[contextly_auto_sidebar]

Natural gas storage inventories increased 34 Bcf for the week ending November 1, according to the EIA’s weekly report. This is lower than the market expectation, which was an injection of 43 Bcf.

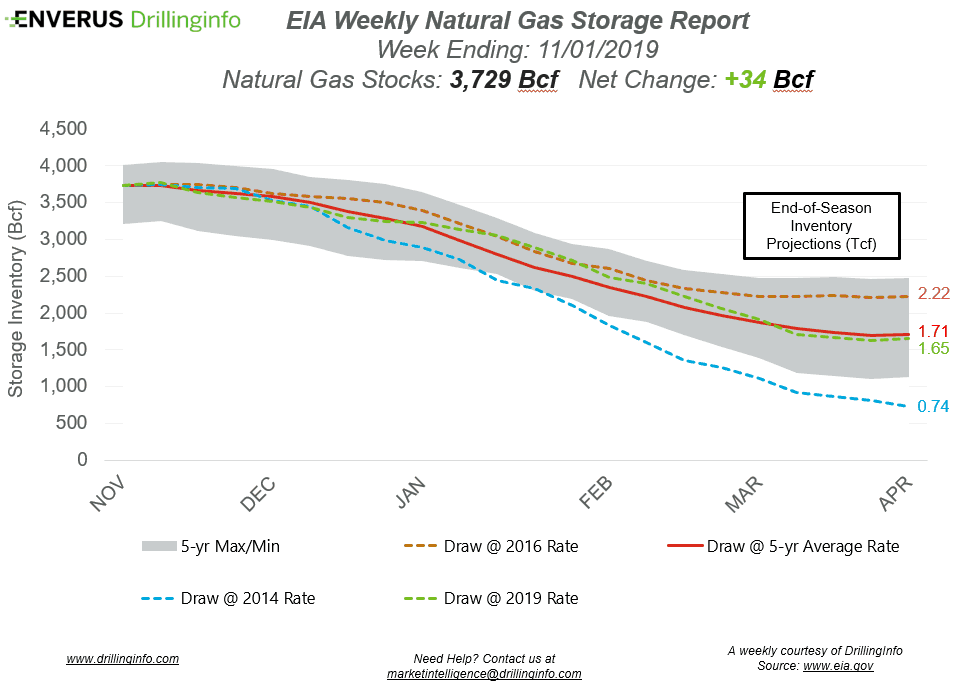

Working gas storage inventories now sit at 3.729 Tcf, which is 530 Bcf above inventories from the same time last year and 29 Bcf above the five-year average.

Prior to the storage report release, the December 2019 contract was trading at $2.811/MMBtu, roughly $0.017 lower than yesterday’s close. At the time of writing, after the report, the December 2019 contract was trading at $2.860/MMBtu.

The start of the winter season is officially here, and volatility already is making an appearance. During the last few trading days of October, the December 2019 contract gained ~$0.17/MMBtu from October 25 to October 31 to reach $2.633. The gains have not slowed down during November, as the December 2019 contract closed on November 5 at $2.862, the highest close for the contract since September 16. This rally can be attributed mostly to the weather forecasts adjusting to show cooler temperatures in the northern Midwest. However, weather forecast changes likely do not explain the entire rally. Initial stages of short covering were seen on the CFTC report, dated October 29, as the Managed Money short positions decreased 21,951 contracts, while the long positions increased 12,085 contracts. This short covering was brought on by the price rally with the weather forecast changes. As prices increased, traders sold off their short positions, adding fuel to the price rally.

See the chart below for projections of the end-of-season storage inventories as of April 1, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending November 7, 2019.

Supply:

- Dry production increased 0.07 Bcf/d on the week. Most of the increase came from the South Central (+0.36 Bcf/d) and the East (+0.20 Bcf/d), with an offset coming from the Mountain region (-0.53 Bcf/d). The Midwest and Pacific saw small gains.

- Canadian imports decreased 0.06 Bcf/d.

Demand:

- Domestic natural gas demand increased 5.69 Bcf/d week over week. Res/Com demand accounted for most of the increase, rising 6.39 Bcf/d. Industrial demand also increased 0.69 Bcf/d, while Power demand decreased 1.39 Bcf/d.

- LNG decreased 0.21 Bcf/d, while Mexican exports decreased 0.02 Bcf/d.

Total supply increased 0.01 Bcf/d, while total demand increased 5.64 Bcf/d week over week. With increased demand and relatively flat supply, expect the EIA to report a weaker injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 4 Bcf. Last year, the same week saw an injection of 39 Bcf; the five-year average is an injection of 10 Bcf.