The Big Beautiful Bill Act reshapes U.S. energy policy, impacting tax credits and project economics across sectors.

Enverus Intelligence® Research, Inc., a subsidiary of Enverus, provides the Enverus Intelligence® | Research (EIR) products. See additional disclosures.

Select “Get Started” below if you would like to unlock Energy Transition Research’s in-depth reports on the power/supply demands of data centers and other energy transition topics, available exclusively for EIR members.

Research Written by:

This e-book provides a comprehensive analysis of the One Big Beautiful Bill Act (OBBBA) and its sweeping changes to U.S. energy policy, focusing on tax credit modifications and their impacts across clean fuels, renewables and CCUS sectors. Energy industry professionals are grappling with shortened eligibility windows for various tax credits, potentially affecting project timelines and economic viability. The e-book offers valuable insights into how these changes will influence different technologies, including clean hydrogen, solar, wind and enhanced oil recovery (EOR), helping stakeholders navigate the evolving regulatory landscape. By exploring the economic implications and providing data-driven analysis, this e-book equips readers with the knowledge needed to make informed decisions and adapt their strategies in response to the OBBBA’s transformative effects on the energy industry.

The One Big Beautiful Bill Act (OBBBA), signed into law July 4, 2025, has made significant changes to tax credits initially introduced by the 2022 Inflation Reduction Act. These changes primarily affect eligibility windows for various energy-related tax credits, impacting sectors like clean fuels, renewables, and carbon capture utilization and storage (CCUS).

The OBBBA was enacted as part of the budget reconciliation process for 2025, allowing the current administration to shape future energy policy. A key goal was to reduce overspending on tax credits for technologies that have achieved cost parity, such as electric vehicles, while redirecting funds to industries still requiring support. This strategic approach aims to optimize the allocation of tax incentives across the energy sector.

