[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories posted an increase of 1.1 MMBbl last week, according to the weekly EIA report. Gasoline and distillate inventories increased 0.8 MMBbl and 0.4 MMBbl, respectively. Total petroleum inventories increased 0.9 MMBbl. US crude oil production was flat week over week, per EIA, while crude oil imports were up 0.3 MMBbl/d, to an average of 7.1 MMBbl/d.

- The WTI market opened with a large gap between the previous Friday’s close and the open late Sunday night. The strength of the rally was expected as traders assessed the immediate and longer-term impact of the Iranian attack on the Abqaiq plant and fields, which limited production to 5.7 MMBbl/d. Prices then spent the rest of the week understanding the time period for Saudi to recoup the supply loss, with some hoping that the production would be restored by the end of the month. Time will tell whether those hopes are accurate, but the production will be coming back to the market at some point.

- The attacks are going to have a long-lasting effect on crude oil prices, regardless of the production coming back, and are likely to cause a higher risk premium to prices based on the regional political instability. It is also remarkable that the Saudis were unable to deter the attack with defense measures. These two elements will likely provide a bid to prices over time regardless of the continuing global economic concerns and tariff discussion between the US and China.

- The CFTC report released Friday (dated September 17) brought little change to the speculative positions regardless of the attacks. The Managed Money long sector (speculating on higher prices) added just 3,993 contracts, while the short position decreased 2,333 contracts. This lack of position bias by either the bullish or bearish camps suggests the market is undecided as to the immediate directional effect the attacks will have.

- After the initial run on Monday, which established the highs for the week at $63.38, WTI spent the remainder of the week retracing a portion of the gains from the previous week’s close ($54.85). The weakness in prices during the week is not a bullish indicator, but as discussed, the success and lack of defensive tactics regarding the attacks are likely to provide a base for prices. While the geopolitical issues surrounding the region have always provided some risk for prices, that risk premium will increase in the near-term. Market internals last week had developed a slightly positive bias as prices rallied and held some of the gains into the close on Friday, while weekly volume was at the highest level in three years. Open interest declined during the week, which is not surprising with the expiration process of the prompt contract.

- WTI will begin developing a series of new ranges for prices with the weekly close from two weeks ago ($54.85) establishing the low side of the new range and the highs from last week ($63.58) providing the high end. Additional sub-ranges may develop in the next few weeks as the market confirms the return of production from the Saudi facilities and learns what retribution (if any) will occur for the attacks. Due to the unknown nature of the retaliation and what further responses will come from Iran, the market has the potential for extreme volatility over the coming weeks.

NATURAL GAS

- Natural gas dry production declined 0.42 Bcf/d last week, while Canadian imports decreased 0.15 Bcf/d.

- Res/Com demand gained 0.14 Bcf/d while power demand dropped 2.58 Bcf/d, as more seasonal temperatures are developing in the Lower 48. Industrial demand fell from the week before, dropping 0.20 Bcf/d. LNG exports gained 0.50 Bcf/d from the previous week, mainly due to increased exports out of Sabine Pass, while Mexican exports increased 0.08 Bcf/d.

- These events left the totals for the week showing the market dropping 0.57 Bcf/d in total supply, while total demand dropped 2.16 Bcf/d.

- The storage report last week showed the injections for the previous week at 84 Bcf. Total inventories are now 393 Bcf higher than last year and 75 Bcf below the five-year average. Current weather forecasts in the near-term (coming week) show above- to well-above-average temperatures from the Rockies to the east, and further out forecasts have a similar profile. This above-average profile will not have a dramatic effect as the market heads into late fall and seasonal temperatures, which are lower than peak summer temperatures.

