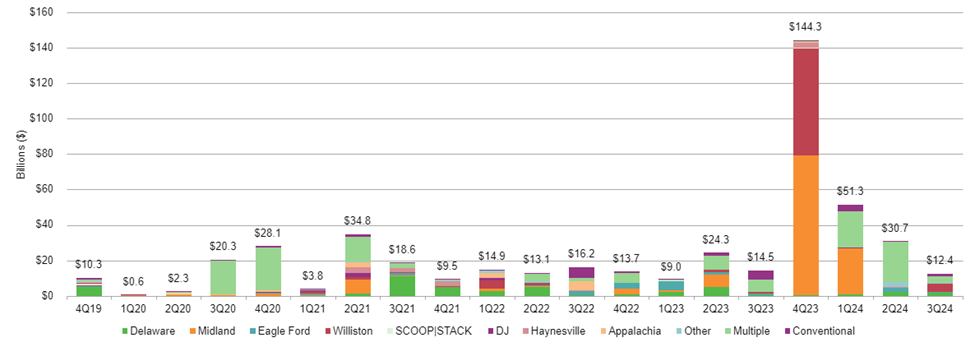

M&A activity in Q3 2024 was geographically diverse, with the Williston Basin taking the lead with $5 billion in deal value, followed by the Delaware Basin at $1.9 billion. This marks a notable shift away from the Permian Basin, which had previously dominated M&A activity. As assets in the Permian become increasingly expensive and opportunities scarcer, companies are broadening their focus to other less consolidated or less expensive plays like the Eagle Ford and Williston Basin.

Beyond-Permian Momentum: Broadening Horizons

The shift in focus beyond the Permian underscores a new trend in the energy sector: buyers are targeting assets outside of core active Permian plays. Elevated pricing in the Delaware and Midland basins has made inventory harder to come by, pushing public companies to explore alternative opportunities. This broadening horizon has led to increased interest in other basins, where companies can still find attractive assets with reasonable pricing.

For instance, Devon Energy’s $5 billion acquisition of Grayson Mill Energy in the Williston Basin was the largest deal of the quarter. The transaction valued Grayson Mill’s assets at $1.6 million per location, highlighting the strategic value of scalable assets with breakeven prices around $50/bbl WTI. This kind of deal exemplifies the willingness of public companies to pay for inventory that provides scale and potential operational synergies, even if it has higher breakevens than core Permian inventory.

Pricing Trends: A Shift Toward Less-Proven Assets

Another key trend emerging in the last two quarters is the growing willingness of buyers to assign value to less proven assets. As inventory prices rise in core basins, companies are increasingly open to assets in less explored areas or with less current horizontal development. This shift could unlock opportunities in regions previously overlooked like the Uinta Basin and Utica Oil Window, providing a new avenue for growth in the sector.

Private Equity: A Steady Source of Opportunity

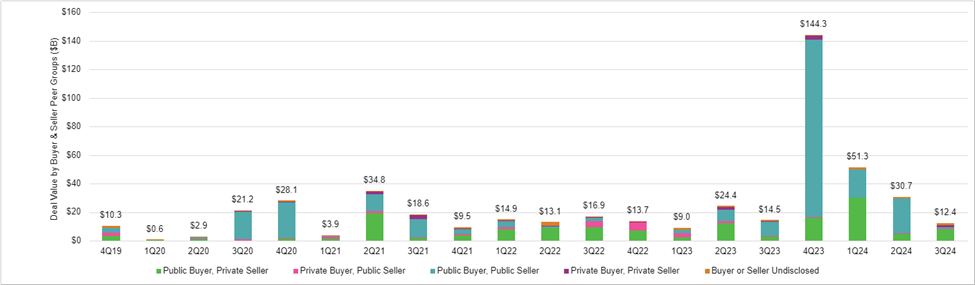

While public company consolidation took center stage in past quarters, Q3 2024 saw renewed interest in acquiring private equity-backed companies. Approximately 65% of total deal value came from private-to-public transactions, with public companies picking up portfolio assets from private equity firms. Private equity is also raising and redeploying fresh capital activity indicates ongoing capital availability for energy sector investments. That includes acquiring private assets in areas not receiving interest from public companies like the SCOOP|STACK and Piceance Basin.

Emerging Opportunities: SMID-Cap Urgency

As companies focus on maintaining capital efficiency, we can expect to see more modest sized in-basin transactions and bolt-on acquisitions from companies seeking to avoid drilling lower quality inventory, with SMID-cap companies leading the way. With a significant delta between current development costs and remaining inventory breakevens, these companies are highly motivated to secure deals with even modest remaining inventory to maintain operational efficiency.

Implications for the Energy Sector

- Diversification of M&A activity The shift beyond the Permian suggests a maturing market, where companies are actively seeking growth opportunities in secondary basins.

- Risk appetite: Buyers’ willingness to value less proven assets points to a potential shift in risk tolerance, which could lead to the development of previously overlooked resources.

- Private equity influence: The continued involvement of private equity signals ongoing interest in upstream investments, even as public company consolidation remains in focus.

- Global gas market impact: Interest in gas assets for LNG supply reflects the growing importance of the global gas market in shaping M&A activity.

These trends highlight the dynamic and evolving nature of the upstream M&A landscape. As the sector adjusts to changing market conditions, companies will need to remain agile, strategic, and well-informed to capitalize on emerging opportunities.

Get Ahead of the Market with Enverus Intelligence

In an industry that’s rapidly evolving, the need for accurate, real-time insights has never been more critical. Enverus Intelligence provides the data-driven tools and analysis you need to navigate today’s shifting market with confidence. Whether you’re tracking the latest M&A trends or evaluating potential deals, our intelligence offering helps you stay ahead of the competition.

Interested in Staying Ahead of the Curve?

Discover how Enverus Intelligence can help you uncover new opportunities and make informed, strategic decisions in a fast-changing energy landscape.

Maximize Your Potential With Enverus

Our cutting-edge intelligence tools empower you to understand market trends, assess risks and identify opportunities before your competitors. Start making data-driven decisions with confidence. Start your journey with Enverus Intelligence now.

Start your journey with Enverus Intelligence® now.

About Enverus Intelligence®| Research

Enverus Intelligence® | Research, Inc. (EIR) is a subsidiary of Enverus that publishes energy-sector research focused on the oil, natural gas, power and renewable industries. EIR publishes reports including asset and company valuations, resource assessments, technical evaluations, and macro-economic forecasts and helps make intelligent connections for energy industry participants, service companies, and capital providers worldwide. See additional disclosures here.