Financial services are the keystone of connecting capital for nascent energy transition technologies; however, the plethora of opportunities is staggering and makes deploying smart capital challenging. Explore how various energy transition technologies and opportunities align most effectively with different capital pools. Gain insights into the risk profiles of these technologies to navigate the ongoing energy transition.

This e-book is based off the report published by the Enverus Energy Transition Research team, Ways to Play | Energy Transition Opportunities for Finance Participants, published July 2, 2024. Enverus Intelligence® Research clients can view the full report here .

Enverus Intelligence® Research, Inc., a subsidiary of Enverus, provides the Enverus Intelligence® | Research (EIR) products. See additional disclosures.

Select “Get Started” below if you would like to unlock Energy Transition Research’s in-depth reports on energy transition topics, available exclusively for Enverus Intelligence® Research

(EIR) members.

Research written by:

Ryan Notacker, Analyst, Enverus Intelligence® Research

Ivana Petrich, CFA, Analyst, Enverus Intelligence® Research

Morgan Kwan, P.Eng, Director, Enverus Intelligence® Research

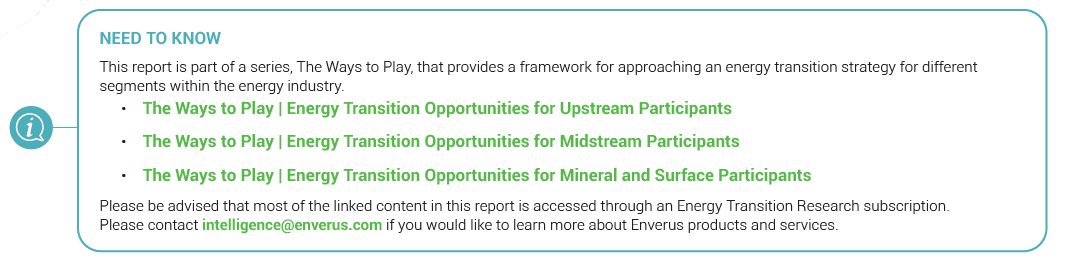

In this iteration of our “The Ways to Play” series, Enverus Intelligence® Research (EIR) identifies the critical investment criteria each capital pool requires and matches that with an energy transition technology, a general framework as to what firms should be spending more or less time on when considering capital deployment. EIR explore the core investment drivers for hedge funds, asset managers, investment banks, private equity, private credit and tax equity investors and match the energy transition technologies that are best suited to them (Figure 1). In today’s investment landscape, renewable energy technologies, such as solar and wind, remain cornerstone opportunities for investors – the purpose of this report is to raise awareness of some of the lesser-known and popularized technologies.

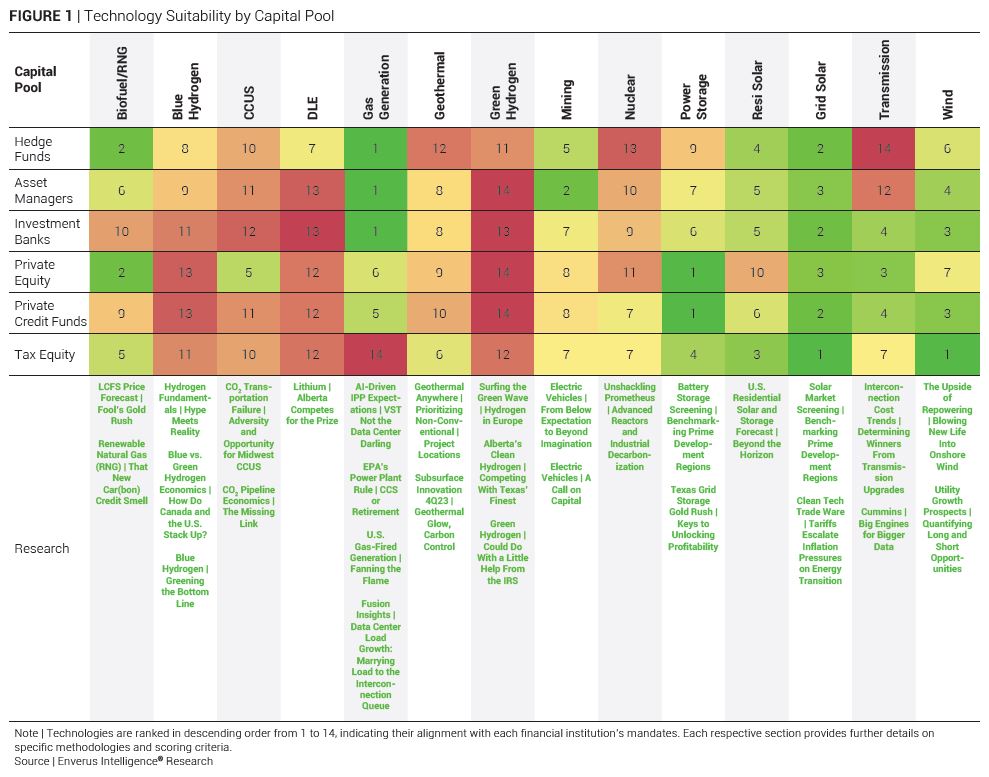

The stage of entry for participants financing the transition varies depending on their risk appetite and the maturity of climate solution technologies (Figure 2). Nascent technologies are at higher risk, with development more likely to be supported by government funding, venture capitalists investing in early-stage companies, impact capital such as philanthropic funds and, to a lesser extent, corporates themselves. A good example is the recent explosion of methane monitoring technologies ahead of Quad O with the more proactive oil and gas companies working with start-up companies to deploy new equipment.

EIR notes a gap between early, high-risk capital providers (e.g., venture capital and impact investing) and more traditional institutions like asset managers with pension fund and endowment mandates. As technologies and the energy transition market matures, they think there are opportunities within the current “capital dead zone” for different capital pools to participate in and take an early mover advantage.

