[contextly_auto_sidebar]

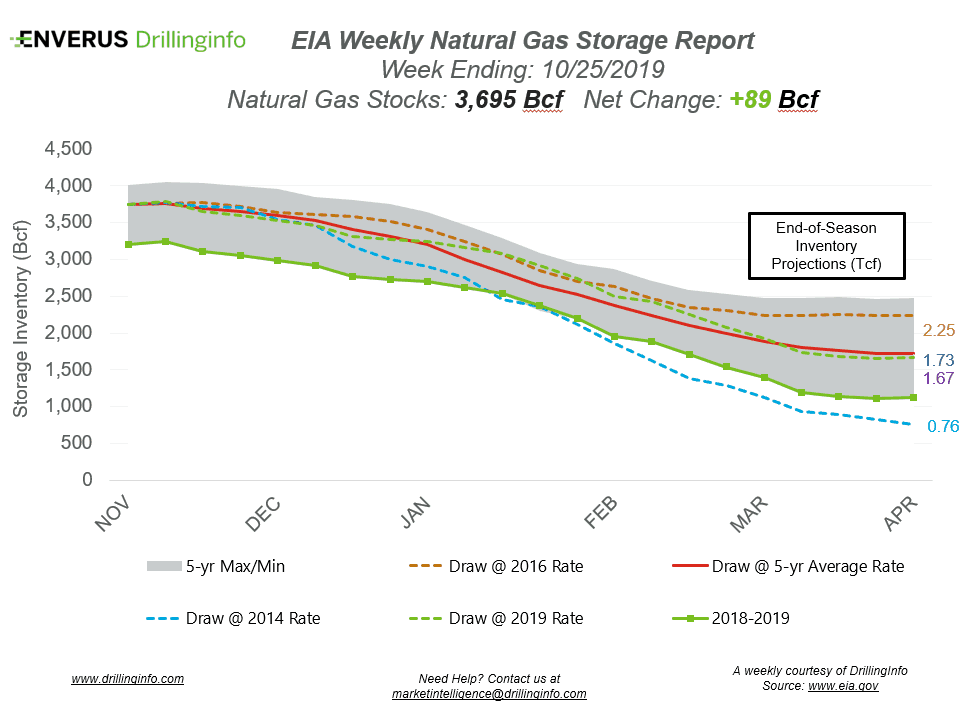

Natural gas storage inventories increased 89 Bcf for the week ending October 25, according to the EIA’s weekly report. This is slightly lower than the market expectation, which was an injection of 91 Bcf.

Working gas storage inventories now sit at 3.695 Tcf, which is 559 Bcf above inventories from the same time last year and 52 Bcf above the five-year average.

Prior to the storage report release, the December 2019 contract was trading at $2.675/MMBtu, roughly $0.016 lower than yesterday’s close. At the time of writing, after the report, the December 2019 contract was trading at $2.655/MMBtu. Earlier this week, the November 2019 contract expired at $2.597/MMBtu, rallying ~$0.30/MMBtu from October 25 to the close on October 29.

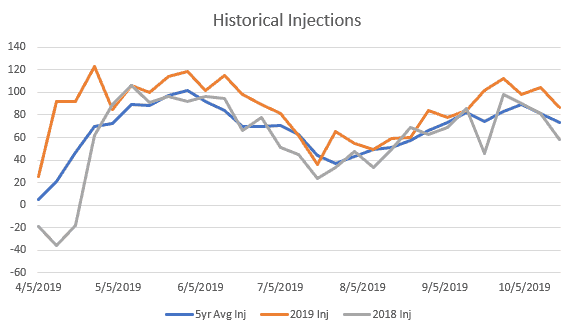

Injections over the summer have been strong compared to last year as well as to the five-year average. Injections during the 2019 summer season have been consistently above the five-year average injection, with the exception of a brief period in July. During summer 2019, injections have averaged 18 Bcf/week stronger than the five-year average and 25 Bcf/week stronger than injections during summer 2018. Lower-48 demand has strengthened over the past five years, with more natural gas power plants and LNG exports. However, that demand hasn’t been able to keep up with supply, allowing for strong injections throughout the summer and storage inventories to recover the deficit at the start of injection season.

See the chart below for projections of the end-of-season storage inventories as of April 1, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending October 31, 2019.

Supply:

- Dry production decreased 0.59 Bcf/d on the week. Most of the decrease came from the Mountain region (-0.28 Bcf/d), the South Central (-0.27 Bcf/d) and the East (-0.04 Bcf/d), with small gains in the Midwest and the Pacific.

- Canadian imports increased 0.21 Bcf/d.

Demand:

- Domestic natural gas demand increased 4.37 Bcf/d week over week. Res/Com demand accounted for most of the increase, rising 4.95 Bcf/d. Industrial demand also increased 0.73 Bcf/d, while Power demand decreased 1.31 Bcf/d.

- LNG exports increased 0.14 Bcf/d, while Mexican exports decreased 0.07 Bcf/d.

Total supply decreased 0.38 Bcf/d, while total demand increased 4.53 Bcf/d week over week. With increased demand and a decrease in supply, expect the EIA to report a weaker injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 51 Bcf. Last year, the same week saw an injection of 65 Bcf; the five-year average is an injection of 46 Bcf.