[contextly_auto_sidebar]

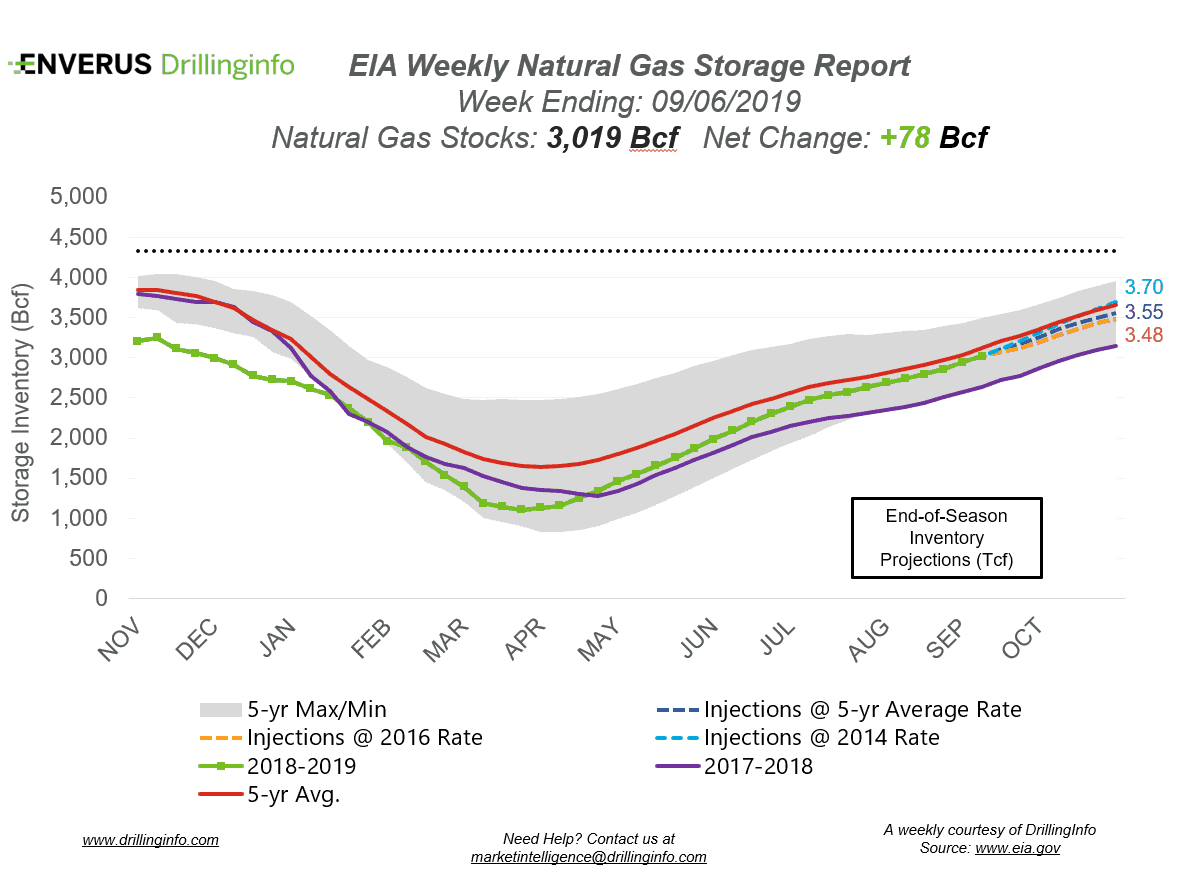

Natural gas storage inventories increased 78 Bcf for the week ending September 6, according to the EIA’s weekly report. This is lower than the market expectation, which was an injection of 82 Bcf.

Working gas storage inventories now sit at 3.019 Tcf, which is 393 Bcf above inventories from the same time last year and 77 Bcf below the five-year average.

Prior to the storage report release, the October 2019 contract was trading at $2.525/MMBtu, roughly $0.027 lower than yesterday’s close. Prices rose post report to $2.559/MMBtu, but could not hold. At the time of writing, the October 2019 contract was trading at $2.549/MMBtu.

At the start of the injection season, the market was at a storage deficit compared to both last year and the five-year average. At the start of injection season for summer 2019, storage inventories sat at 1,107 Bcf. This inventory level was 276 Bcf below 2018 and 544 Bcf below the five-year average. However, increased production year over year has been able to help get the market out of the deficit. Last year, lower-48 dry gas production averaged 82.98 Bcf/d from April to August, while this year production has averaged 89.59 Bcf/d for the same time frame. This production increase, coupled with mild weather at the beginning of the summer season, allowed for larger injections during summer 2019. By the end of August, inventories were well past last year’s levels, and they are gaining on the five-year average. The largest regional deficit that remains is in the South Central/Gulf region, which was 51 Bcf behind the five-year average at the end of August.

Looking forward, September is expected to remain above-average in terms of temperature, causing above-average CDDs and power burn. In the 10- to 15-day range, temperatures are expected to show more seasonal cooling. October is also currently expected to have above-average temperatures. However, above-average temperatures in October can have a bearish impact as HDDs are lower, causing lower heating demand and more supply in the market.

See the chart below for the projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending September 12, 2019.

Supply:

- Dry production decreased 0.47 Bcf/d on the week. Most of the decrease came from the Mountain region (-0.41 Bcf/d), where North Dakota production dropped 0.14 Bcf/d and Colorado production fell 0.17 Bcf/d.

- Canadian imports increased 0.12 Bcf/d on the week.

Demand:

- Domestic natural gas demand dropped 0.76 Bcf/d week over week. Power demand accounted for most of the decrease, falling 0.62 Bcf/d. Res/Com demand decreased 0.06 Bcf/d, while Industrial demand decreased 0.08 Bcf/d.

- LNG exports fell 0.22 Bcf/d, while Mexican exports decreased 0.06 Bcf/d.

Total supply decreased 0.35 Bcf/d while total demand decreased 0.65 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a stronger injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 87 Bcf. Last year, the same week saw an injection of 86 Bcf; the five-year average is an injection of 86 Bcf.