Your free guide to navigating the North American and international energy landscape in 2025.

Select “Get Started” below if you would like to unlock Enverus Intelligence® Research’s (EIR) entire collection of in-depth reports, including the unredacted report on 2025 Energy Outlook and Trends, available exclusively for EIR members.

Enverus Intelligence® Research, Inc., a subsidiary of Enverus, provides the Enverus Intelligence® | Research (EIR) products. See additional disclosures.

As we head into 2025, the race for artificial intelligence (AI) dominance has escalated into a global security issue, with the incoming U.S. administration aiming to be both business friendly and a China hawk. Against this backdrop, the energy sector has never been more prominent, or dynamic.

The energy narrative in 2024 shifted from focusing on the urgency of the energy transition to the urgency of energy security. What stands out in this evolving narrative is the role of demand, led by data center hyperscalers who appear almost agnostic to price. For this group, the energy trilemma prioritizes reliability as No. 1, environmental concerns as No.2, cost as No. 3. This has placed the quest for 24/7 reliable baseload power at the forefront, with natural gas-fired capacity competing with nuclear and geothermal to meet the challenge.

Looking ahead to 2025, power demand growth fueled by the AI race will dominate the energy narrative. Readily available fuel options like natural gas will be essential to meeting the reliability aspects of this demand. While the long-standing North American gas thesis has centered on LNG, this year has introduced a second source of demand growth: the power market’s pivot toward gas to meet its reliability needs. We forecast relatively flat gas demand in the power sector out to 2030, which is bullish relative to the EIA’s forecast of a 9 Bcf/d decline. The intersection of power and gas will drive the North American energy narrative in 2025, with oil production taking a back seat. Power is not only influencing the gas sector but is permeating every aspect of the energy landscape.

Against this backdrop we see the following major themes for 2025:

U.S. Data Center Boom: LNG Export Growth & Regulatory Overhaul Will Reshape Global Energy Markets

Data Centers Will Lead U.S. Load Growth

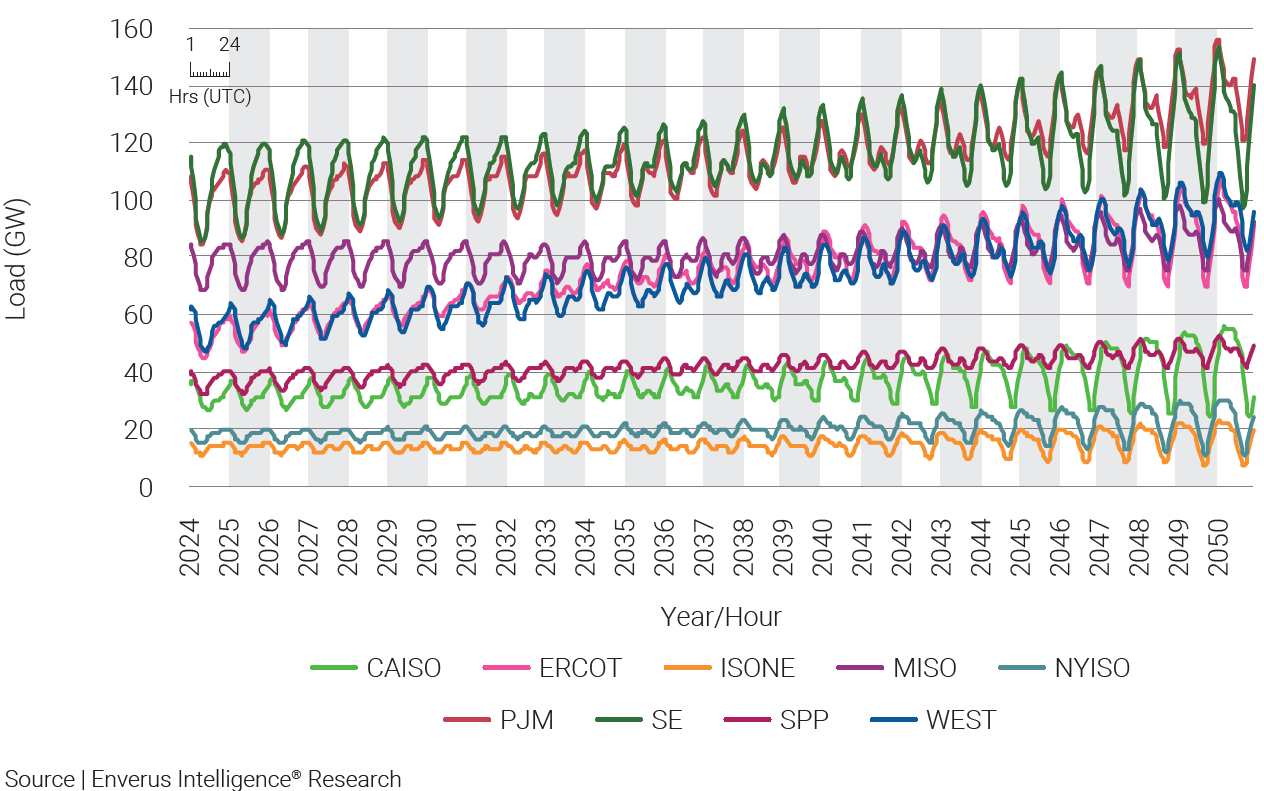

EIR forecasts U.S. load to increase 1.2% Y/Y and 38% by 2050, returning to growth after more than a decade of stagnation. Accelerated AI adoption and several energy transition and electrification themes foster expansion. Two of these levers — data centers and residential solar — impact the future in complex ways. Installed residential solar will rise from 45 GW to 56 GW in 2025 and 557 GW by 2050, vastly contributing to intraday volatility in load and offsetting load growth from all non-data center demand drivers. Data centers are the largest driver of load growth, with the highest requirement for reliability and most risk to the upside.

