On Feb. 3, a Wall Street Journal opinion piece titled, “Oil Frackers Brace for End of the U.S. Shale Boom,” took a hard look at major shale players’ remaining inventory of quality drilling locations.

The gist of the piece was that major shale operators — no matter what basin they’re operating in — have a limited number of economic locations they can drill. As a result, they are slowing drilling to avoid depleting remaining reserves too quickly, or within the next five to 10 years.

What struck me about the piece was its limited perspective. Namely, it ignores the fact that oil and gas basins have more than one producing reservoir.

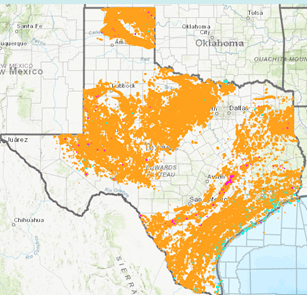

The map of Texas below shows all wells that were drilled with a first production date before Dec. 1, 1980, prior to the unconventional boom.

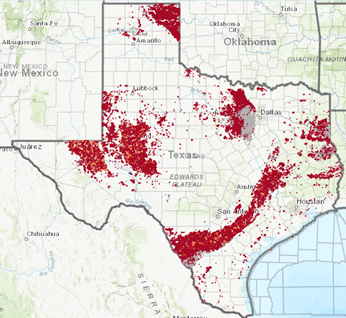

If we look next at the horizontal wells that have been drilled in Texas alone from 2000-present, one thing is clear — these unconventional wells have been drilled in fairways with plenty of conventional production.

The above map shows 84,895 horizontals, and nearly all of them — except the eastern Austin Chalk/Woodbine wells in Polk, Tyler, Jasper and Newton Counties — have been drilled in areas of adequate to excellent conventional production.

Nearly 85,000 new well logs have been added to our store of knowledge about Texas’ subsurface. Given the astounding number of line miles of seismic that have been shot to tease out the fracturing, surface curvature and petrophysical characteristics of formations like the Eagle Ford or the Wolfcamp, it’s a sure bet that there are more tools than ever in our exploration arsenal to find attractive new conventional field or field extensions.

The rewards are there.

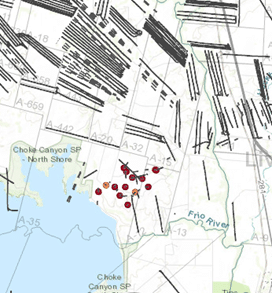

Consider my favorite example, Pioneer’s discovery of Sinor Nest field in Live Oak County.

