[contextly_auto_sidebar]

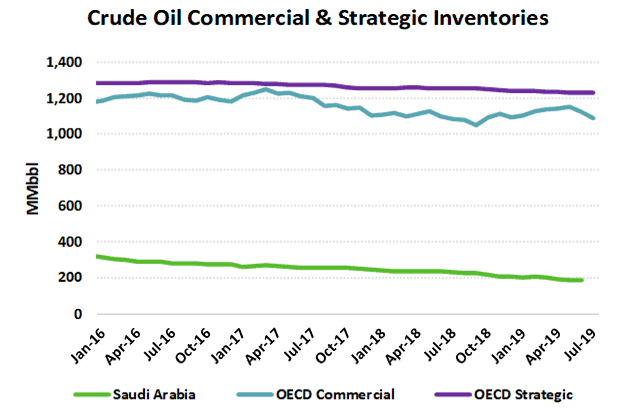

Roughly 5.7 MMbbl/d, more than half of Saudi Arabian crude production, was knocked offline early Saturday morning in a surprise drone attack coordinated by Houthi rebels in Yemen. The attack damaged two major facilities: the Hijra Khurais oil field (one of the country’s largest) and Abqaiq (the world’s biggest crude stabilization and processing facility). With these two targets, the attack struck directly at the heart of the Saudi oil industry. In particular, the attack on the crude treatment facility in Abqaiq hit a key chokepoint in Saudi Arabia’s export-oriented crude infrastructure. So central is the facility that it processes roughly 7 MMbbl/d out of the Kingdom’s 9.75 MMbbl/d current production, much of which goes to export markets. With Abqaiq offline, Saudi Arabia will struggle to maintain current exports of 6.8 MMbbl/d without drawing down on its 187.9 MMbbl/d of inventories located around the world.

Any attack on Saudi Arabia’s oil infrastructure is bound to rattle oil markets because the affected volumes account for around 5% of world supply. The Kingdom is also one of a small number of oil-producing countries with spare production capacity and has long been regarded as the “central bank” of oil markets due its ability to increase or decrease production with relative ease. It is also important to note that Saudi Arabia currently holds the lion’s share of global spare capacity (2.4 MMbbl/d of the global total of 3.21 MMbbl/d, according to the International Energy Agency).

What Comes Next?

The size of disruption is massive compared with other supply outages we’ve seen elsewhere in recent years. Now the question is how long it will last. Indeed, 187.9 MMB of Saudi inventories amounts to only a little over one month’s cover for the 5.7 MMbbl/d of production shut-in because of the attacks. Saudi officials have pledged to restore 2 MMbbl/d of lost production by Monday, which should stretch out inventories by another couple of weeks. Saudi Aramco’s pre-staging of these barrels in Egypt, Rotterdam, and Okinawa will mean the timing of deliveries may not be immediately affected either. Due to this inventory cushion, Saudi Aramco customers are not likely to see their volumes impacted if the disruption is short-lived. But if the damages at Abqaiq and Hijra Khurais prove to be especially severe, then the world oil market is going to need another supply buffer to fall back on until repairs can be completed.

The good news is that global crude inventories remain relatively high despite recent declines. In addition, as recently as Thursday the market was looking at worsening oversupply conditions heading into 2020, with continued growth in US tight oil production as well as increases from Norway and Brazil and low quota compliance by Iraq, Nigeria, Russia, and other members of OPEC+. In short, the loss of 5% of the world’s crude supply due to this weekend’s attack could not have happened at a better time.

The bad news is that the world’s confidence in Saudi spare capacity has been shaken to its core. One needs to seriously ask: How did Houthi rebels in Yemen manage to pull off such a spectacular attack from the other side of the Arabian Peninsula, and how did Saudi air defenses fail to stop it? Furthermore, does this weekend’s events foreshadow a deepening of the Saudi–Iran conflict, and what are the prospects for a major war in the Middle East Gulf? The United States has pledged its support to Saudi Arabia, claiming that the attack was carried out by Iran using cruise missiles; this raises the very real prospect of US airstrikes against targets inside Iranian territory. The potential for further escalation would increase, potentially leading to war. Even if the Saudi supply disruption can be managed in the short term by drawing on the Kingdom’s inventories and those held in commercial and strategic stockpiles around the world, a significant geopolitical risk premium will likely remain in the market for some time unless hostilities ended quickly.

The United States Is Not a Swing Producer

The public seems to believe that US tight oil production can ramp up immediately. Unfortunately, that is simply not the case. The crude market thinks about spare capacity, or the barrels that are sitting on the sidelines that could be brought online quickly if necessary. To have spare capacity implies having existing oil fields that are being willfully kept offline until their production is needed by the market. That is simply not how US tight oil production works. There is no central authority in the US—no national oil company—that can simply open a spigot and make the oil flow. US production comes from hundreds of thousands of individual wells controlled by hundreds of privately owned and publicly traded companies. Boosting tight oil production in the United States means increasing capital expenditures on rigs, completion crews, and infrastructure (not to mention the thousands of hours of analysis and planning that take place before capital budgeting decisions are made). None of this can be done overnight.

In addition to the challenges mentioned above, the major limiting factor today in US operators’ ability to grow the Permian Basin (the most prolific basin in the United States) is infrastructure bottlenecks, especially for natural gas and natural gas liquids (NGL) that are co-produced with crude. While it is true that a major buildout is underway for crude oil pipeline capacity out of the Permian, capacity to move associated natural gas remains tight, and NGL fractionation capacity at the Gulf Coast could be easily overwhelmed. Furthermore, sustainable export capacity for crude oil off the US Gulf Coast sits currently just below 4.5 MMbbl/d (with around 3 MMbbl/d already being used). Of course, there is also the difference in quality one has to consider when comparing Permian and Saudi crude; the former is very light and sweet, while the latter leans toward medium sours. Even if the United States was able to act as a swing producer (it is not), the grades produced in the US (and in the Permian basin in particular) are not a good replacement for the Saudi grades that were knocked offline.

Although the United States is unlikely to swoop in as a surprise swing producer, any increase in crude prices that results from this weekend’s events will certainly benefit US producers. Indeed, these companies have been under pressure from shareholders to keep spending within operational cash flow. A higher flat price environment would go a long way toward those ends. But whether it translates to increased capital expenditure is another question; if US producers see that the Saudis can manage the current outage by drawing down inventories while they bring damaged equipment back online, they may decide to sit on the sidelines and reap the benefit of higher profit margins.

Will 2020 capital budgets be increased compared to 2019? Only if the price of West Texas Intermediate jumps to the mid-60s and stays there… for a long time. If there is the expectation in the market that the price jump will be short-lived (i.e., weeks, not months), you will see limited response from US operators. But if there is a sustained mid-$60 to $70 price, the US would likely grow crude production by about 2 MMbbl/d per year again (just like in 2018) instead of the 1 MMbbl/d growth expected in 2019. Still, that is only an incremental 1 MMbbl/d increase—hardly enough to cover the volumes knocked offline in Saudi Arabia on Saturday. By the time those incremental US barrels are on the market, the stabilization and processing facility in Abqaiq would have long been restored to normal operations.