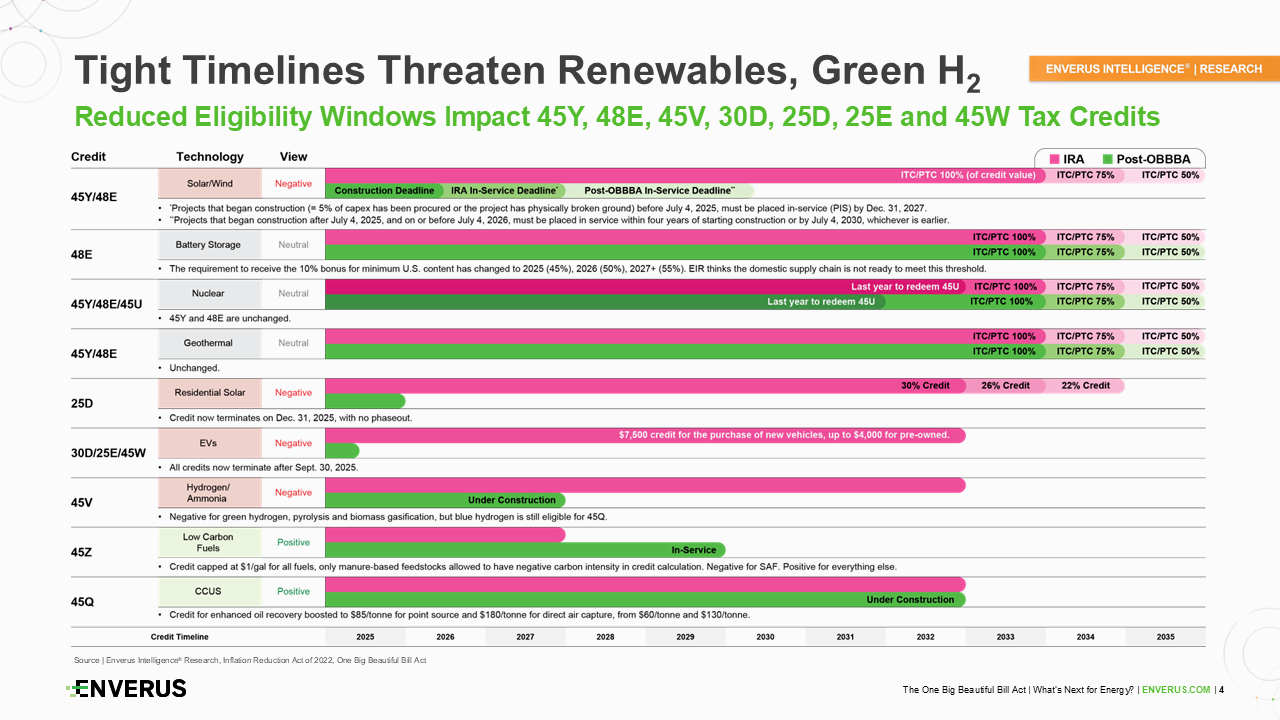

The OBBBA introduces several significant changes to the eligibility timelines for key federal tax credits, aimed at incentivizing clean energy. For solar and wind technologies, the 45Y and 48E credits have seen their eligibility windows drastically shortened, requiring projects to begin construction before July 4, 2026 to qualify. The 48E credit for battery storage systems, however, remains unchanged, while the timeline for the 45U nuclear energy credit has been slightly reduced, pushing its expiration date to 2031, a year earlier than before. Credits for geothermal systems remain stable, but the residential solar credit is set to expire at the end of this year, and the $7,500 electric vehicle (EV) credit will phase out by Sept. 30, 2025.

The clean hydrogen industry, eligible under the 45V credit, faces particularly steep changes with the eligibility window to begin construction reduced sharply from the end of 2032 to the end of 2027. This shortened timeline is expected to place substantial pressure on green hydrogen projects. In contrast, the 45Z credit for clean transportation fuels provides a rare exception, offering an extended eligibility period. The 45Q credit for carbon capture and storage remains unchanged, providing consistency for that sector. The implications of these timeline adjustments vary across industries, intensifying the pace required for many energy projects to start their development.

To qualify for these credits, it’s also important to note the “start construction” requirement. Currently, developers must either (a) spend 5% of the project cost or (b) initiate physical construction (e.g., shovels in the ground) to meet this requirement. Additionally, any project that begins construction within 12 months of OBBBA’s enactment will have up to four years to be placed in service to qualify. However, this definition may soon face stricter revisions, as a decision related to the Executive Order issued July 7 is expected Monday, Aug.18. If enacted, the revised policy could make it more challenging for projects to meet the “start construction” criteria, potentially reshaping qualification pathways for tax credits.

The 45Z tax credit for clean transportation fuels has seen its eligibility window extended from 2027 to 2029, offering modest economic gains for most fuels except sustainable aviation fuel (SAF). However, changes to SAF include an adjusted baseline rate, restrictions on negative emission rates in carbon intensity calculations, and new feedstock sourcing requirements. These adjustments will have varying impacts on fuel types, with some agricultural-based fuels potentially experiencing increased 45Z revenues.

