[contextly_auto_sidebar]

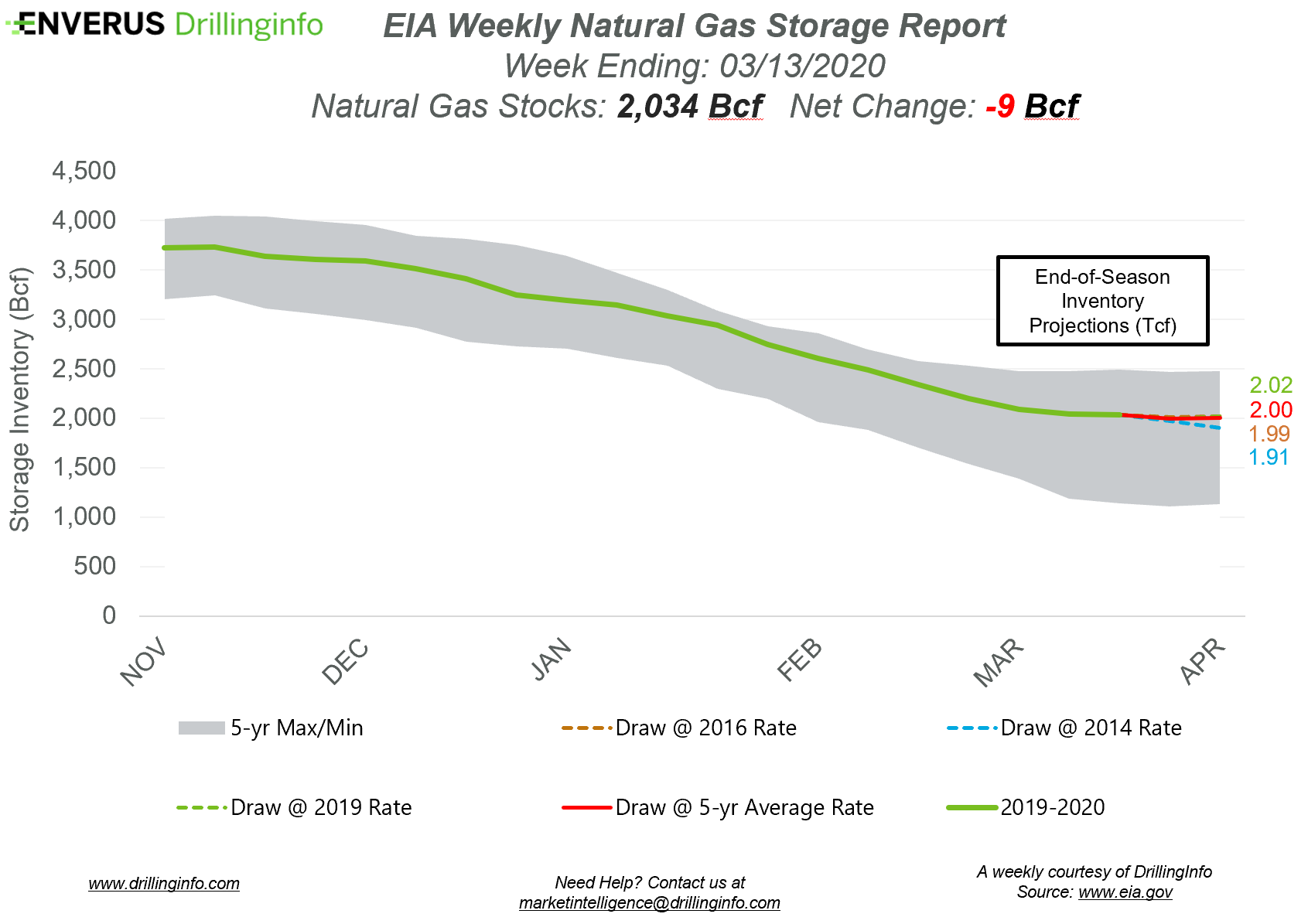

Natural gas storage inventories decreased 9 Bcf for the week ending March 13, according to the EIA’s weekly report. This was larger than the expected draw of 4 Bcf.

Working gas storage inventories now sit at 2.034 Tcf, which is 878 Bcf above inventories from the same time last year and 281 Bcf above the five-year average.

Prior to the storage report’s release, the April 2020 contract was trading at $1.618/MMBtu, roughly $0.014 above yesterday’s close. After the release of the report and at the time of writing, the April 2020 contract was trading at $1.640/MMBtu.

The bullish sentiment in the natural gas market as a result of the OPEC+ production cuts falling apart hasn’t taken hold in the market. Natural gas prices have traded between $1.60 and $2.00 since the announcement. However, with numerous companies announcing less ambitious drilling plans in 2020 because of poor oil economics, associated gas production is expected to decline throughout the year. Some of the associated gas that would normally fall off at these price levels will still hit the market, as operators have hedges in place and will continue to produce. As operator hedges roll off and if production economics are still poor, operators will stop completing oil-directed wells and associated natural gas production will decline. This will likely lead to higher natural gas prices to incentivize completing wells in gas-directed areas, as demand still needs to be met.

See the chart below for projections of the end-of-season storage inventories as of April 1, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus’ analysis for the week ending March 19.

Supply:

- Dry production increased 0.89 Bcf/d on the week. Most of the increase came from the South Central (+0.55 Bcf/d), East (+0.21 Bcf/d), and Mountain (+0.12 Bcf/d) regions. The Midwest also saw a small increase (+0.02 Bcf/d), while the Pacific saw a small decrease (-0.01 Bcf/d).

- Canadian net imports increased 0.33 Bcf/d.

Demand:

- Domestic natural gas demand increased 3.63 Bcf/d week over week. Power demand and Res/Com demand accounted for the majority of the increase, rising 2.42 Bcf/d and 1.42 Bcf/d on the week. Industrial demand decreased, falling 0.21 Bcf/d, respectively.

- LNG exports decreased 0.27 Bcf/d, while Mexican exports increased 0.03 Bcf/d.

Total supply increased 1.23 Bcf/d, while total demand increased 3.54 Bcf/d week over week. With the increase in demand outpacing the increase in supply, expect the EIA to report a larger draw next week. The ICE Financial Weekly Index report is currently expecting a draw of 21 Bcf. Last year, the same week saw a draw of 36 Bcf; the five-year average is a draw of 37 Bcf.