[contextly_auto_sidebar]

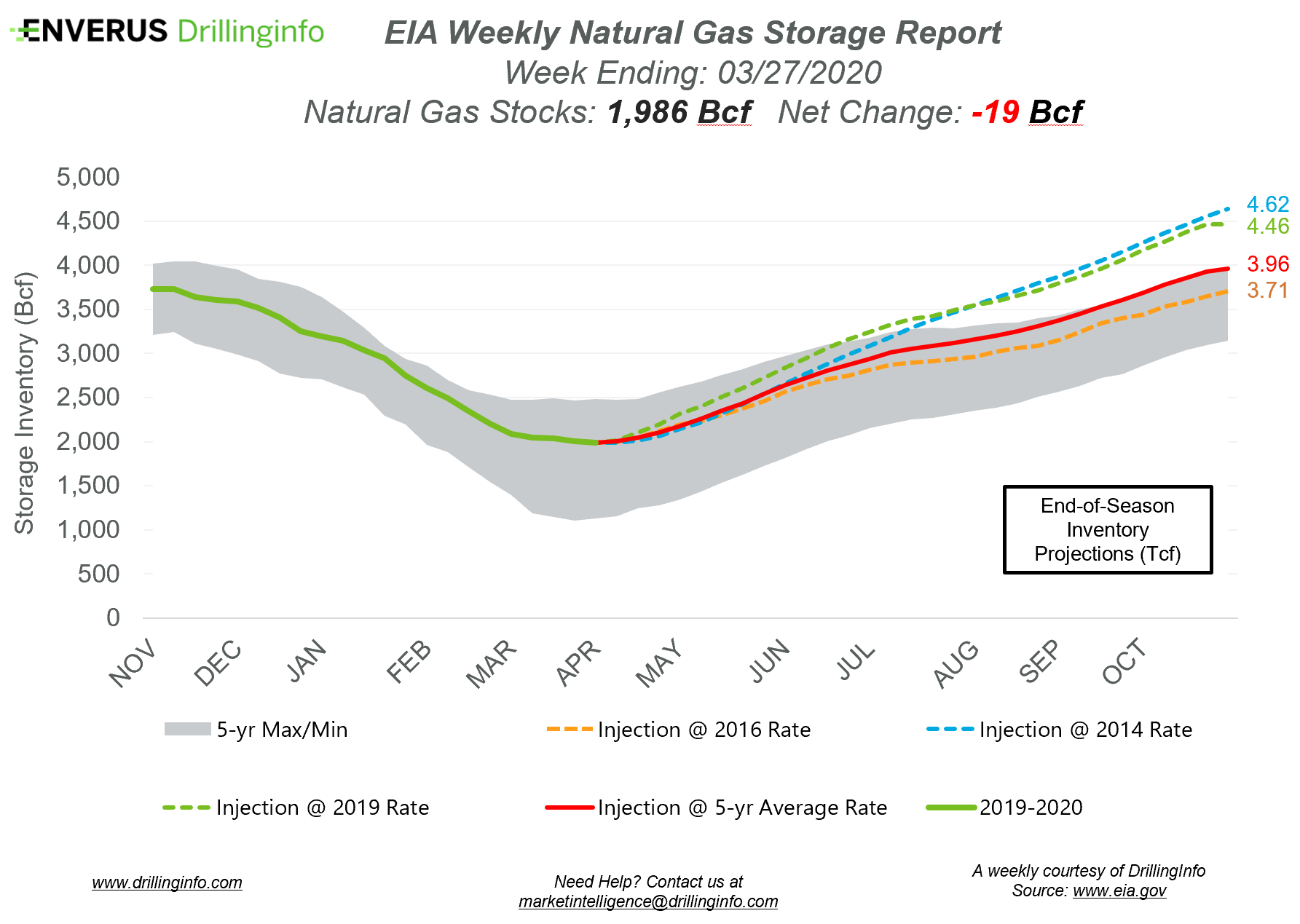

Natural gas storage inventories decreased 19 Bcf for the week ending March 27, according to the EIA’s weekly report. This was larger than the expected draw of 15 Bcf.

Working gas storage inventories now sit at 1.986 Tcf, which is 863 Bcf above inventories from the same time last year and 292 Bcf above the five-year average.

The April 2020 contract expired Friday at $1.634/MMBtu, establishing a record low settlement for April within the past two decades. Prior to the storage report’s release, the May 2020 contract was trading at $1.558/MMBtu, roughly $0.029 below yesterday’s close. After the release of the report and at the time of writing, the May 2020 contract was trading at $1.542/MMBtu.

Rigs continue to fall off the map as operators are slowing their drilling plans because of the lack of demand due to COVID-19 and the vast oversupply in the market. Since March 1, the US has fallen from 821 rigs to 676 rigs, based on Enverus’s Daily Rig Count. On a percentage basis, the most rigs have fallen from the Anadarko which dropped 13 rigs, or 27.1%, from March 1 to April 1. The Permian has been the main driver of the 145-rig drop, falling 58 rigs (-14.9%) over the past month. The drop in the Permian started in mid-March after OPEC+ couldn’t reach an agreement on production cuts, forcing US shale players to restructure their capital spending for the year and ultimately lower CapEx and production guidance.

As liquids storage fills up—which might very well happen in the near future—shut-ins are likely to take place. These shut-ins will be heavily reliant on the variable operational expenses (OpEx), which vary among individual wells. The more expensive wells to operate have a higher likelihood of being shut in during the current low-price environment. Looking at OpEx by basin can provide an understanding of where associated gas is likely to fall off first due to shut-ins.

Natural gas storage inventories are currently expected to end the injection season well above-average levels. However, should operators start shutting in production, this will take away additional associated gas supply, and the end of injection season inventories will be revised down from current expectations.

In Enverus’s latest FundamentalEdge Series, “The Dark Side of the Boom,” variable OpEx was analyzed by basin to understand what these costs look like across major basins in the US. To get a preview of the latest FundamentalEdge report, reach out to sag@enverus.com.

See the chart below for projections of the end-of-season storage inventories as of November 1, 2020, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus’ analysis for the week ending April 2.

Supply:

- Dry natural gas production increased 0.11 Bcf/d on the week. Most of the increase came from the Mountain region, which gained 0.13 Bcf/d.

- Canadian net imports decreased 0.65 Bcf/d, largely due to decreased imports into the Pacific Northwest and the North Midcontinent.

Demand:

- Domestic natural gas demand decreased 8.23 Bcf/d week over week. Res/Com demand accounted for the majority of the decrease, falling 5.22 Bcf/d on the week. Power and Industrial demand also decreased, falling 2.48 Bcf/d and 0.53 Bcf/d, respectively.

- LNG exports increased 0.09 Bcf/d, while Mexican exports decreased 0.04 Bcf/d.

Total supply decreased 0.65 Bcf/d, while total demand decreased 8.75 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report the first injection of the season. The ICE Financial Weekly Index report is currently expecting an injection of 27 Bcf. Last year, the same week saw an injection of 23 Bcf; the five-year average is an injection of 5 Bcf.