[contextly_auto_sidebar]

Injection Tops Market Expectations, Gulf Coast Express Starts Service

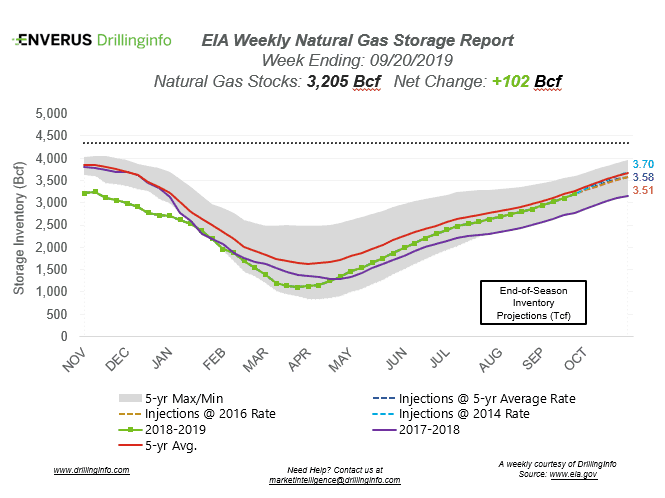

Natural gas storage inventories increased 102 Bcf for the week ending September 20, according to the EIA’s weekly report. This is higher than the market expectation, which was an injection of 92 Bcf.

Working gas storage inventories now sit at 3.205 Tcf, which is 444 Bcf above inventories from the same time last year and 47 Bcf below the five-year average.

Prior to the storage report release, the October 2019 contract was trading at $2.475/MMBtu, roughly $0.027 lower than yesterday’s close. At the time of writing, post report, the October 2019 contract was trading at $2.399/MMBtu.

Natural Gas News

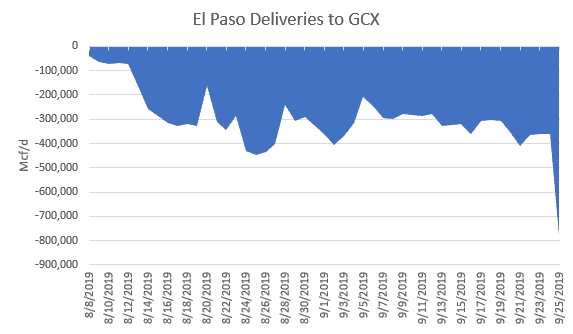

Kinder Morgan announced yesterday the start-up of the Gulf Coast Express pipeline. The pipeline runs from the Permian to the Gulf Coast, delivering gas near Corpus Christi. The pipeline is the first gas pipeline to hit the market to help relieve the gas pipeline bottleneck in the Permian. On day one of service on September 25, deliveries from El Paso to Gulf Coast Express ramped up to 0.78 Bcf, more than double the prior day’s delivery of 0.36 Bcf/d. The gas coming from Gulf Coast Express hits interconnects and will be used to serve the growing demand markets along the Gulf Coast.

Cove Point LNG started maintenance earlier this week, taking volumes to the plant to zero. During the maintenance around the same time in 2018, the plant was down for roughly three weeks. A similar maintenance time frame for the Cove Point facility is expected.

See the chart below for the projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending September 26, 2019.

Supply:

- Dry production increased 0.44 Bcf/d on the week. Most of the increase came from the South Central (+0.12 Bcf/d), the Mountain region (+0.18 Bcf/d), and the East (+0.13 Bcf/d).

- Canadian imports decreased 0.13 Bcf/d on the week.

Demand:

- Domestic natural gas demand dropped 1.65 Bcf/d week over week. Power demand accounted for most of the decrease, falling 1.76 Bcf/d. Res/Com demand increased 0.15 Bcf/d, while Industrial demand decreased 0.04 Bcf/d.

- LNG exports decreased 0.74 Bcf/d, mainly due to Cove Point starting their annual maintenance. Mexican exports increased 0.20 Bcf/d.

Total supply increased 0.30 Bcf/d while total demand decreased 2.21 Bcf/d week over week. With the increase in supply and the decrease in demand, expect the EIA to report a stronger injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 104 Bcf. Last year, the same week saw an injection of 46 Bcf; the five-year average is an injection of 69 Bcf.