[contextly_auto_sidebar]

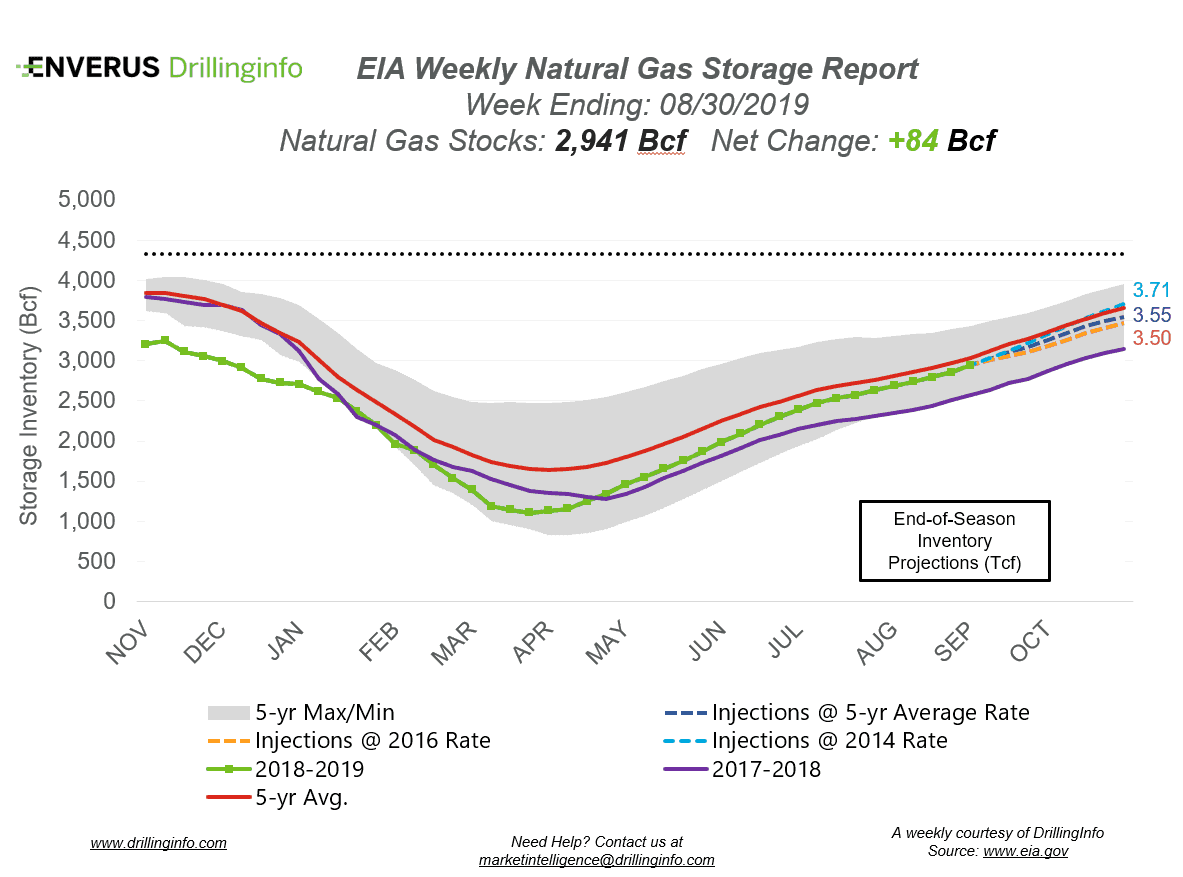

Natural gas storage inventories increased 84 Bcf for the week ending August 30, according to the EIA’s weekly report. This is higher than the market expectation, which was an injection of 76 Bcf.

Working gas storage inventories now sit at 2.941 Tcf, which is 383 Bcf above inventories from the same time last year and 82 Bcf below the five-year average.

Prior to the storage report release, the October 2019 contract was trading at $2.426/MMBtu, roughly $0.019 lower than yesterday’s close. However, prices continued to fall post report, and at the time of writing were trading at $2.400/MMBtu.

Since last Thursday, prices have gained ~$0.10/MMBtu. The main driver of the price increase is the weather forecast. September temperatures are expected to be above average in the South/South Central, driving higher than normal power burn demand. Additionally, Hurricane Dorian shifted course as the storm headed toward the lower 48. Dorian, which made landfall in the Bahamas last weekend, then turned north to move up the East Coast. This change in path caused less rain and cooling in the southeastern portion of the US, and didn’t impact power demand as drastically as if the storm had trended inland. In the coming days, Dorian is expected to bring wind and rain to the Carolinas before traveling back into the Atlantic.

See the chart below for the projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus analysis for the week ending September 5, 2019.

Supply:

- Dry production didn’t see much movement week over week, decreasing 0.03 Bcf/d on the week.

- Canadian imports increased 0.39 Bcf/d on the week.

Demand:

- Domestic natural gas demand gained 1.22 Bcf/d week over week. Power demand accounted for nearly the entire change in demand week over week, increasing 1.22 Bcf/d. Res/Com demand decreased 0.01 Bcf/d, while Industrial demand gained 0.02 Bcf/d.

- LNG exports fell 0.44 Bcf/d, mainly due to decreased exports at Sabine Pass. Mexican exports remained relatively flat on the week, gaining only 0.05 Bcf/d.

Total supply increased 0.36 Bcf/d, while total demand increased 0.88 Bcf/d week over week. With demand outpacing supply, expect the EIA to report a slightly weaker injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 82 Bcf. Last year, the same week saw an injection of 69 Bcf; the five-year average is an injection of 78 Bcf.