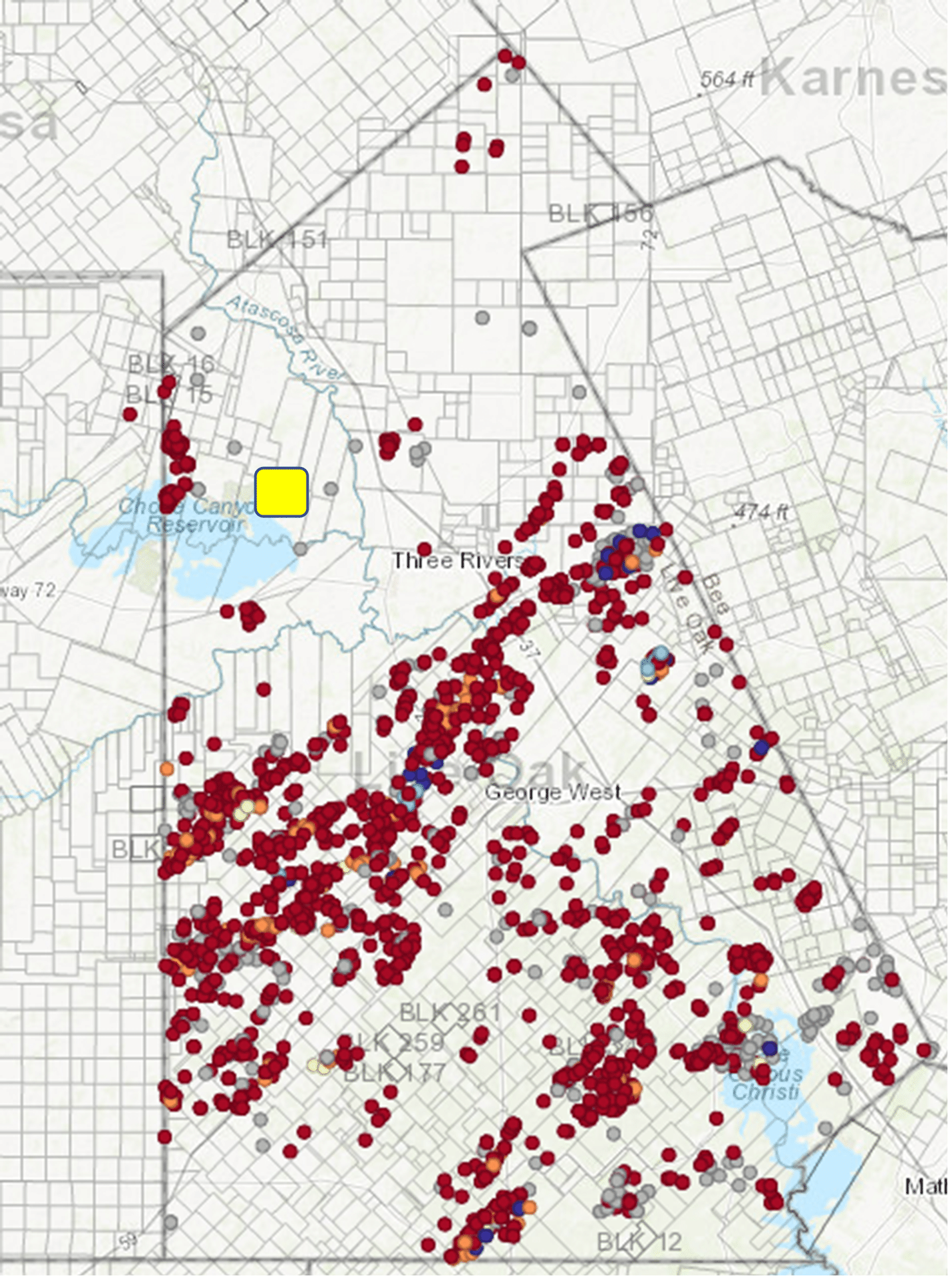

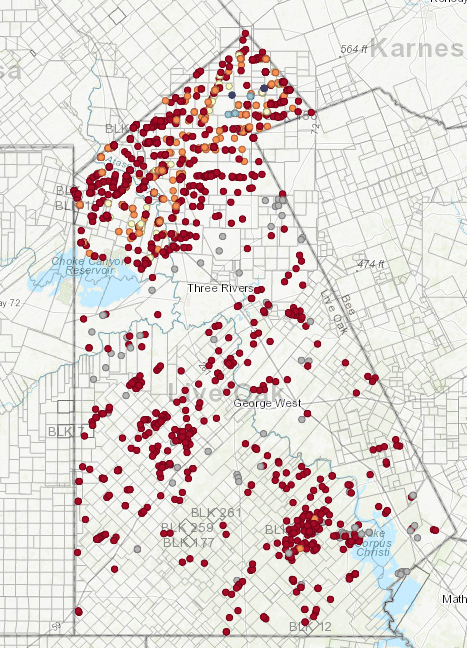

The following map shows vertical wells with first production dates that precede the Eagle Ford boom. The northern part of the county was sparsely explored.

That changed with the burgeoning Eagle Ford expansion.