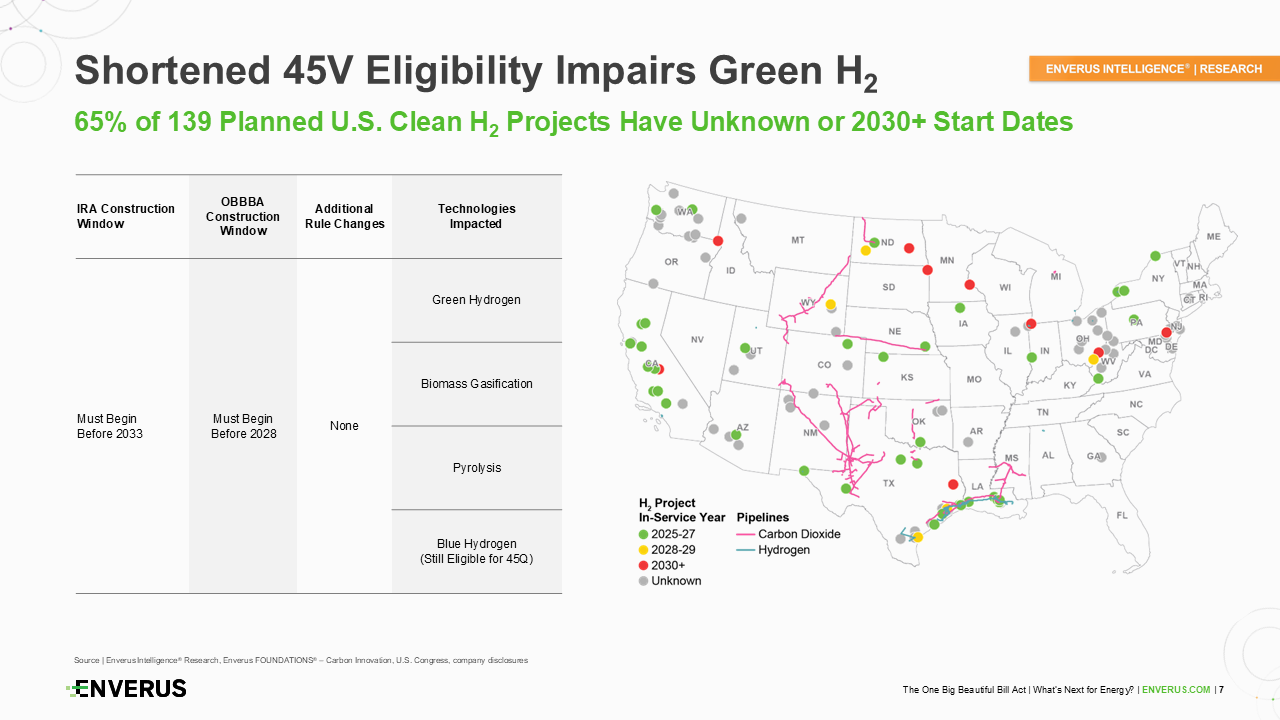

In contrast, the shorter eligibility window for the 45V tax credit, which supports clean hydrogen projects, presents significant challenges for the green hydrogen industry. The 45V is a production tax credit lasting 10 years from eligibility and offers up to $3 per kilogram of hydrogen, depending on carbon intensity. Originally, projects only needed to begin construction by the end of 2032 to qualify. However, under the new legislation, projects must now begin construction by the end of 2027. This change could have a pronounced impact on low-carbon hydrogen projects such as green hydrogen, biomass gasification and pyrolysis, as developers will need to accelerate their construction timelines to remain eligible. Many projects, 65% of the 139 planned U.S. clean hydrogen projects, either have in-service dates of 2030 or beyond, or no specified timeline, putting them at risk of missing eligibility. The 45V has the potential to reduce the levelized cost of hydrogen by up to 50%, meaning its absence could render many green hydrogen projects uncompetitive.

While the extended 45Z eligibility window is generally positive, its economic impact is muted by the dominance of other incentives like D3 RINs and LCFS credits. For example, landfill RNG projects see only a slight improvement in after-tax IRRs, from 60% to 62%. The limited impact is primarily because the 45Z credit only applies for five years, whereas D3 RINs can be claimed over the full project life. Similarly, the shortened 45V window adds pressure on developers of low-carbon hydrogen to accelerate their timelines or develop alternative production strategies. Blue hydrogen, however, remains eligible for the 45Q credit, providing a stable pathway for some hydrogen projects.