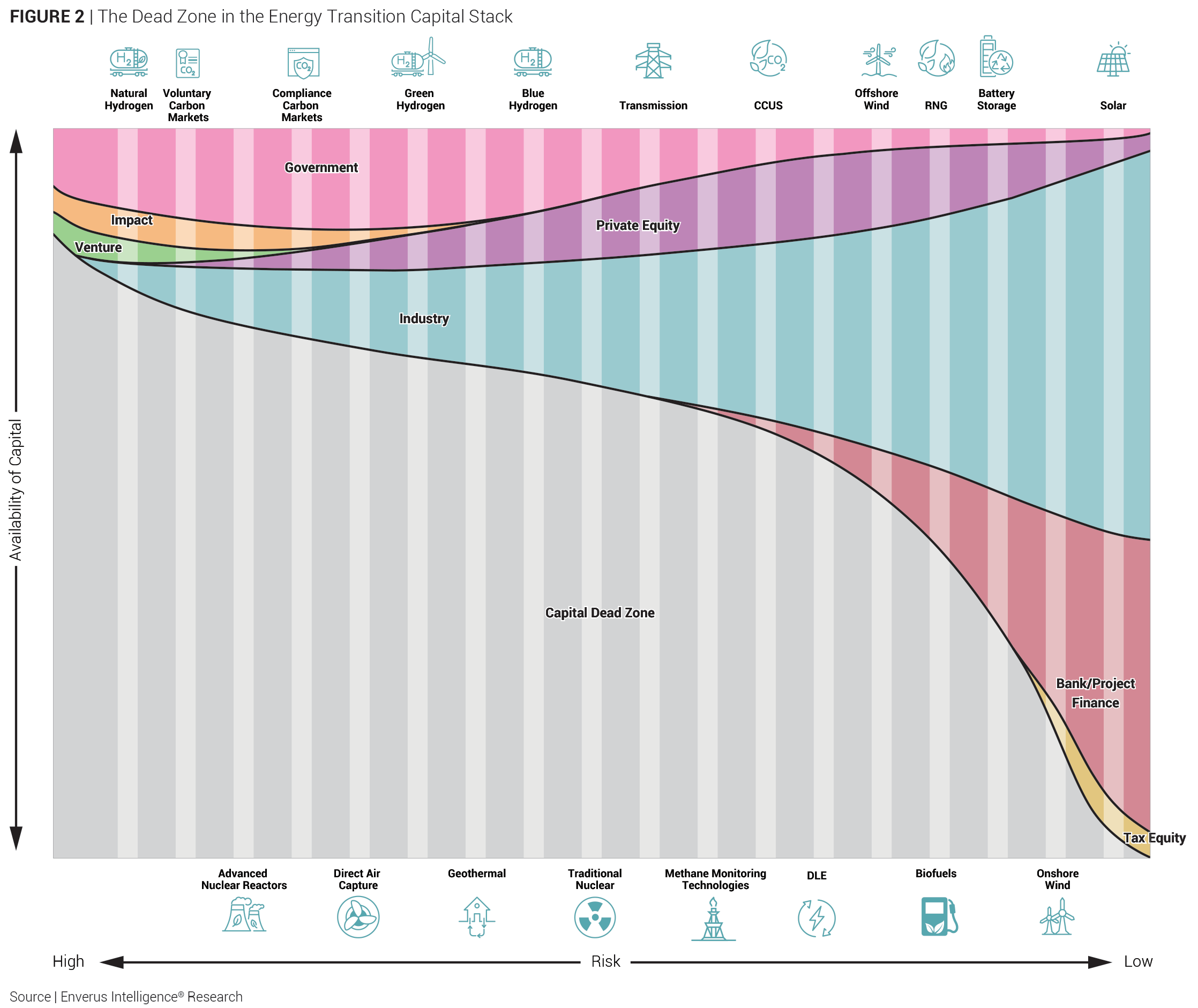

For the scope of this report, we define hedge funds as investment vehicles that pool capital and employ diverse strategies to profit in both rising and falling markets. These strategies favor highly liquid and volatile public equities that are exposed to a fundamental rate of change story that is translated into the price of the securities, ultimately profiting from market mispricing. Figure 3 shows how each of the technologies within our energy transition coverage score in these core hedge fund investment parameters – gas generation and grid and residential solar are the most favorable today. For hedge funds looking for ways to play in the energy transition, focusing efforts on equities that fall within these realms of technology should be prioritized.

