[contextly_auto_sidebar]

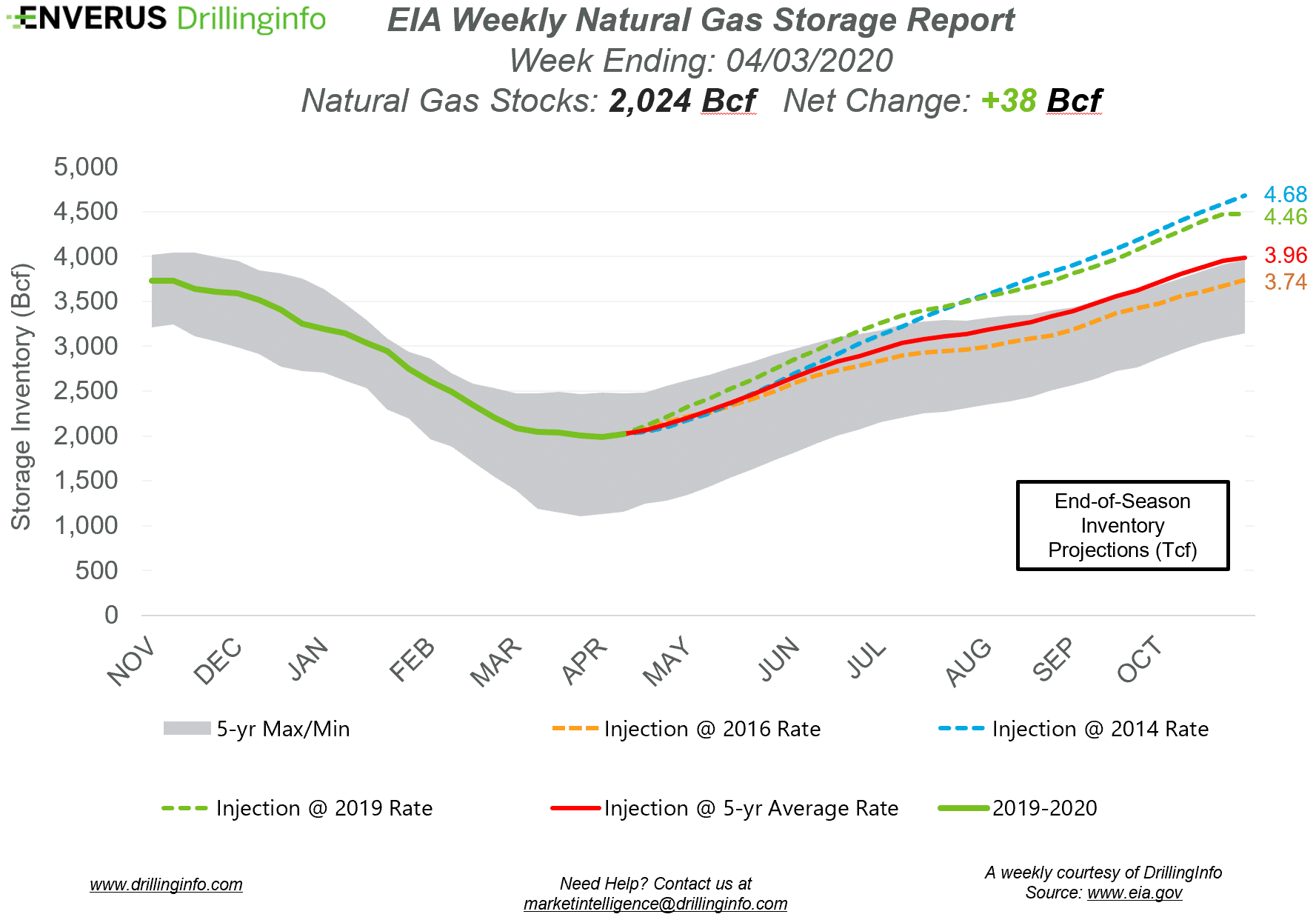

Natural gas storage inventories increased 38 Bcf for the week ending April 3, according to the EIA’s weekly report. This was larger than the expected injection of 28 Bcf.

Working gas storage inventories now sit at 2.204 Tcf, which is 876 Bcf above inventories from the same time last year and 324 Bcf above the five-year average.

Prior to the storage report’s release, the May 2020 contract was trading at $1.784/MMBtu, roughly $0.001 above yesterday’s close. After the release of the report and at the time of writing, the May 2020 contract was trading at $1.776/MMBtu.

The withdrawal season ended with last week’s EIA report for week ending March 27, and inventories sat at 1.986 Tcf, well above inventory levels from the year prior. Currently the market is in shoulder season, and demand is already at a low point for the year. COVID-19 has also caused some demand loss in the market during this already-low demand period. Coupling both of these together, and with the demand rebound from COVID-19 not expected to happen until the back half of the year, storage will likely get a significant prop up in the next couple of months. These early season injections, plus withdrawal season having ending inventories above average, are expected to leave storage inventories above average at the end of injection season.

However, associated gas production is expected to decline throughout the summer as the global crude market is in a severe oversupply state. Even though we will end injection season with above-average gas inventory levels, prices will need an uptick in the back half of the year as above-average storage levels aren’t expected to be enough to fulfill the winter demand with the decline in associated gas. With demand expected to recover from COVID-19 and the winter season causing an increase in heating demand, production will need to grow in dry gas areas to offset the expected loss in associated gas.

See the chart below for projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus’ analysis for the week ending April 9.

Supply:

- Dry natural gas production decreased 0.64 Bcf/d on the week. Most of the decrease came from the Mountain region (-0.37 Bcf/d) and the South Central (-0.35 Bcf/d), with an offset from the East (+0.07 Bcf/d).

- Canadian net imports decreased 0.10 Bcf/d.

Demand:

- Domestic natural gas demand decreased 3.59 Bcf/d week over week. Res/Com demand accounted for the majority of the decrease, falling 3.76 Bcf/d on the week. Industrial demand also decreased, falling 0.35 Bcf/d, while Power demand increased, rising 0.51 Bcf/d, respectively.

- LNG exports fell 1.23 Bcf/d, mainly due to decreases at Sabine Pass. Mexican exports decreased 0.59 Bcf/d.

Total supply decreased 0.73 Bcf/d, while total demand decreased 5.56 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a stronger injection next week. The ICE Financial Weekly Index report is currently expecting an injection of 49 Bcf. Last year, the same week saw an injection of 25 Bcf; the five-year average is an injection of 15 Bcf.