[contextly_auto_sidebar]

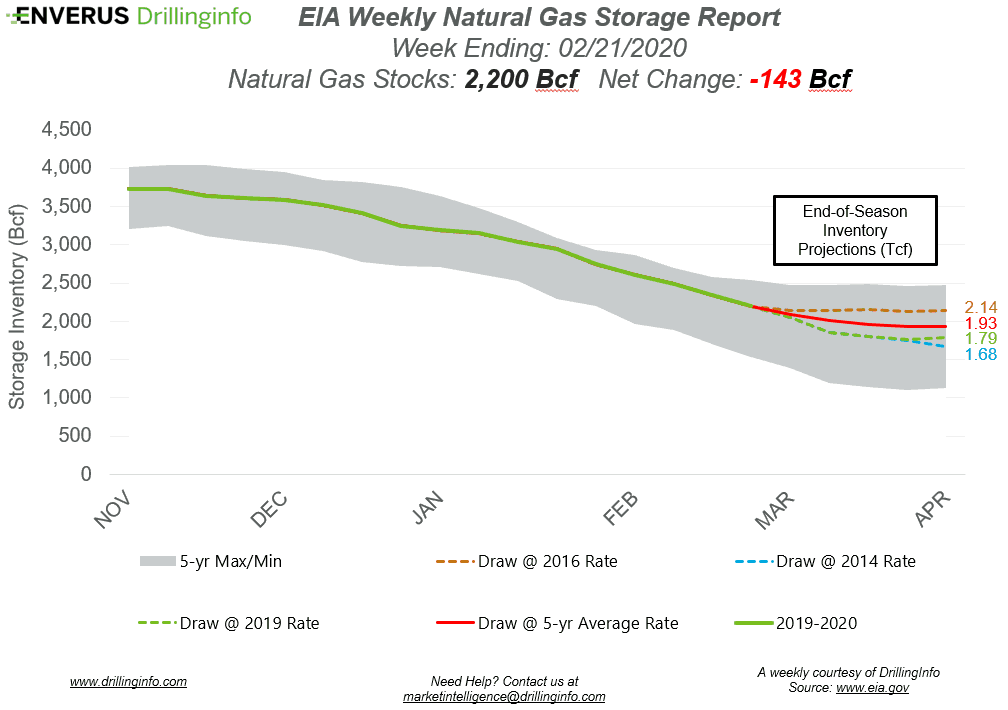

Natural gas storage inventories decreased 143 Bcf for the week ending February 21, according to the EIA’s weekly report. This was less than the expected draw of 152 Bcf.

Working gas storage inventories now sit at 2.200 Tcf, which is 637 Bcf above inventories from the same time last year and 179 Bcf above the five-year average.

The March 2020 contract expired yesterday and settled at $1.821/MMBtu. Prior to the storage report release, the April 2020 contract was trading at $1.746/MMBtu, roughly $0.091 below yesterday’s close. After the release of the report and at the time of writing, the April 2020 contract was trading at $1.735/MMBtu.

Last week, the storage report was a bullish draw and the 6-to-14-day weather forecast showed below-average temperatures in high-demand areas. This prompted prices to exceed the $2.00/MMBtu mark for the first time since January 17. However, the price run was short-lived. As the day continued, prices fell back below the $2.00/MMBtu mark and ultimately closed at $1.92/MMBtu. Over the weekend, weather forecasts turned warmer, causing prices to decline further, closing Monday at $1.827. Prices have remained near the $1.80 area throughout the week, but broke below that area this morning. With weather forecasts showing normal to above-normal temperatures in areas with high demands for heat, market sentiment is overwhelmingly bearish. Expect further price declines and possibly a test of the 2016 lows of $1.63.

See the chart below for projections of the end-of-season storage inventories as of April 1, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus analysis for the week ending February 27.

Supply:

- Dry production increased 0.12 Bcf/d on the week. Most of the increase came from the East (+0.18 Bcf/d), with an offset coming from the Mountain region (-0.04 Bcf/d) and the South Central (-0.02 Bcf/d).

- Canadian net imports decreased 0.59 Bcf/d, mainly due to decreased imports into the Northeast.

Demand:

- Domestic natural gas demand decreased 7.44 Bcf/d week over week. Res/Com demand accounted for the majority of the decrease, falling 5.98 Bcf/d on the week. Power demand and Industrial also decreased, falling 1.07 Bcf/d and 0.39 Bcf/d, respectively.

- LNG exports increased 0.61 Bcf/d, mainly due to maintenance coming to a close at Cameron and Sabine Pass. Mexican exports increased 0.11 Bcf/d.

Total supply decreased 0.46 Bcf/d, while total demand decreased 6.94 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a weaker draw next week. The ICE Financial Weekly Index report is currently expecting a draw of 123 Bcf. Last year, the same week saw a draw of 149 Bcf; the five-year average is a draw of 106 Bcf.