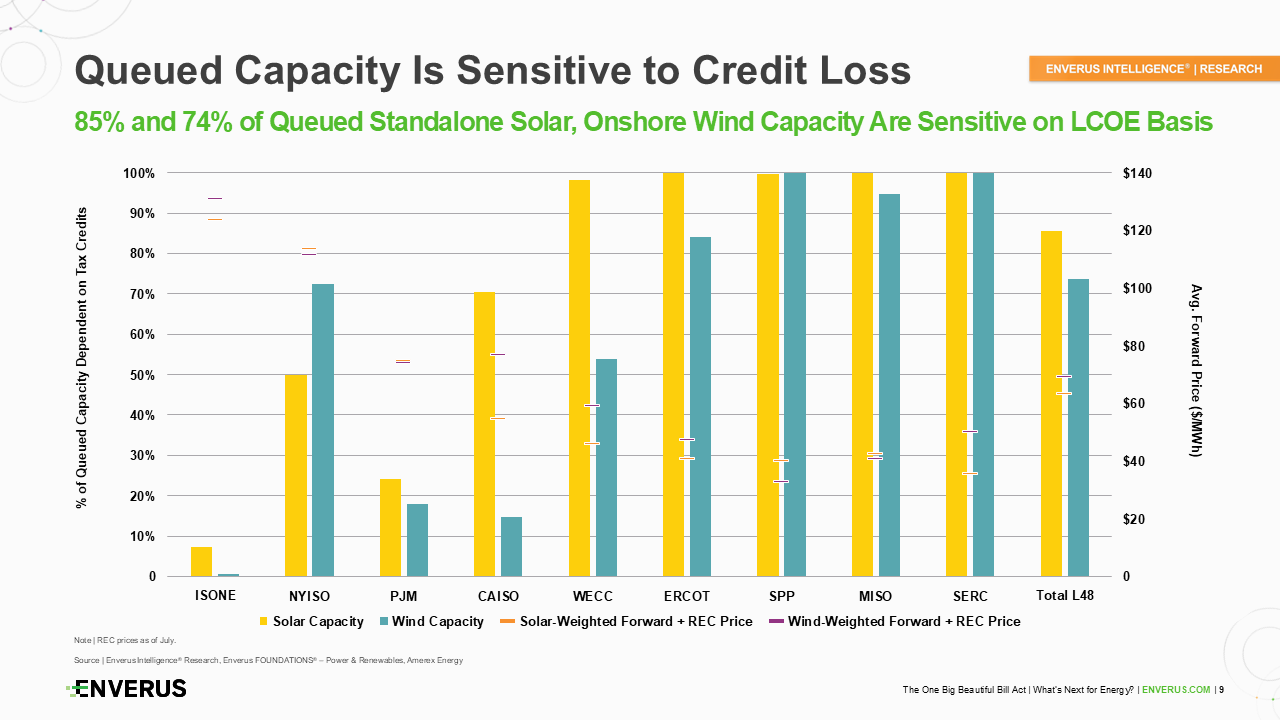

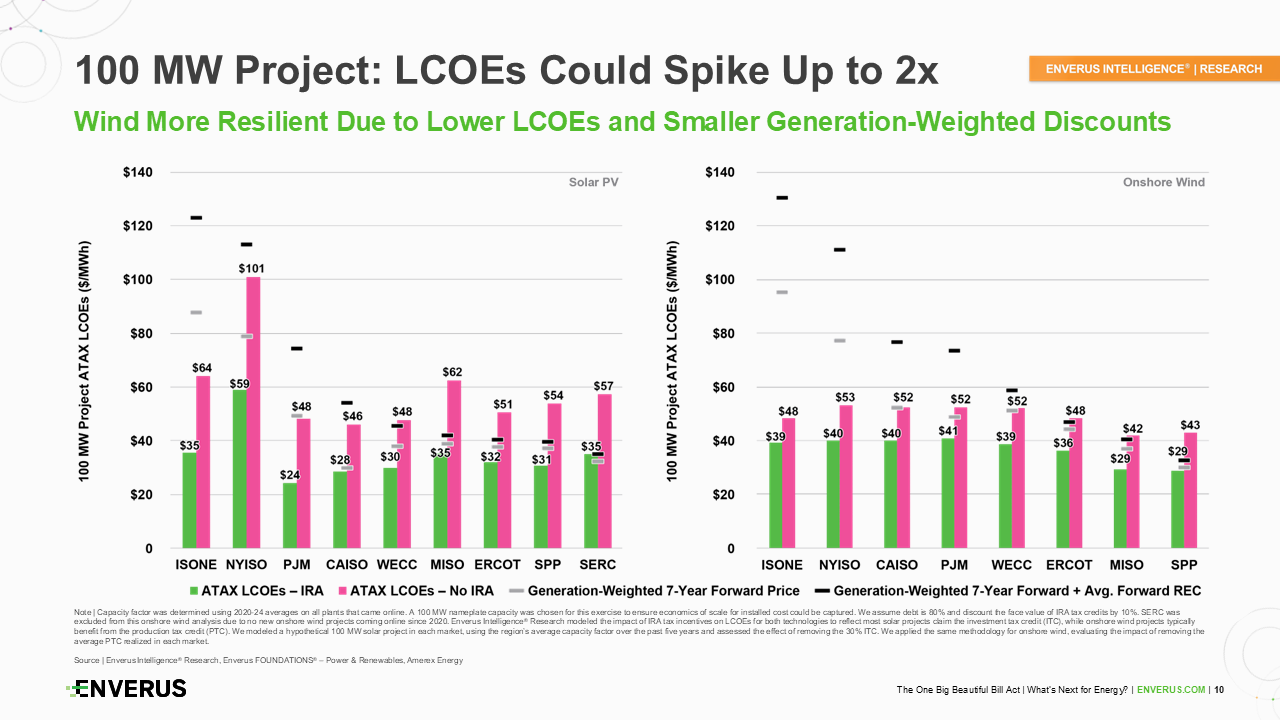

Analysis of queued renewable capacity across the Lower 48 states reveals that 85% of queued solar and 74% of queued onshore wind projects are sensitive to tax credit loss. However, this doesn’t spell the end for wind and solar development. Factors such as increasing load growth, supply chain constraints for new gas-fired plants, and resilient corporate offtake demand are expected to support continued renewable growth.

The impact of tax credit changes varies by market, with some regions showing greater resilience than others. For instance, ISO New England has less than 10% of queued solar and 2% of queued wind dependent on tax credits, while other markets show higher sensitivity. Project economics are influenced by factors such as generation-weighted prices, REC prices, and regional solar premiums or discounts. Despite the challenges, shifts to larger projects with economies of scale and rising REC prices driven by state RPS targets offer alternative paths to project viability.