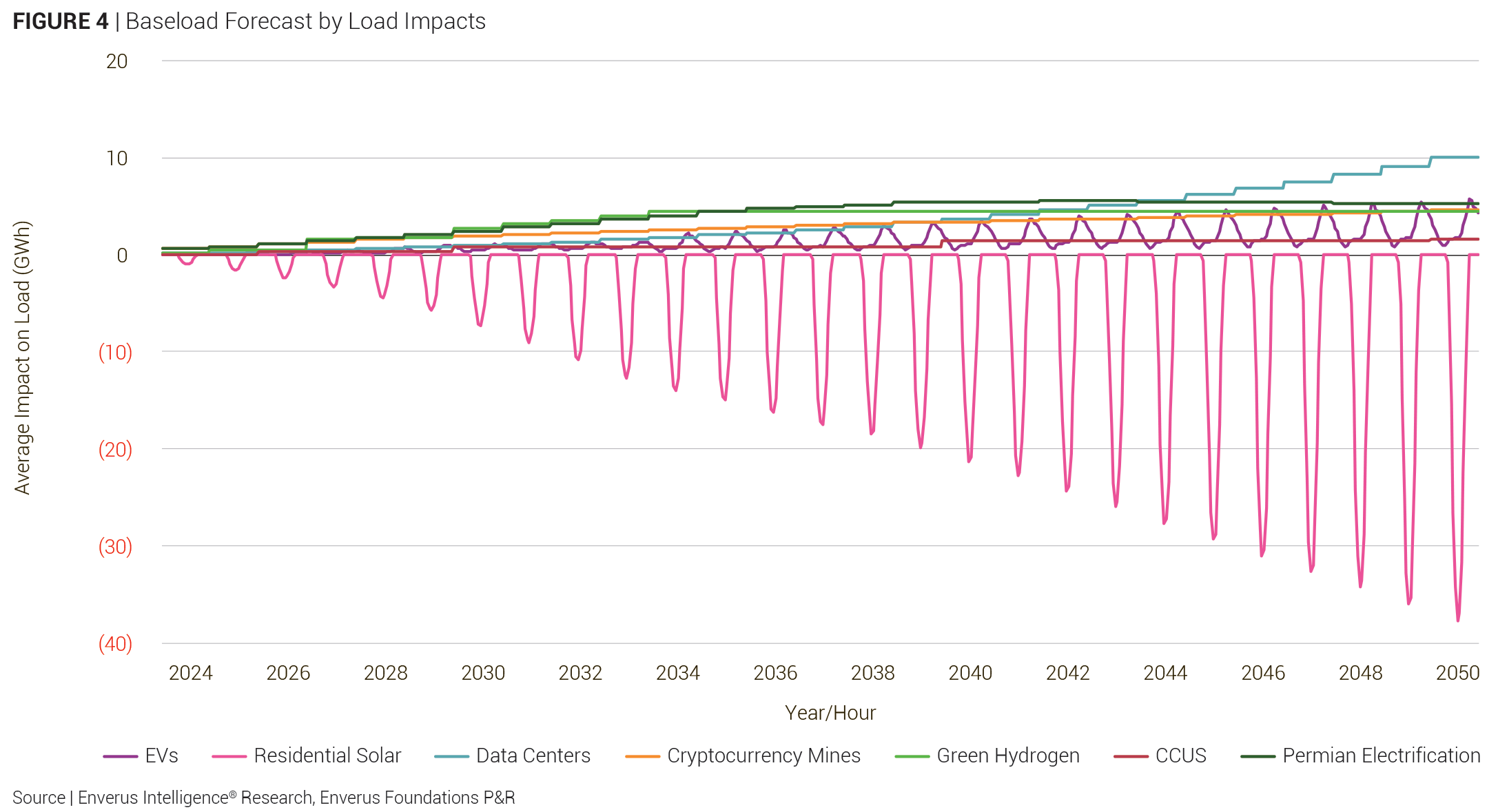

The fundamental secular bull thesis surrounding increasing power demand (Figure 4), especially around the deployment of ratable and clean energy for the growing data center rollout, will continue and contribute to the demand side tailwind for equities in both gas generation and the grid solar space. Conversely, EIR surmises that residential solar represents an attractive sector for hedge funds with short mandates to benefit from the highly volatile nature of the industry. The volatility in residential solar stems from their relatively high asset-level leverage and distressed corporate debt, paired with a highly interest rate-sensitive clientele.

While EIR is supportive of nuclear, geothermal and transmission, they think these technologies, as they stand today, are too thinly traded, not volatile enough and lack a rate of change for hedge fund participants to meaningfully deploy capital and generate alpha.

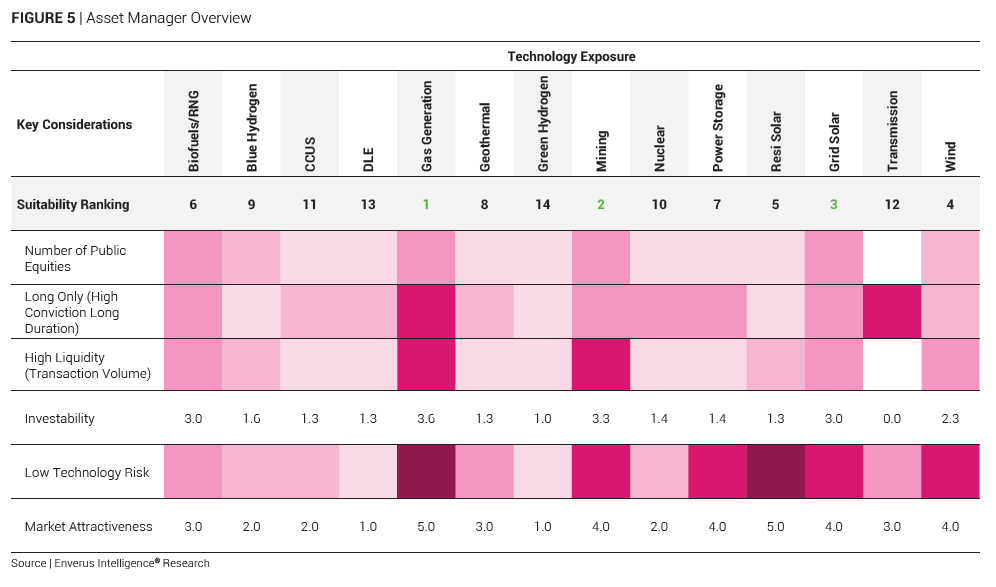

In this ways-to-play exercise, asset manager is defined as a firm that manages investment portfolios on behalf of institutional clients and accredited investors, such as pension funds, insurance companies, sovereign wealth funds and high-net-worth individuals. These firms target long-duration, high-conviction capital deployment opportunities into public markets and seek to minimize unnecessary risk for their client portfolios.

The bull theme for increased power production, including gas generation, continues and EIR concludes that it represents a logical place for asset managers to deploy capital, as seen in Figure 5. EIR view mining as an attractive sector as the pricing environment for metals and base commodities such as copper from the rollout of fiber optic cables has resulted in a supply crunch, which is anticipated to linger as the data center construction buildout thesis plays out.

The path to commerciality for DLE and green hydrogen is required before logical deployment of capital from asset managers can be realized. As most projects remain in the pilot stage, EIR would require the market to mature and derisk before they recommend the sectors for asset managers’ portfolios. EIR would need to see more pure-play power storage equities to make it an attractive space. However, the technology and long thesis are supportive, particularly when paired with grid-scale solar deployment opportunities. Residential solar equities are more volatile and speculative due to the leverage profile of the corporates. This interest rate exposure burdens the equities in the sector and does not fit traditional asset managers’ high conviction and long-duration holding period.