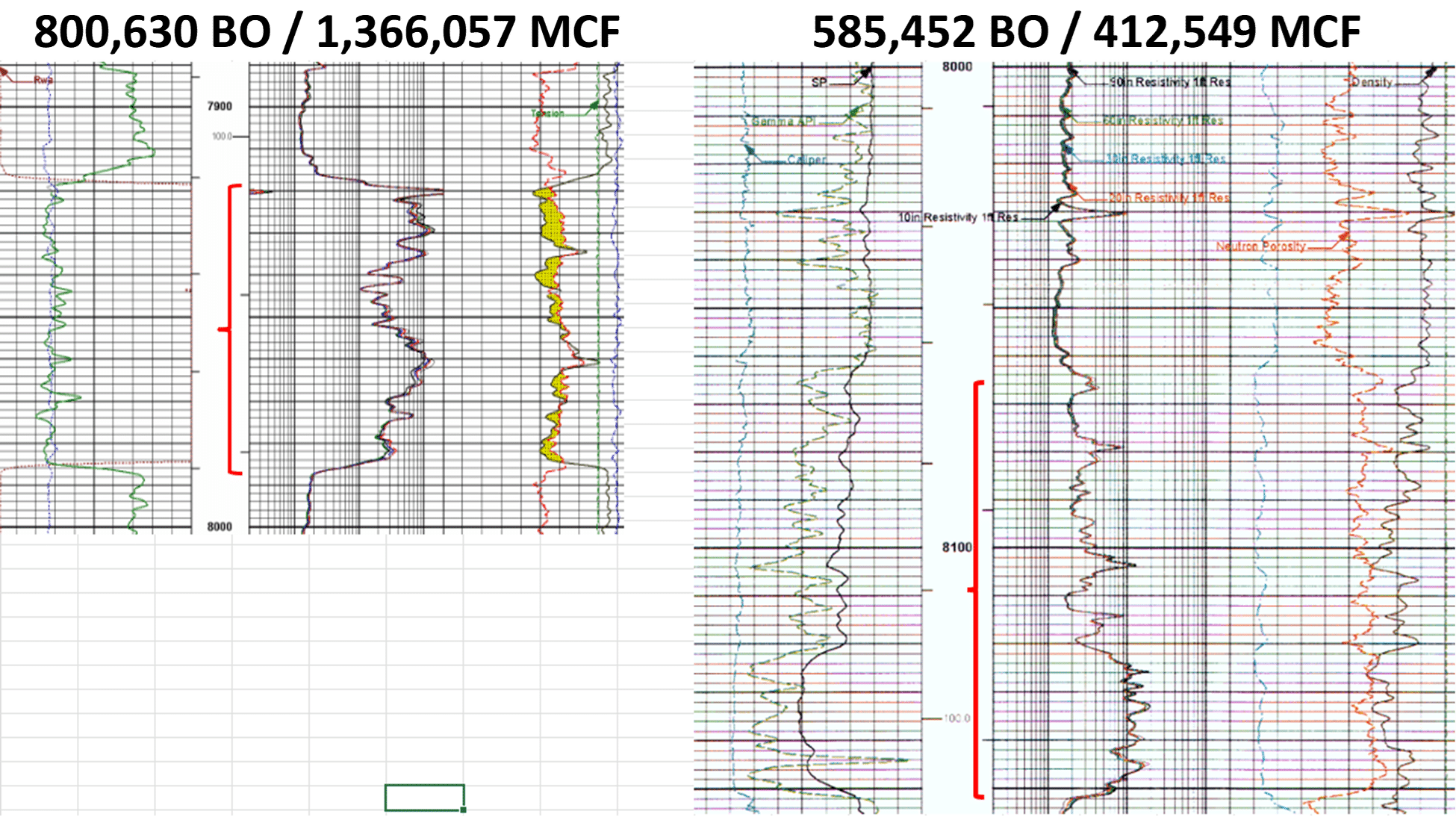

And with it, Pioneer found a nice, thick stray Wilcox sand (open hole log examples below) discovery that became the Sinor Nest Field, the yellow box on the previous map.

With well total depths around 8,000 feet and a mix of vertical and low offset directional wells, Sinor Nest has produced more than 7 million barrels of oil and 11 Bcf of gas from 28 wells. Using oil and gas prices from Feb. 4, 2022, and assuming a royalty of 25%, these produced assets would generate more than $485 million of net revenue before ongoing lease operating expenses. Not bad at all for 28 vertical wells drilled to about 8,000 feet.

Nearly half the Wilcox wells have produced more than 350,000 BOE.

I remember working in the Austin Chalk in the mid ‘80s when I was put on notice about uphole opportunities when AOP Operating plugged back Humble’s Isis well (Austin Chalk) and re-perforated the Wilcox from 5,502 to 5,534 feet. This uphole re-completion in the Wilcox produced nearly six Bcf of gas but only 39,414 bbl of oil.

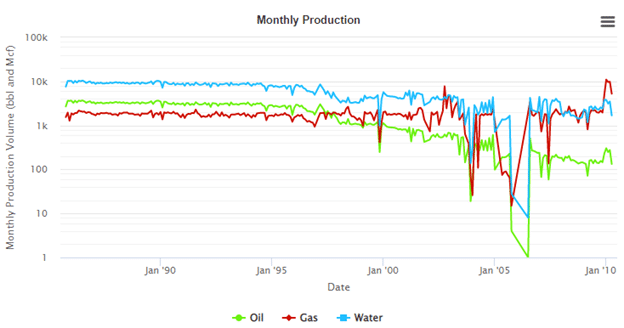

Four months later, HECI Exploration brought in the Russell Neel Unit well, which ultimately produced 507,621 bbl and 521,959 MCF of gas at depths of around 5,600 feet with stable and predictable decline rates, but with high water cuts.

The focus on unconventional production capabilities is understandable. Enormous amounts of money have been spent to exploit these resources, and production from them vaulted the U.S. into the top spot as the world’s most voluminous oil producer.

And the focus is, quite naturally, for major unconventional players to manage their reserves and their capex to hew to the valuation mandates around free cash flow that Wall Street and the banking community have prioritized.

But there is good potential for significant uphole, and maybe downhole, reserves to be discovered in almost all of these unconventional plays.

It’s impossible to know at this point whether a focus on uphole conventional targets could yield the same reserves as the bounty that unconventional wells have provided the industry and the country.

But if you compare Eagle Ford’s median BOE of 322,000 with Sinor Nest’s median BOE of 230,000, which was achieved at a fraction of the high cost of fractured horizontal wells, there can be a compelling value proposition around dedicating interpretation resources to identifying uphole conventional reservoirs.

We’re not hearing much about farmouts from these large operators, but it sure seems like a sensible way to capitalize on the enriched data set that all these horizontals have created.

A quick LandTrac search into Reeves County, Texas, for leases over the past 36 months (by instrument date) finds only about 14% of leases subject to depth or Pugh clauses, so farmouts of relatively large acreage positions that are still held by production by unconventionally drilled wells, should be a realistic option.

Private equity, are you listening?