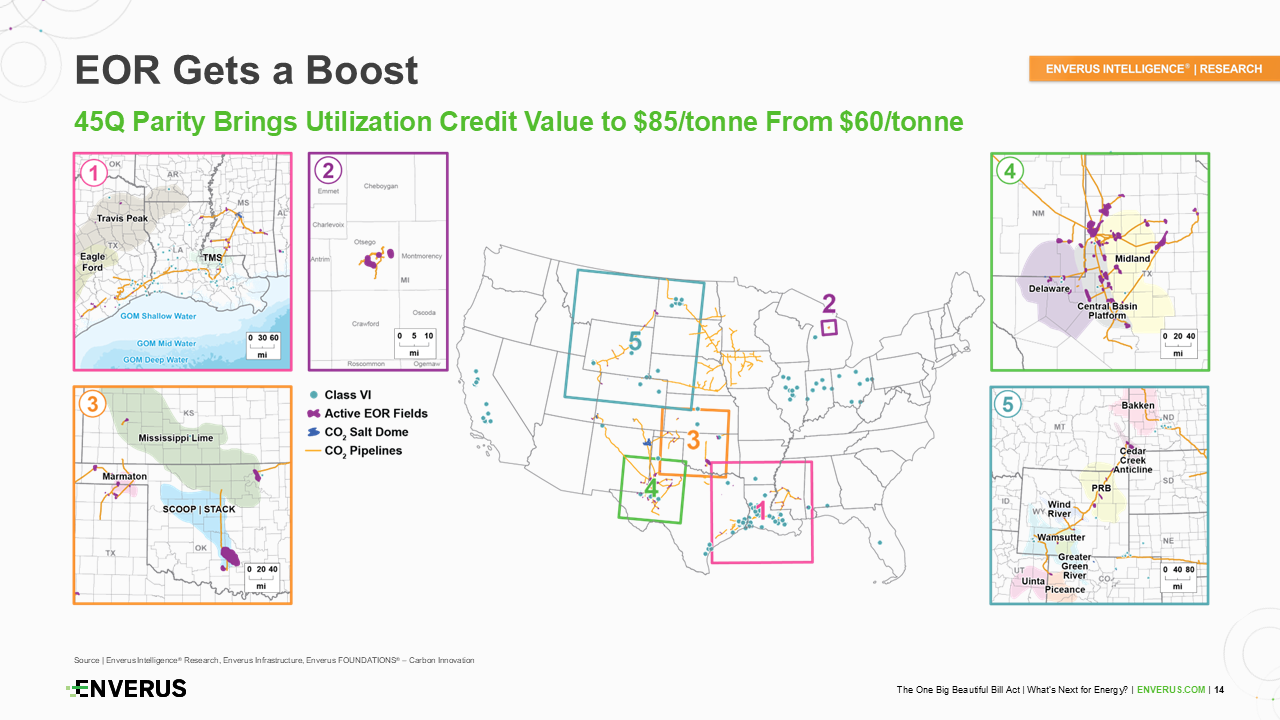

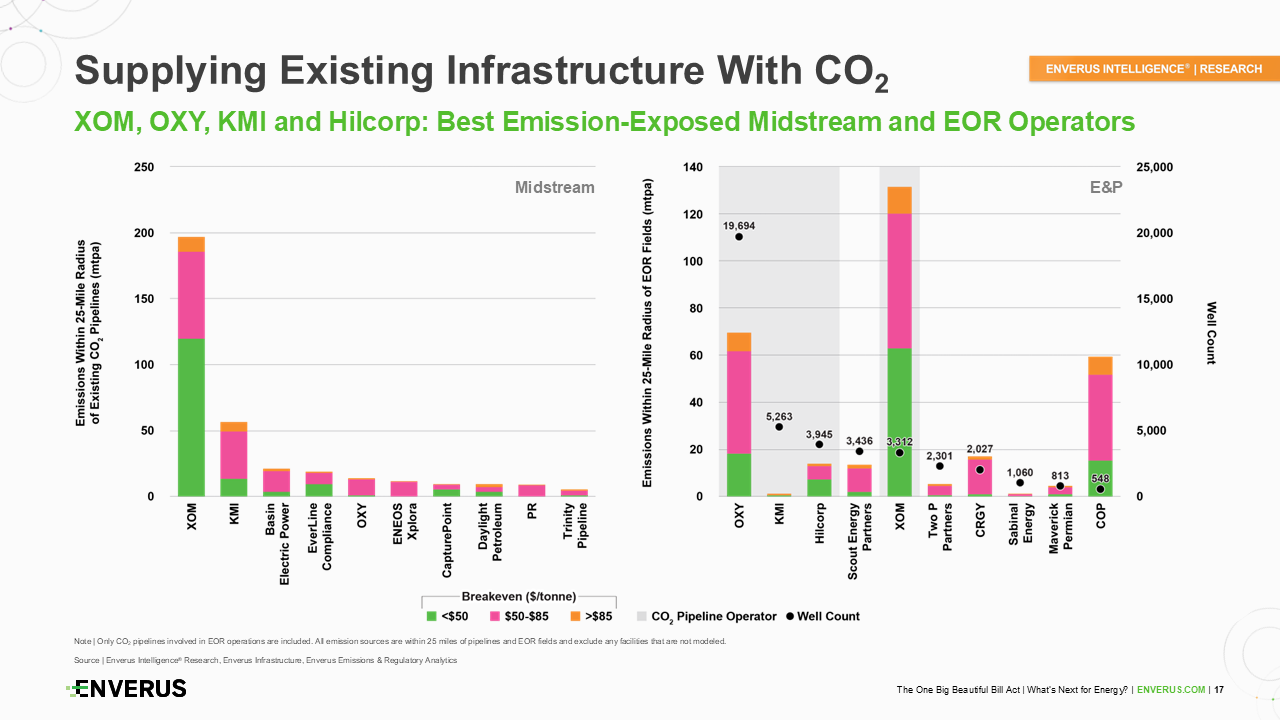

The OBBBA has given a significant boost to CCUS and EOR by providing parity in the 45Q tax credit. The utilization credit value has increased from $60 per ton to $85 per ton, matching the permanent sequestration credit. This change enhances the economic potential for anthropogenic CO2 capture in EOR operations across the Lower 48 states.

The increased credit value improves the economics of conventional EOR, potentially making it more favorable than remaining tier-one unconventional inventory in areas like the Permian Basin. This change could incentivize emitters, midstream companies and operators to explore EOR as a means of avoiding lengthy Class 6 well permitting timelines and recouping capital investments in carbon capture equipment more quickly. The parity in credit values also simplifies carbon accounting for projects utilizing both EOR and permanent sequestration.

The changes introduced by the OBBBA will have significant impacts on project economics across various energy sectors. For 100MW renewable projects, levelized cost of energy (LCOE) could potentially double without tax credit support. However, the impact varies by technology and location. For instance, wind projects in markets like ERCOT, MISO and SPP may still have LCOEs below wind-weighted forward prices plus REC prices, even without tax credits.