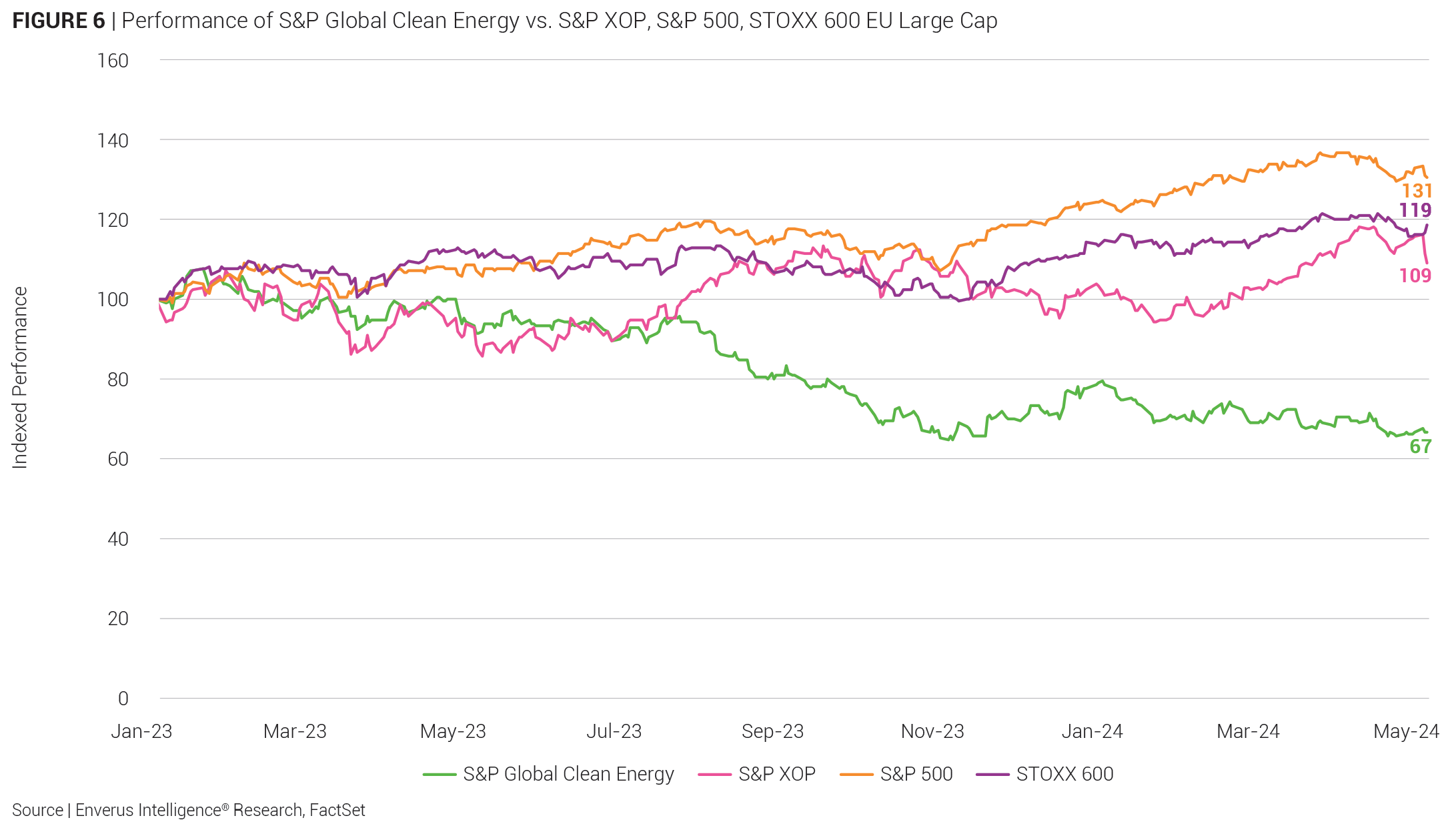

ESG asset managers are already actively deploying capital into the energy transition and are not an area of focus for this report. EIR notes a relative underperformance of clean energy-dedicated funds relative to the market recently (Figure 6) and considers that investors will have to get much more selective in incorporating which specific technologies they invest in rather than investing in clean energy as a whole.

Managers have expanded their sustainable investment teams, further integrating ESG factors into their investment process and focusing on stewardship. While headlines are quick to report that ESG has peaked based on high-profile withdrawals from global investor coalitions like Climate Action 100+, EIR sees it as a sign of capabilities moving in house. This will lead to a broader range of opportunities being assessed rather than applying a one-size-fits-all approach to climate engagement. Despite EIR’s long-term view that gas-fired power generation will largely be displaced by renewables, EIR still view the onset of the AI data center boom cements oil and gas’ role in the energy transition, more so than most ESG portfolios currently reflect.

