[contextly_auto_sidebar]

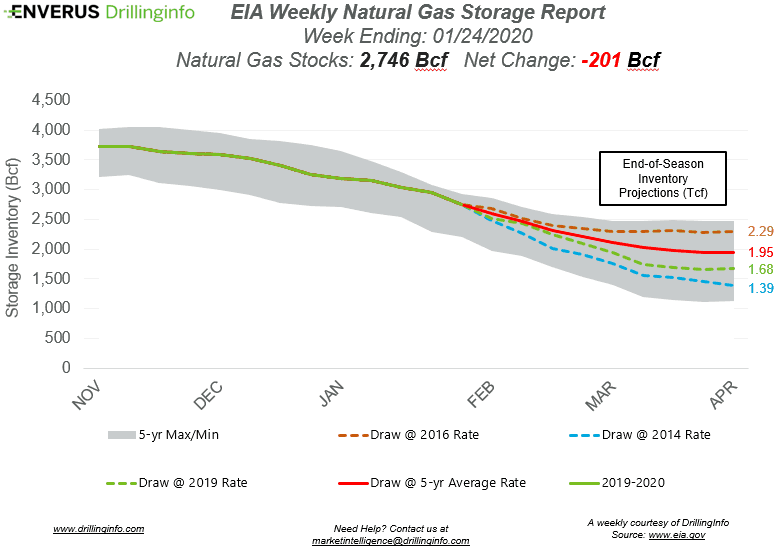

Natural gas storage inventories decreased 201 Bcf for the week ending January 24, according to the EIA’s weekly report. This was less than the expected draw of 204 Bcf.

Working gas storage inventories now sit at 2.746 Tcf, which is 524 Bcf above inventories from the same time last year and 193 Bcf above the five-year average.

Prior to the storage report release, the March 2020 contract was trading at $1.854/MMBtu, roughly $0.011 below yesterday’s close. After the release of the report, the March 2020 contract was trading at $1.835/MMBtu.

The February contract expired yesterday at $1.877/MMBtu, the lowest a February contract has expired since at least 2012. Since the February contract took over as prompt month, prices haven’t been able to garner any traction and have fallen over $0.30/MMBtu. Weather has been the main culprit for the price weakness, as the winter has been very mild overall.

Current weather forecasts from NOAA’s Climate Prediction Center show the 6-to-10-day forecast with below-average temperatures in the southern Rockies and from western Texas to Southern California; from eastern Texas up to Michigan and to the east shows above-average temperatures. The 8-to-14-day forecast shows a similar pattern, but with additional below-average temperatures in the northern Midwest.

See the chart below for projections of the end-of-season storage inventories as of April 1, the end of the withdrawal season.

This Week in Fundamentals

The summary below is based on Bloomberg’s flow data and DI analysis for the week ending January 30.

Supply:

- Dry production increased 0.03 Bcf/d on the week. Most of the increase came from the Mountain region (+0.09 Bcf/d) and the South Central (+0.06 Bcf/d), with an offset coming from the East (-0.12 Bcf/d). The Midwest saw a relatively small increase, while the Pacific saw a relatively small decrease.

- Canadian net imports decreased 0.49 Bcf/d, mainly due to decreased imports into the Northeast.

Demand:

- Domestic natural gas demand decreased 11.59 Bcf/d week over week. Res/Com demand accounted for the majority of the decrease, falling 8.48 Bcf/d on the week. Power and Industrial demand also decreased, falling 2.30 Bcf/d and 0.81 Bcf/d, respectively.

- LNG exports increased 0.93 Bcf/d, due to Sabine Pass and Cove Point ramping back up to normal levels after the prior week was down, as well as Freeport shipping volumes to the facility on train 2. Mexican exports increased 0.53 Bcf/d, due to the completion of maintenance on Valley Crossing.

Total supply decreased by 0.47 Bcf/d, while total demand decreased 10.57 Bcf/d week over week. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a weaker draw next week. The ICE Financial Weekly Index report is currently expecting a draw of 130 Bcf. Last year, the same week saw a draw of 237 Bcf; the five-year average is a draw of 148 Bcf.