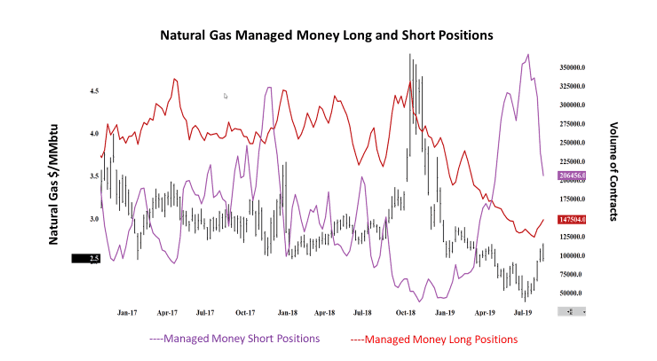

- The CFTC report released last week (dated September 17) provides significant information explaining the recent gains in prices. The Managed Money short position covered their short exposure by buying back 30,358 contracts. The chart below shows the dramatic reduction in short positions and the price actions while those shorts were covering.

- Over the last three weeks, the speculative short position has been reduced by more than a third compared with the total short position held in August. There is little evidence for what started the exodus (fundamentally) other than the annual tendency for prices to rise going into the winter period.

- With the price declines last week, the market internals maintain a neutral/bullish bias. Volume declined week over week, and so did open interest (according to preliminary data from the CME). If the declines in prices were associated with additional short interest expecting lower prices, the total open interest should have increased week over week. This relationship may be muddled slightly due to the expiring October contract.

- Prices will now test an area that provided significant buying from 2016 through early 2019. The area around $2.50 held until the breakdown in late May, which set up the test of $2.00 during August. Expect this area to be tested this coming week; should it break down again, prices are likely headed back to the low $2.30s. If prices can garner the support, then the highs of last week ($2.71) will come into play.

NATURAL GAS LIQUIDS

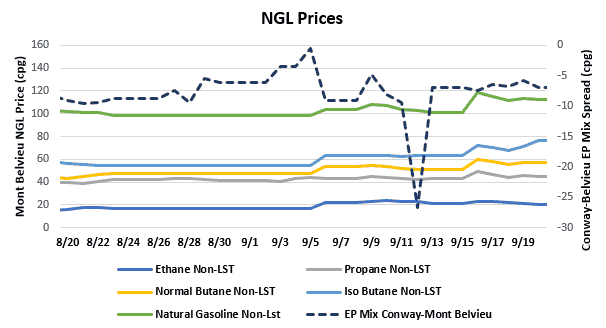

- Ethane was down $0.009 to $0.219, propane was up $0.029 to $0.463, normal butane was up $0.050 to $0.575, isobutane was up $0.084 to $0.715, and natural gasoline was up $0.098 to $1.143.

- US propane stocks increased ~2.93 MMBbl for the week ending September 13. Stocks now sit at 100.69 MMBbl, roughly 25.94 MMBbl and 19.89 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

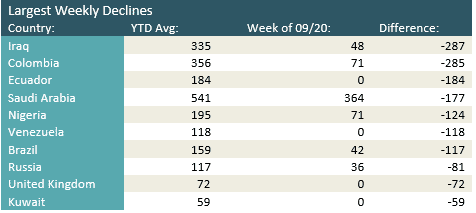

- US waterborne imports of crude oil fell for the week ending September 20, 2019, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of September 23, aggregated data from customs manifests suggested that overall waterborne imports decreased by 1.12 MMBbl/d from the previous week. All PADDs saw a decline in imports, with PADD 1 down by 440 MBbl/d, PADD 3 down by roughly 550 MBbl/d and PADD 5 down by 130 MBbl/d. Waterborne imports to PADD 3 are showing a sub-1 MMBbl/d for the first time since February.

- The decline in imports was due to lower than average imports from Iraq, Colombia, and Ecuador. US imports from Iraq have averaged 335 MBbl/d in 2019, but fell to 48 MBbl/d for this week — all of which went to PADD 5. Imports from Colombia have averaged 356 MBbl/d, but fell to 71 MBbl/d for the week. Imports from Ecuador have averaged 184 MBbl/d, but fell to 0 for the week.