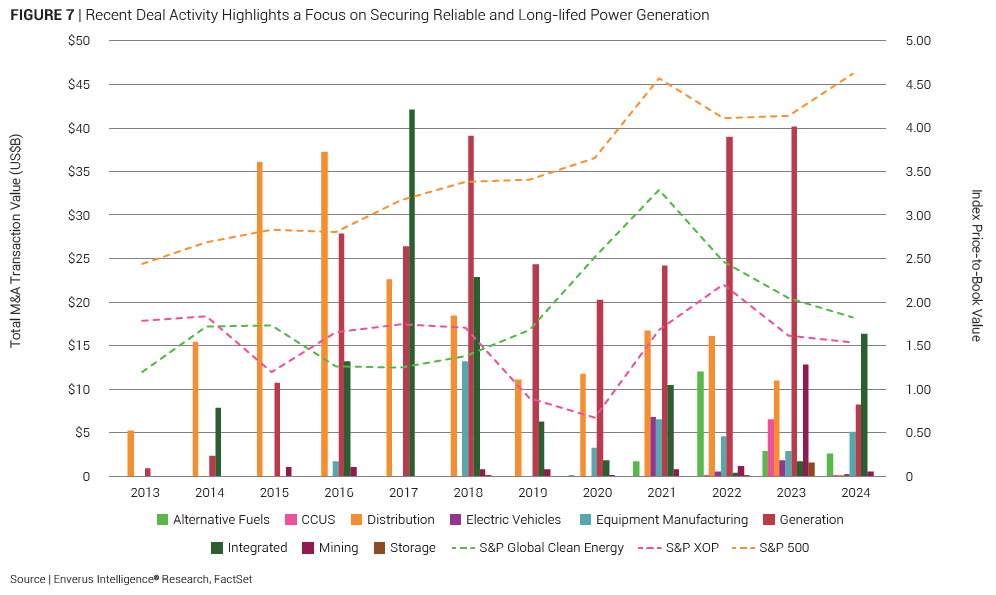

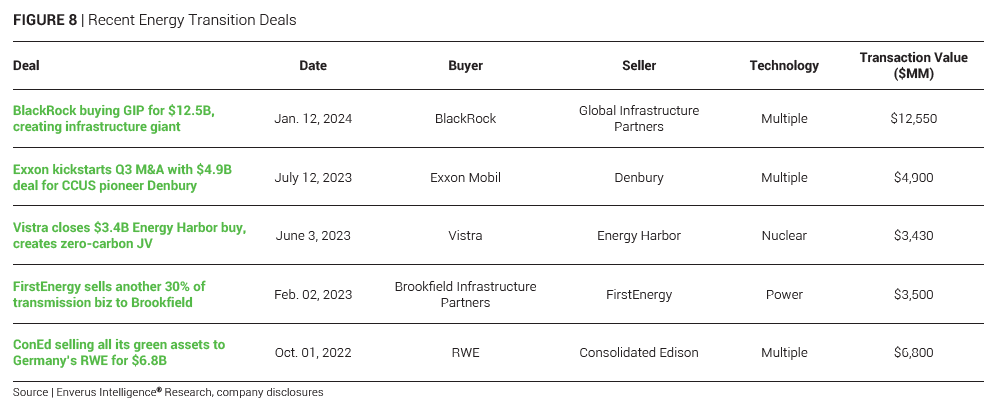

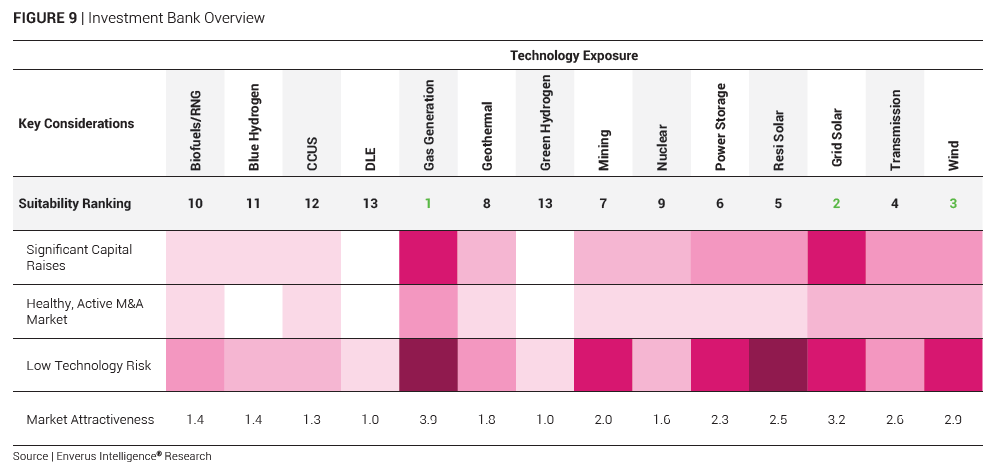

In “The Ways to Play” series, investment banks are defined as financial institutions that provide a range of services for their clients, including underwriting, facilitating mergers and acquisitions, brokering equity issuances or raising debt financing. They generate fee events primarily through advisory services and underwriting fees and benefit most from industries that require significant capital raises (in both frequency and offering sizes above $100 million), possess a healthy and active M&A market (50 deals above $100 million in the past three years) and are generally lower technology risk to support project financing (Figure 7). EIR sees the proportion of energy-related deal activity with a transition thesis continue to ramp up (Figure 8), so despite being smaller on a relative basis, it still demands that investment banks expand to include the sector in their coverage.

Given these considerations, gas generation, grid solar and wind is scored as the most lucrative sectors for the sell side to participate in (Figure 9). All three technologies require recurring capital raises (either asset-backed or corporate), are exposed to strong deal activity and typically have long-term, fixed-price contracts with creditworthy counterparties due to their low technology risk profiles.

EIR does caveat that although certain technologies might be in the early innings of market activity, they still represent opportunistic sectors for mid-market and lower mid-market participants. However, more advancements in DLE and green and blue hydrogen are required for the sectors to ascend the EIR rankings of opportunistic technologies.

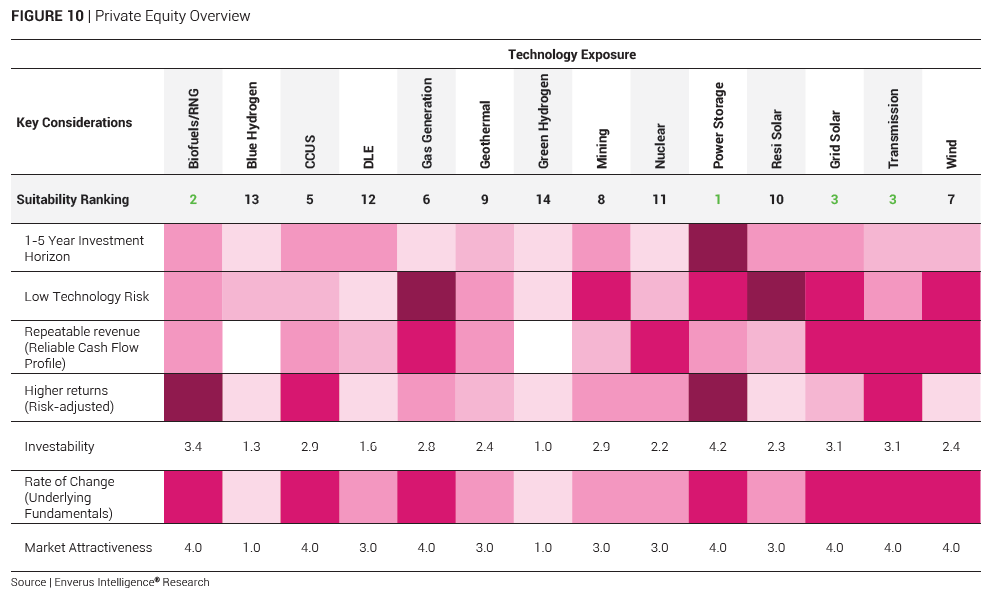

EIR defines private equity firms as investment managers that acquire private companies or take public companies private, restructuring them to improve their value before eventually selling them for a profit. They generate income through management fees charged on committed capital and performance fees (carried interest) based on the profits from successful investments. They typically look to earn a multiple on their invested capital within a one-to-five-year investment horizon, prefer companies with lower technology risks, are exposed to a fundamental growth story on a macro basis, have strong recurring cash flow profiles and pursue projects that have a higher risk-adjusted return profile. By providing capital and strategic guidance, they accelerate the path to commerciality for early-stage projects or boost returns for mature operating companies.

