[contextly_auto_sidebar]

CRUDE OIL

- U.S. crude oil inventories decreased by 1.7 MMBbl last week, according to the weekly EIA report. Gasoline and distillate inventories decreased 3.1 MMBbl and 2.7 MMBbl, respectively. Total petroleum inventories posted a substantial decline of 9.0 MMBbl. U.S. crude oil production was unchanged from the previous week, per the EIA, while crude oil imports were down 0.44 MMBbl/d to an average of 5.9 MMBbl/d.

- WTI prices spent the week gaining on the expectations of OPEC+ increasing the production cuts at the upcoming meeting in early December. Saudi Arabia has not committed to this strategy of making additional cuts until some members (Iraq and Nigeria) come into full compliance with the cuts that had previously been agreed upon.

- Additional support came from the news that China has increased its crude oil import quotas for independent refiners. This latest announcement will have total quotas awarded in 2019 at 3.3 MMBbl/d, up nearly 0.3 MMBbl/d as compared to quotas awarded during the full year 2018. Rarely do Chinese independent refiners allow crude import quotas to go unused as it affects the government’s computation of future quota awards.

- The week’s strength in WTI was impressive and left the contract at the highest weekly close since September, and the market continues to limit rallies on the geopolitical economy concerns about growth. The IMF (International Monetary Fund) expects economic growth in Asia to slow, and it adjusted its projections to 5% in 2019 and 5.1% in 2020. This represents a 0.4% decline in 2019 and a 0.3% decline in 2020. The WTI market reflects the concerns about growth in 2020 as the monthly contract prices trade at a discount to the December and January contracts in 2020.

- The CFTC report released Friday (showing positions from October 22) showed a slight adjustment in the trader’s expectations as the Managed Money long sector added 18,752 contracts, while the Managed Money short positions increased positions by 9,362 contracts. The gains in both of the speculative sectors continue to reflect the indecision of the current market direction, and this tug-of-war between the sectors is likely to continue.

- Market internals last week developed a more neutral bias with prices closing at recent highs. Those highs were met with lower volume and a loss in open interest.

- Prices started strong and maintained that direction all week. They closed the week above the tested resistance area above $56.00 and will likely find some follow-through strength to open this week. The lack of volume during the rallies brings a momentum question to additional gains. The commonly traded 200-day average is just above last week’s close at $57.02, and then the highs from late September at $58.49-$59.39 will find additional selling. Declines to last week’s low at $55.60 and the key area of $55.00-$53.00 will likely find buying.

NATURAL GAS

- Natural gas dry production increased 0.84 Bcf/d last week, while Canadian imports decreased by 0.21 Bcf/d.

- Res/Com demand increased 0.02 Bcf/d, while power demand increased 0.53 Bcf/d, and industrial demand declined 0.09 Bcf/d. LNG exports gained 0.52 Bcf/d on the week, while Mexican exports decreased 0.13 Bcf/d.

- These events left the totals for the week showing the market gaining 0.63 Bcf/d in total supply while total demand increased by 0.90 Bcf/d.

- The storage report last week showed injections for the previous week at 87 Bcf. Total inventories are now 519 Bcf higher than last year and 28 Bcf above the five-year average. Current weather forecasts from NOAA in the near term (coming week) have below-average temperatures throughout the nation (including the Texas area), with exceptions in California and Florida. The eight- to 14-day forecast has below-average temperatures continuing in most of the lower 48, but it shows above-average temperatures in the Deep Southeast, Florida, and California.

- The CFTC report that was released last week (dated October 22) showed further expansion of the Managed Money short position, adding 19,250 contracts, while Managed Money long positions increased by 1,459 contracts.

- Prices started with weakness and spent the rest of the week building back support. Market internals now have developed a neutral bias as the market gained during the course of the week, but with a slight reduction in total open interest (according to preliminary data from the CME). If the market is to develop a positive or bullish bias going into the winter, rallies higher will need gains in volume and open interest.

- The market continues to be in a range environment ($2.18 to $2.39). Weather forecasts may provide strength in the coming week with the colder temperatures. However, extended strength in prices will need winter forecasts supporting demand into December. Should the current forecast trend continue to support heating demand, there is the potential for some volatility as the speculative short position is forced to cover. Should the forecasts adjust warmer, the declines will extend below the $2.18 area, and they may even go down to $2.12.

NATURAL GAS LIQUIDS

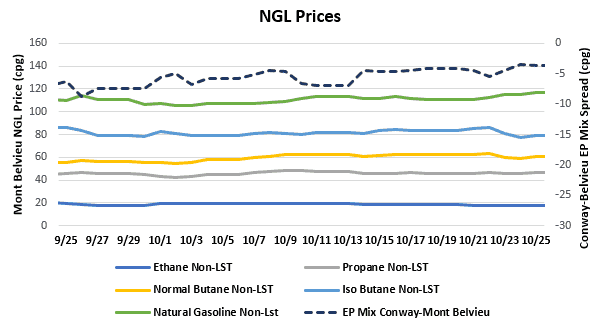

- Enterprise stated in their 3Q2019 earnings release that the Front Range pipeline will ramp up to 225 MBbl/d in 2021, up ~63 MBbl/d. Additionally, Front Range’s interconnect, Texas Express, will also receive an uptick in capacity, reaching ~330 MBbl/d in 2022, up ~44 MBbl/d. These pipeline expansions will allow more y-grade produced in the Rockies to reach Mont Belvieu.

- Ethane was down $0.005 to $0.179, propane was flat on the week, normal butane was down $0.010 to $0.610, isobutane was down $0.016 to $0.816, and natural gasoline was up $0.023 to $1.141.

- U.S. propane stocks fell ~461 MBbl for the week ending October 18. Stocks now sit at 99.99 MMBbl, roughly 17.99 MMBbl and 22.37 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

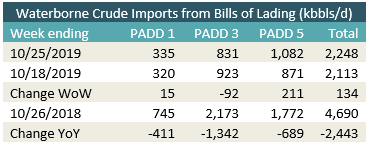

- We were expecting a low import number on last week’s import report, as that’s what the customs manifests were indicating, and the EIA did not disappoint. Weekly U.S. imports were reported at 5.857 MMBbl/d, the lowest level since February 1996. The EIA reported PADD 3 crude imports at their lowest level since the agency began reporting that level of detail in 1990. Looking forward to this week’s report, it appears that U.S. waterborne imports for the week ending on the 25th rose slightly, according to our analysis of manifests from U.S. Customs and Border Protection. As of October 14, aggregated data from customs manifests suggested that overall waterborne imports rose by 134 MBbl/d. In PADD 3, imports actually appear to have decreased, down 92 MBbl/d from the previous week. PADD 1 and PADD 5 increased their imports, up by 15 MBbl/d and 211 MBbl/d respectively.

-

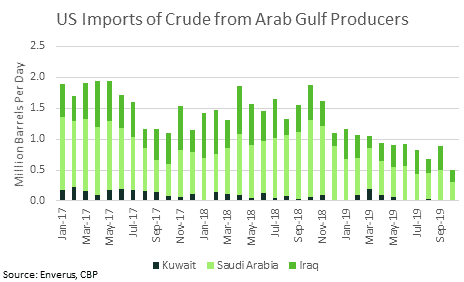

As we approach the end of October, we are seeing lower imports from all the major Persian Gulf producers. Iraq will see one of the lowest levels we’ve seen over the past 2 years, around 190k bbls/d right now. Imports from Saudi Arabia are also very low, just above 300k bbls/d. The current low since 2017 is 417k bbls/d. The US has not imported Kuwait crude since August.