The domestic content strategy appears to be working, as illustrated by a case study of a utility-scale solar farm in CAISO. Projects using domestic equipment, while initially more costly, can achieve lower after-tax LCOEs compared to imported equipment scenarios due to the domestic content bonus adder. This demonstrates the effectiveness of the policy in encouraging domestic manufacturing while maintaining project viability.

Analysis of queued portfolio resiliency among the top 30 largest renewable owners reveals varying degrees of sensitivity to tax credit changes. Companies like Hexagon, Brookfield and CIP stand out with highly resilient portfolios, while others show more vulnerability. This variation in portfolio resilience will likely influence companies’ strategies moving forward, potentially driving shifts in project locations, technologies and development timelines.

In the CCUS and EOR space, companies are strategically positioned to take advantage of the new opportunities presented by the 45Q credit parity. Major players like Exxon, Occidental and Kinder Morgan have significant emissions within proximity to existing CO2 pipelines and EOR fields, potentially allowing them to quickly capitalize on these changes. However, the economics of carbon capture still vary widely, with some sources offering capture costs below $50 per ton while others fall in the $50-$85 per ton range.

The OBBBA’s changes will have far-reaching effects on the energy industry’s development trajectory. While some sectors face challenges, others see new opportunities. Clean transportation fuels see modest economic gains, excluding SAF, but these benefits are diluted by the long-term impact of LCFS credits and RINs. The green hydrogen industry faces significant challenges and must act quickly to secure credits, while blue hydrogen can still rely on the unchanged 45Q timelines.

Despite tax credit rollbacks, renewables are expected to remain a key part of the generation mix due to their rapid deployment capabilities and increasing demand driven by load growth. The CCS and EOR sectors receive a significant boost, providing new options for emitters and potentially improving EOR economics compared to declining unconventional inventory. As the industry adapts to these changes, ongoing analysis and forecasting will be crucial for understanding the long-term impacts on capacity expansion and overall energy mix evolution.

The OBBBA introduces transformative changes to U.S. energy policy, reshaping tax credit timelines and financial incentives for various sectors. While clean transportation fuels and CCUS see promising opportunities, challenges persist in areas like green hydrogen and residential renewables. Despite the reduced tax credit windows, the resilience of renewables and the strategic adaptability of industry leaders ensure continued progress in key markets. By navigating these shifts, stakeholders can position themselves to capitalize on new opportunities while mitigating risks in a rapidly evolving energy landscape.

Advanced grid insights with accurate load forecasts and extensive monitoring enhance trade execution and profitability.

Quickly identify grid opportunities and risks with high-quality mid-term forecasts, expert analysis and streamlined grid analysis.

Confidently shape your investment strategy, identify optimal power asset locations and optimize utility scale PV project profitability—all in minutes.

With Enverus Instant Analyst™, you receive answers you can trust, delivered in seconds. Sourcing from 25+ years of vetted data and research on the most trusted SaaS platform designed exclusively for energy.

Confidently shape your investment strategy, identify optimal power asset locations and optimize utility scale PV project profitability—all in minutes.

Arm yourself with the knowledge to inform strategic decisions and grow your business with one source for insights across oil and gas, renewables, carbon capture and ESG.

Design PV Plants & Battery Storage Systems 90% Faster with Our Advanced Solar & Battery Software.

SUGAR™ helps grid operators and utilities manage increasing interconnection queue volumes by accelerating modeling and simulation studies, with up to 2x reduction in time-consuming study processes.

Unlock returns of electron and molecule-based energy transition technologies with deal insights, from power generation assets to CCUS and hydrogen.

Tune out the noise, get unbiased evaluations and uncover hidden opportunities with advice you can trust from experienced energy and power intelligence advisors.

Comprehensive coverage of power markets and insights into emerging energy technologies and project economics.

Interconnect offers developers certainty throughout the interconnection lifecycle, providing scenario analysis and risk assessment capabilities to improve the chances of deploying new projects.

Let’s get started!

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Ready to Subscribe?

Ready to Get Started?

Ready to Subscribe?

Sign Up

Power Your Insights