[contextly_auto_sidebar]

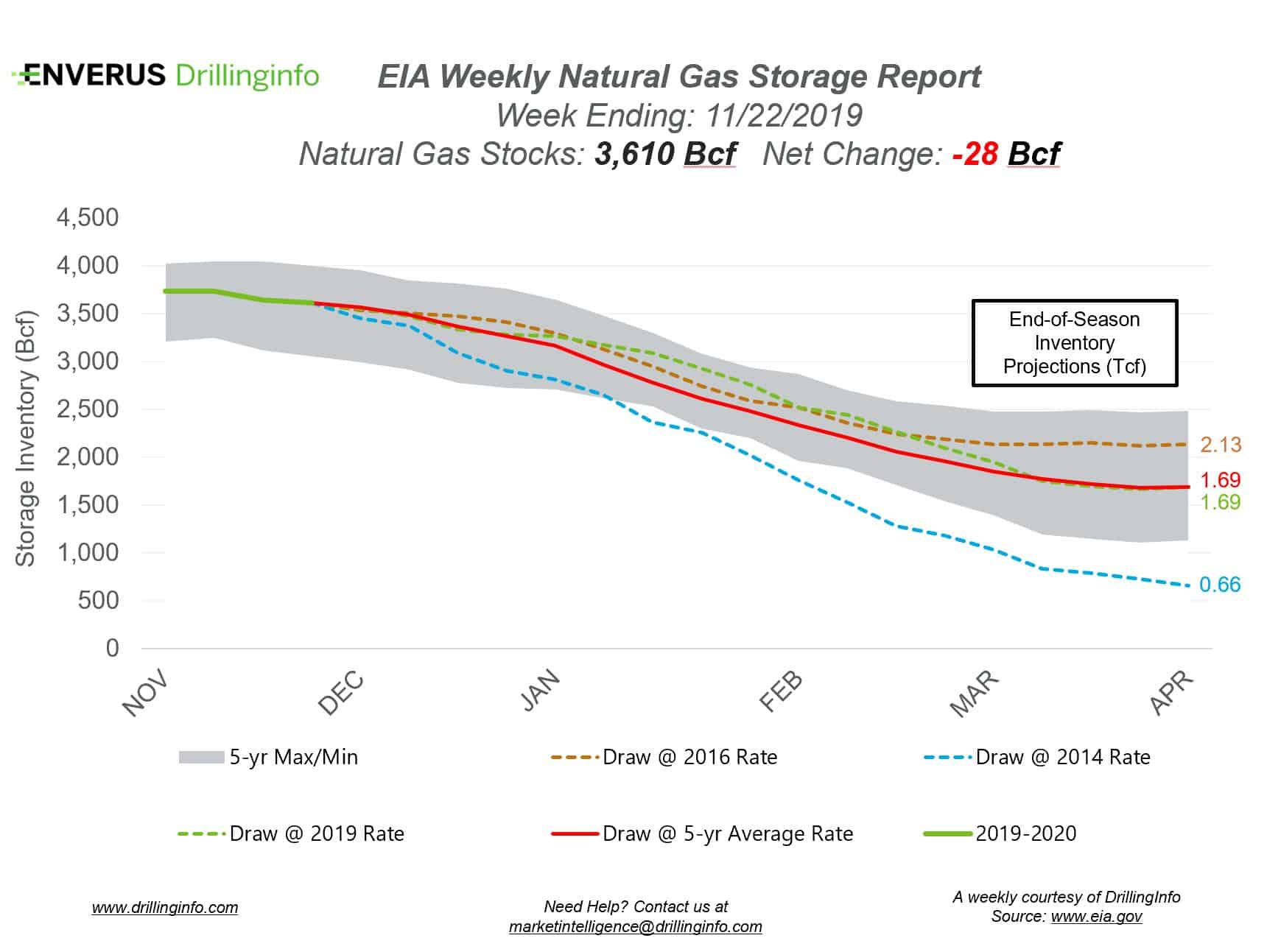

Natural gas storage inventories decreased 28 Bcf for the week ending November 22, according to the EIA’s weekly report. This was higher than the market expectation, which was a draw of 27 Bcf.

Working gas storage inventories now sit at 3.610 Tcf, which is 548 Bcf above inventories from the same time last year and 31 Bcf below the five-year average.

Prior to the storage report release, the January 2020 contract was trading at $2.507/MMBtu, roughly $0.026 lower than yesterday’s close. At the time of writing, after the release of the report, the January 2020 contract was trading at $2.518/MMBtu. The December contract expired yesterday at $2.470.

Volatility has been the theme of the market to start the winter season. Since the beginning of November, the December 2019 contract has traded in a ~$0.40 range, between $2.45 and $2.84, and the contract closed near the bottom of the range. The wide range has been, and will continue to be, driven by changes in weather forecasts. Current weather forecasts show below-average temperatures through the weekend and early next week. By mid-next week, temperatures will moderate, with above-average temperatures expected.

See the chart below for projections of the end-of-season storage inventories as of April 1, 2020, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending November 27, 2019.

Supply:

- Dry production increased 0.88 Bcf/d on the week. Most of the increase came from the South Central (+0.67 Bcf/d) where Texas (+0.48 Bcf/d) and Oklahoma (+0.15 Bcf/d) accounted for most of the increase.

- Canadian net imports decreased 1.21 Bcf/d mainly due to decreased imports to the Midwest and the Northeast.

Demand:

- Domestic natural gas demand decreased 3.78 Bcf/d week over week. Res/Com demand fell 3.09 Bcf/d, while Power and Industrial demand decreased 0.26 Bcf/d and 0.44 Bcf/d, respectively.

- LNG exports fell 0.10 Bcf/d, while Mexican exports decreased 0.21 Bcf/d on the week.

Total supply decreased 0.33 Bcf/d, while total demand decreased 4.17 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a weaker draw next week. The ICE Financial Weekly Index report is currently expecting a draw of 23 Bcf. Last year, the same week saw a draw of 63 Bcf; the five-year average is a draw of 46 Bcf.