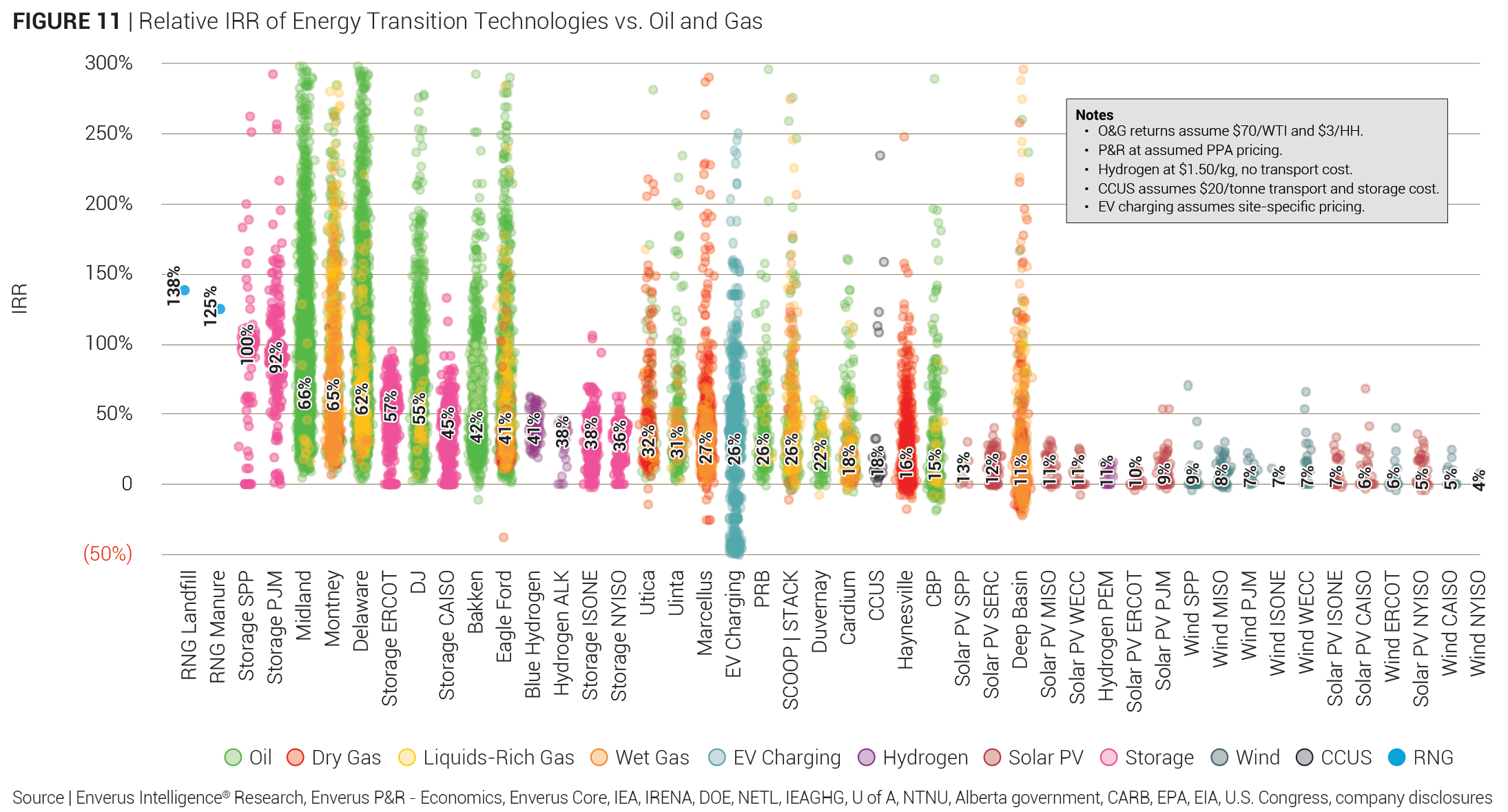

With these parameters in mind, power storage, biofuels/RNG, grid solar and transmission are viewed as compelling areas of energy transition for private equity (Figure 10). Power storage stands out due to revenue streams derived from multiple value propositions, including energy arbitrage, frequency regulation, demand response and capacity services. Taken together these lead to attractive returns, particularly as grid reliance on renewable energy increases. Biofuels and RNG also represent excellent spaces for private equity to incorporate into their portfolios, as advancements in low-carbon fuels technology and economies of scale reduce production costs, enhance profitability and create attractive exit opportunities through strategic sales or public offerings. When it comes to generating returns, EIR notes that RNG and power storage have the potential to outcompete some oil and gas plays on an IRR basis (Figure 11), but identifying these unique opportunities requires a data-driven approach.

The most compelling rate of change story is the buildout of data centers and the increasing call for power as a whole. This acts as a revenue growth catalyst for all power generation assets, but especially those that can meet baseload power requirements (gas generation and nuclear) and those that satisfy low-carbon generation standards (solar, storage, wind). Paired with low technology risk and a one-to-five-year investment horizon, power storage and grid solar screen as favorable areas to play for private equity.

Conversely, hydrogen is viewed as being too speculative and early-stage for private equity. While EIR is supportive of government derisking and regulatory support through tax credits, they still are in a wait-and-see position until a pattern of cash flow streams emerges through committed offtake agreements and wider adoption of the technology takes hold. Geothermal and DLE are on the cusp of being a valid area of participation, but until project commercialization is achieved, their current state of technology risk and low repeatable revenue put them out of the running.

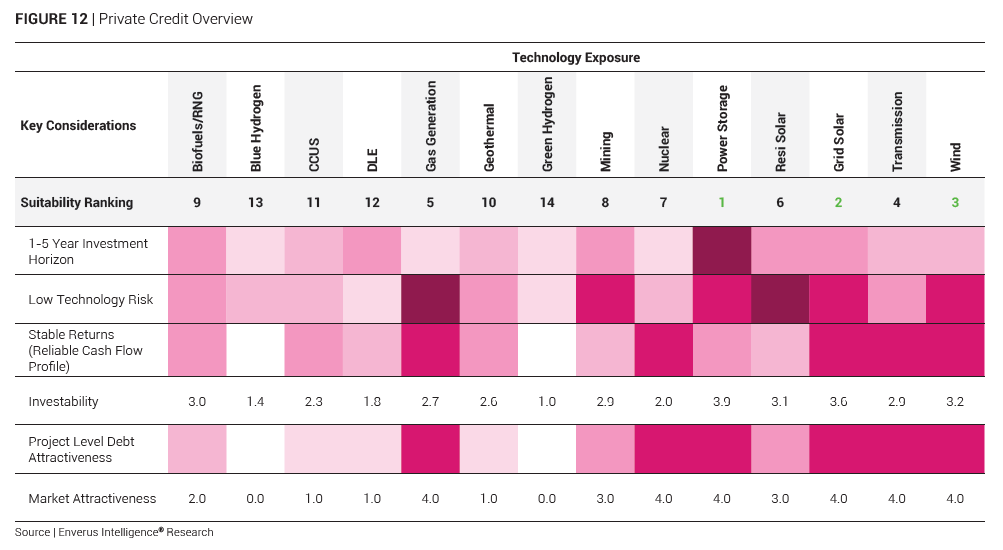

In this analysis, private credit funds are defined as investment vehicles that provide bespoke debt financing to private and public companies, often including mezzanine, direct lending and distressed debt strategies. They generate returns through interest payments, origination fees and, sometimes, equity participation via warrants or convertible notes, targeting higher yields compared to traditional fixed-income securities and corporate debt. The technologies are scored on their key considerations for making investment decisions, assessing the creditworthiness of the borrower, the ability to return investment within one to five years, the stability and growth potential of the underlying cash flows and the technological maturity and scalability of the energy transition initiatives being financed.

Private credit funds can play a vital role in energy transition by offering flexible financing solutions to renewable energy projects and clean technology companies that may lack access to traditional bank financing. This is most often realized through infrastructure-type investing.

