[contextly_auto_sidebar]

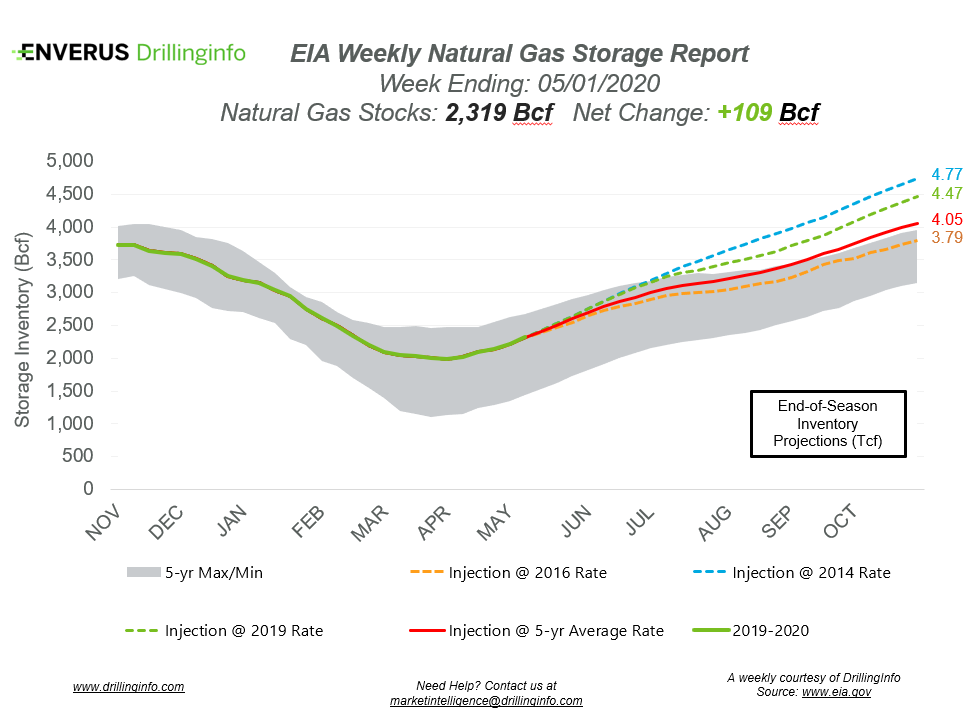

Natural gas storage inventories increased 109 Bcf for the week ending May 1, according to the EIA’s weekly report, marking the first triple-digit injection of the season. This was above the expected injection of 105 Bcf.

Working gas storage inventories now sit at 2.319 Tcf, which is 796 Bcf above inventories from the same time last year and 395 Bcf above the five-year average.

Prior to the storage report’s release, the June 2020 contract was trading at $1.974/MMBtu, roughly $0.030 above yesterday’s close. After the release of the report and at the time of writing, the June 2020 contract was trading lower, falling to $1.930/MMBtu.

After an explosion in August 2019, TETCO had another explosion on May 4, the second explosion in the past 9 months. This recent explosion, similar to the explosion in 2019, took place in Kentucky, reducing capacity on the pipeline from north to south on the east leg of the system from 1.35 Bcf/d to 0. Based on flow data from Enverus’ OptiFlo Gas, TETCO dropped ~0.60 Bcf/d of receipts from production meters in the Northeast as a result of the explosion, leaving 0.75 Bcf/d of gas needing to find a new home. While there is spare capacity in the Northeast that could replace the capacity lost from TETCO, the additional supply wasn’t seen hitting the available capacity, as other pipelines’ supply volumes remained similar to those as on the day before the explosion. Instead of other pipelines taking the extra supply, the gas was injected into storage for future use. Most of the gas was seen being injected into the Oakford and Steckman Ridge storage fields.

See the chart below for projections of the end-of-season storage inventories as of November 1, the end of the injection season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and Enverus’ analysis for the week ending May 7.

Supply:

- Dry natural gas production took a large fall for week ending May 7, dropping 3.08 Bcf/d. Decreases in the South Central (-1.89 Bcf/d), Mountain (-0.90 Bcf/d), and East (-0.31 Bcf/d) regions account for the production drop.

- Canadian net imports increased 0.20 Bcf/d on the week.

Demand:

- Domestic natural gas demand decreased 4.02 Bcf/d week over week. Res/Com demand accounted for the majority of the decrease, dropping 2.31 Bcf/d on the week, while industrial demand also fell 1.83 Bcf/d. Power demand saw a slight increase of 0.13 Bcf/d on the week.

- LNG exports decreased 0.09 Bcf/d on the week, while Mexican exports fell 0.16 Bcf/d.

Total supply decreased 2.88 Bcf/d, while total demand decreased 4.55 Bcf/d week over week. The ICE Financial Weekly Index report is currently expecting an injection of 87 Bcf. Last year, the same week saw an injection of 106 Bcf; the five-year average is an injection of 89 Bcf.