[contextly_auto_sidebar]

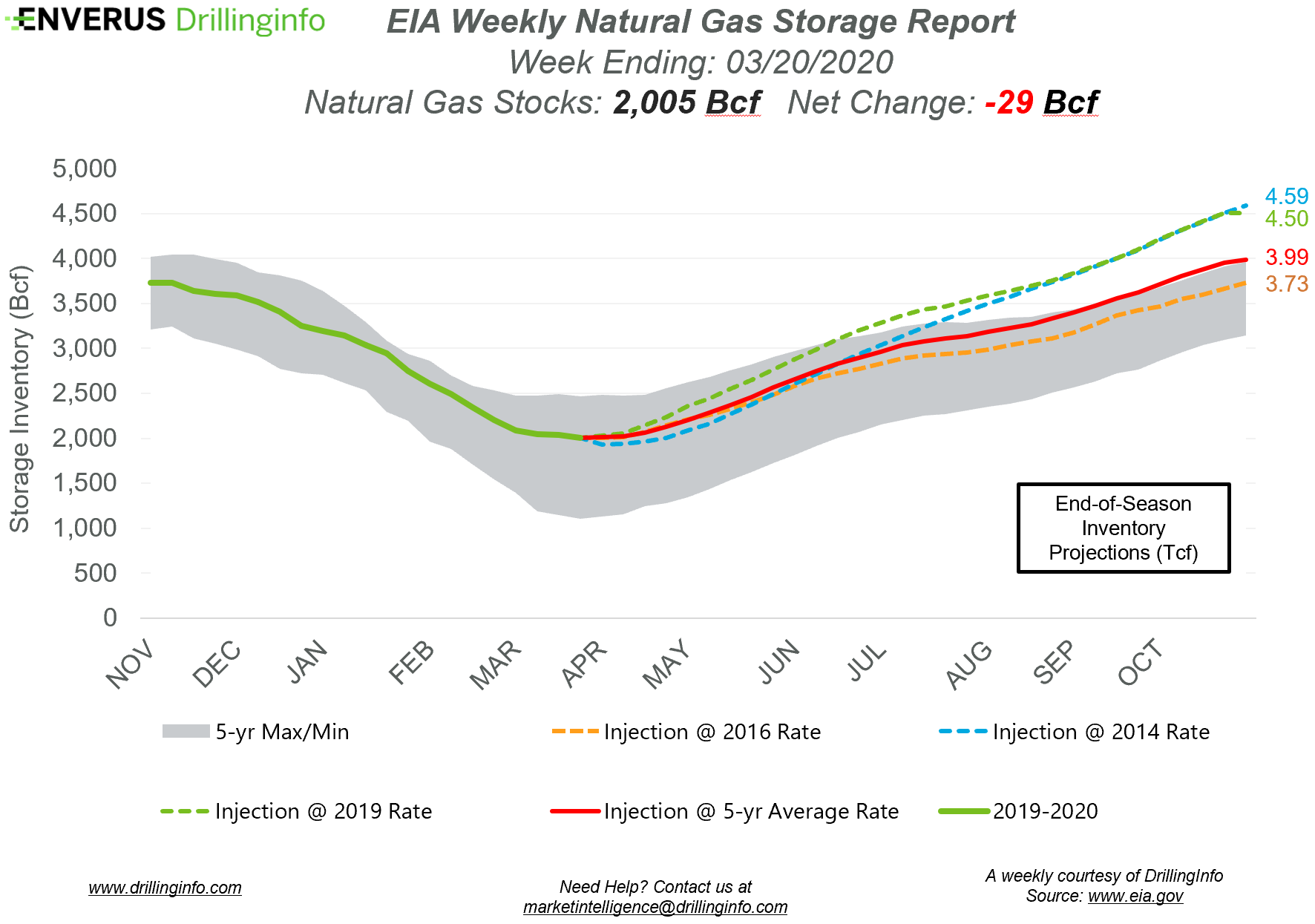

Natural gas storage inventories decreased 29 Bcf for the week ending March 20, according to the EIA’s weekly report. This was larger than the expected draw of 26 Bcf.

Working gas storage inventories now sit at 2.005 Tcf, which is 888 Bcf above inventories from the same time last year and 292 Bcf above the five-year average.

Prior to the storage report’s release, the April 2020 contract was trading at $1.642/MMBtu, roughly $0.017 below yesterday’s close. After the release of the report and at the time of writing, the April 2020 contract was trading at $1.641/MMBtu.

The natural gas market is in an interesting and unpredictable time right now. On one hand, the OPEC+ cuts falling apart and crude prices taking a tumble have operators reducing CAPEX and cutting their drilling plans for 2020, which will lead to less associated natural gas. However, on the other hand, we have the COVID-19 pandemic, which has tens of millions of Americans under stay-at-home orders. These orders keeping people at home mean that a number of businesses and industrial facilities are closed. Ultimately, people staying at home will lead to less natural gas demand in the commercial and industrial sectors. As we are in shoulder season, demand is already low, as it’s too warm for residential heating but too cold for power burn demand.

The impact on demand from COVID-19 has yet to really be seen in the US, but on the supply side, we’ve already seen a number of rigs drop off. From March 17 to March 25, the rig count in the lower 48 fell from 802 rigs to 739, indicating that operators’ less ambitious plans are already making headway. Continue to monitor the rig count here using Enverus’s daily rig count to understand what drilling trends look like. On the demand side, as well as the supply side, monitor natural gas flow data trends to understand what kind of demand drops are happening in the market because of COVID-19 and where supply is falling as operators slow their drilling plans. If you or your company doesn’t currently utilize natural gas flow data but think it could be beneficial, reach out to Enverus at sag@enverus.com to get a demo of OptiFlo Gas to see how flow data can help you understand supply and demand dynamics.

See the chart below for projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus’ analysis for the week ending March 26.

Supply:

- Dry production decreased 0.47 Bcf/d on the week. Most of the decrease came from the East (-0.32 Bcf/d) and South Central (-0.10 Bcf/d) regions. The Mountain region also saw a small decrease (-0.04 Bcf/d), while the Pacific and Midwest both saw relatively small changes week over week.

- Canadian net imports increased 0.41 Bcf/d, mainly because of increased imports into the Northeast and Midwest.

Demand:

- Domestic natural gas demand decreased 1.01 Bcf/d week over week. Decreases in demand were seen across the board, with Res/Com demand falling 0.43 Bcf/d, Power demand falling 0.41 Bcf/d, and Industrial demand falling 0.17 Bcf/d.

- LNG exports increased 1.41 Bcf/d mainly due to Sabine Pass and Corpus Christi rebounding from last week after resolving operational issues. Mexican exports decreased 0.08 Bcf/d.

Total supply decreased 0.06 Bcf/d, while total demand increased 0.43 Bcf/d week over week. The ICE Financial Weekly Index report is currently expecting a draw of 15 Bcf. Last year, the same week saw a draw of 36 Bcf; the five-year average is a draw of 37 Bcf.