Technologies that screened well for private credit are project-based with investable debt tied to the projects themselves (Figure 12). Power storage projects’ investability is bolstered by their reliable returns. EIR has analyzed which battery size, operating strategy and location for storage assets in ERCOT are the most profitable, as well as ranked the most attractive regions for battery storage developers looking to enter or expand in the U.S. Utility-scale solar energy projects also offer compelling opportunities for private credit investors due to their mature technology and established market. The predictable cash flows generated from long-term PPAs and feed-in tariffs provide a reliable income stream that is ideal for debt financing. Wind and transmission projects typically have lower operational risk and benefit from significant regulatory and policy support, ensuring a stable investment environment. Additionally, the rollout of PPAs with data centers, which require a consistent and substantial energy supply, underscores a bullish sentiment by linking robust and steady demand with ratable generation.

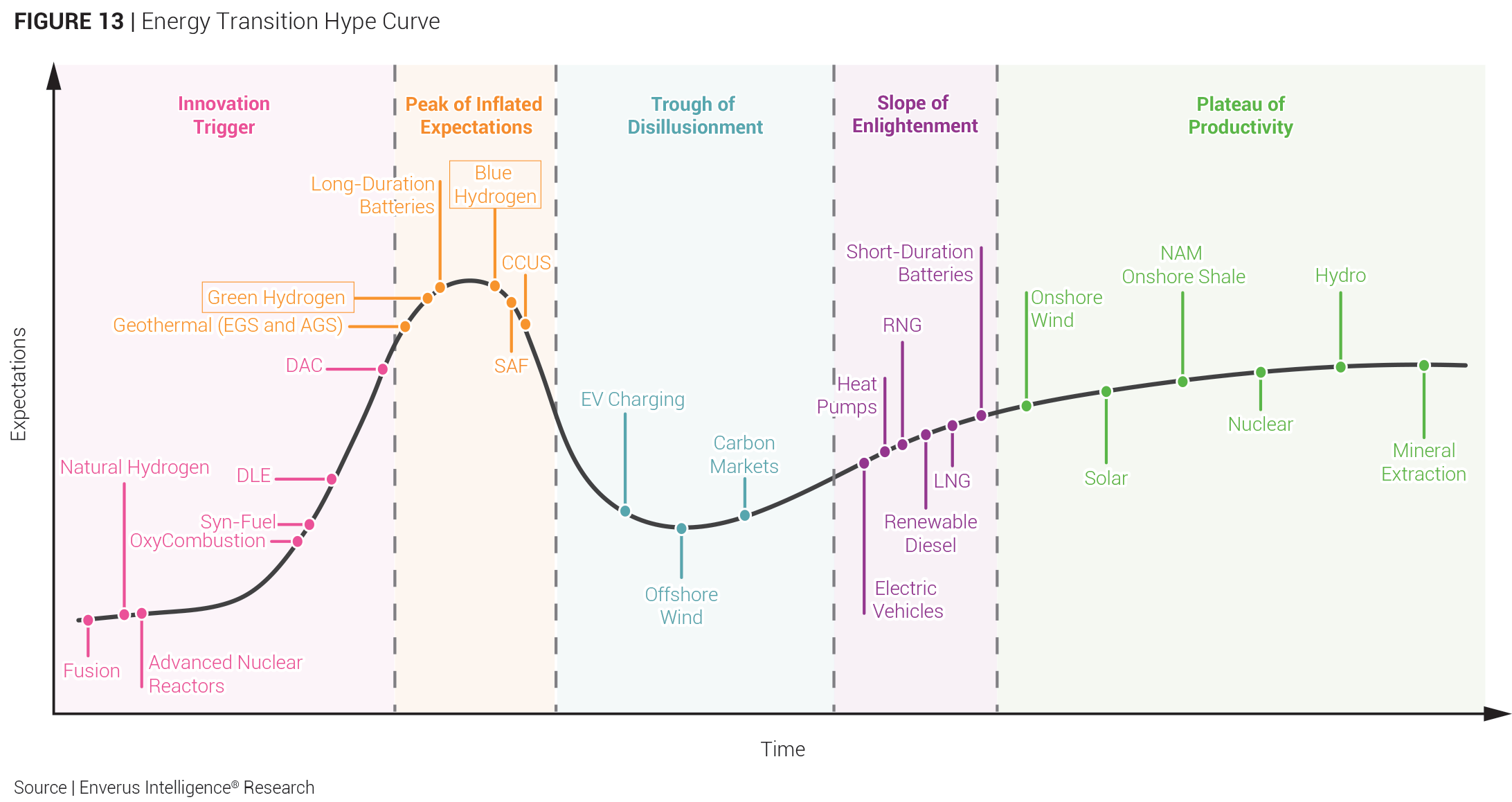

DLE is less suited for private credit investment due to its emerging status and higher technological and market risks. As a relatively new technology, DLE faces uncertainties in commercial scalability that a debt investor requires. This contributes to a higher risk profile, making it less attractive for private credit investors seeking stable and predictable returns. Similarly, while promising as a player in the future energy landscape, hydrogen is currently in the early stages of commercialization. EIR suggests credit investors remain on the sidelines until it ascends beyond the hype curve (Figure 13).

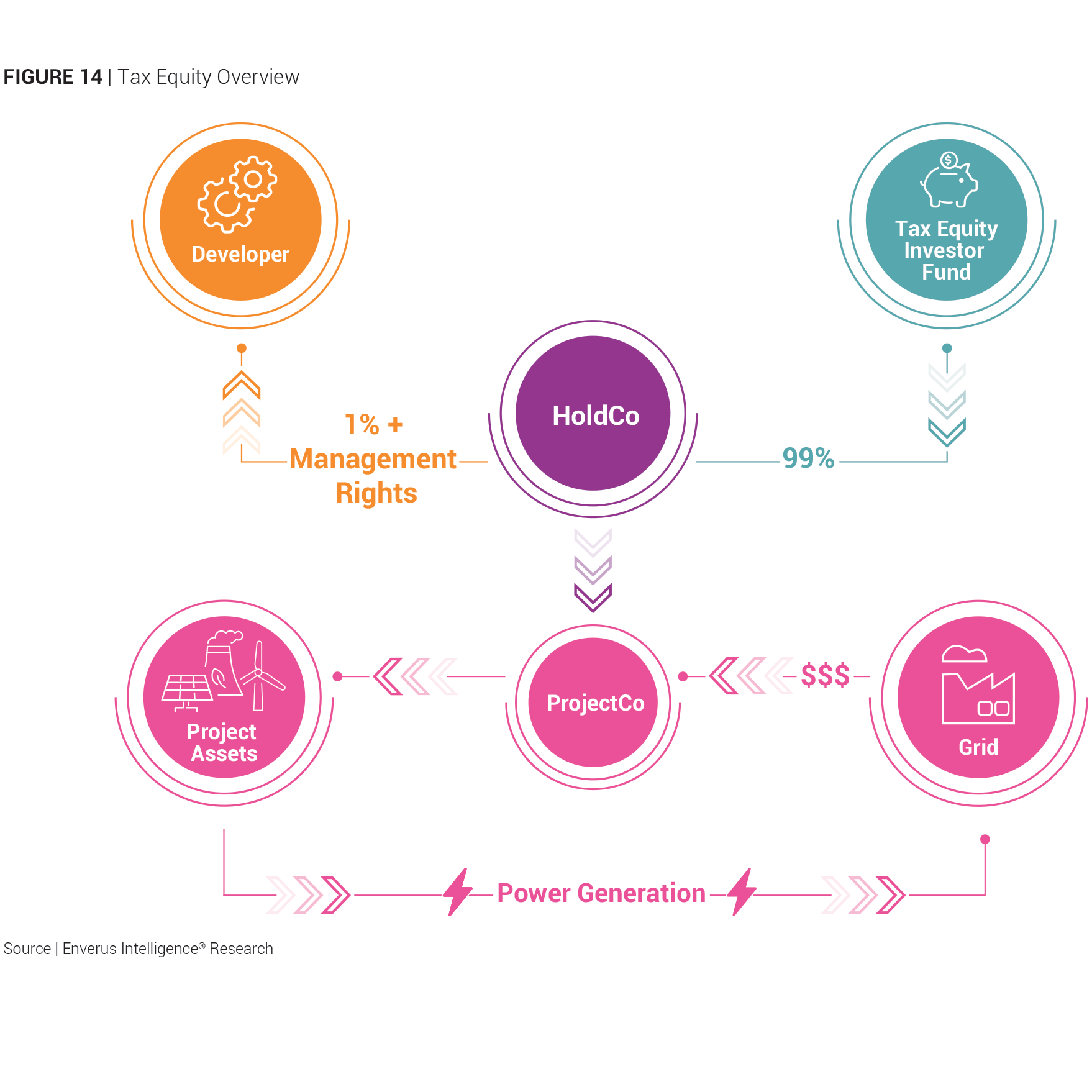

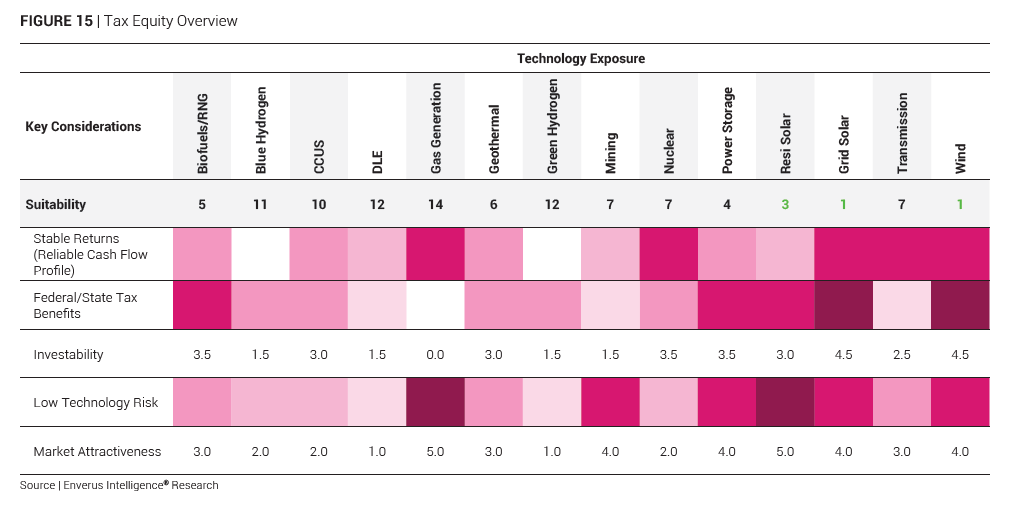

Grid solar, wind and residential solar screen well for tax equity investors (Figure 15) because of several key factors. Firstly, these technologies benefit significantly from ITCs and PTCs, providing substantial financial incentives that enhance project economics. Grid-scale solar and wind projects typically involve large capital investments, making them attractive for tax equity financing as they can absorb sizable tax credits over time, thereby reducing investors’ tax liability. Additionally, these projects often have established revenue streams through long-term PPAs that mitigate revenue risks and provide predictable cash flows essential for investors seeking stable returns. While smaller in scale, residential solar projects also benefit from ITCs and can be aggregated to attract tax equity investors looking to diversify their portfolios with distributed generation assets.

Gas generation screens poorly for tax equity investors primarily because of its limited eligibility for renewable energy tax incentives designed to promote clean energy deployment. Additionally, while hydrogen projects aimed at reducing carbon emissions through processes like CCS for blue hydrogen (section 45Q) or electrolysis using renewable energy for green hydrogen are exposed to tax incentives, the market is still in its infancy. They require careful evaluation of technological maturity, market demand and regulatory support to effectively manage investment risks before they compete with more established technologies for tax equity investments.

Grid solar, wind and residential solar screen well for tax equity investors (Figure 15) because of several key factors. Firstly, these technologies benefit significantly from ITCs and PTCs, providing substantial financial incentives that enhance project economics. Grid-scale solar and wind projects typically involve large capital investments, making them attractive for tax equity financing as they can absorb sizable tax credits over time, thereby reducing investors’ tax liability. Additionally, these projects often have established revenue streams through long-term PPAs that mitigate revenue risks and provide predictable cash flows essential for investors seeking stable returns. While smaller in scale, residential solar projects also benefit from ITCs and can be aggregated to attract tax equity investors looking to diversify their portfolios with distributed generation assets.

Gas generation screens poorly for tax equity investors primarily because of its limited eligibility for renewable energy tax incentives designed to promote clean energy deployment. Additionally, while hydrogen projects aimed at reducing carbon emissions through processes like CCS for blue hydrogen (section 45Q) or electrolysis using renewable energy for green hydrogen are exposed to tax incentives, the market is still in its infancy. They require careful evaluation of technological maturity, market demand and regulatory support to effectively manage investment risks before they compete with more established technologies for tax equity investments.

Let’s get started!

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Ready to Subscribe?

Ready to Get Started?