The contrast between these two significant factors will send ripples throughout the power ecosystem, fracturing the way we price different attributes of energy production. The early stages are visible today as power purchase agreements (PPAs), capacity markets and ancillary services all distort the once-clear nature of pool prices. We witnessed the first PPAs for baseload energy production this year; in 2025, those agreements will become increasingly commonplace. Capacity market prices exploded in the Eastern U.S.; next year those markets will develop in other regions and continue demanding high prices, supporting the economics of dispatchable generators.

Figure 1 | Lower 48 Annual Load Forecast

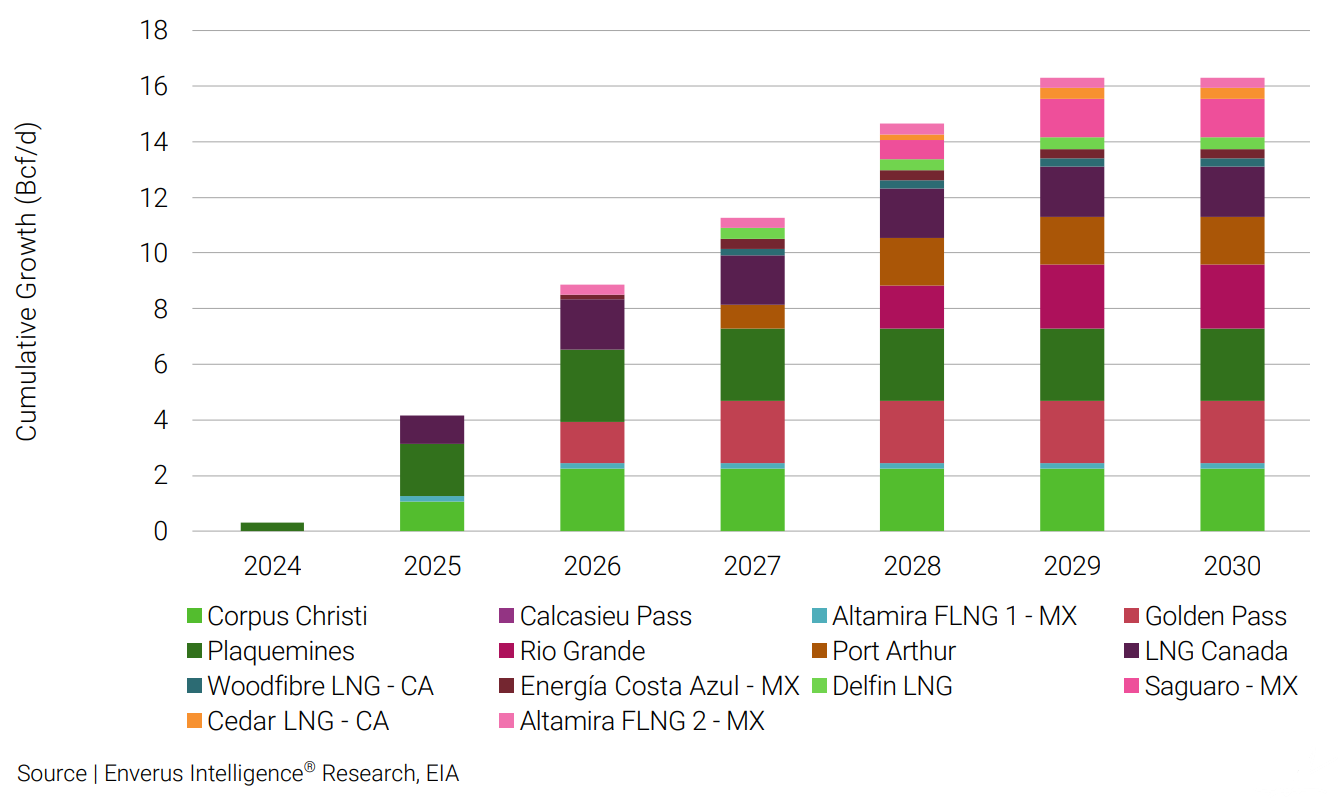

LNG Export Growth Will Push Henry Hub to $4.00/MMBTU

The next phase of growth in North American LNG exports will finally kick off in 2025 with the ramp of Plaquemines LNG (2.6 Bcf/d) and Corpus Christi Stage 3 (1.3 Bcf/d) in the U.S. and LNG Canada (1.8 Bcf/d) on Canada’s West Coast.

Enverus Intelligence® Research (EIR) forecasts NYMEX HH gas prices will rise to $4.00/MMBtu by 4Q25 and average $3.40 for the year. Given the pandemic-low drilling activity in the Haynesville and Appalachia through 2024, we expect activity will rise and production gains will be weighted to the latter part of 2025.

Figure 2 | North American LNG Cumulative Growth

Green Hydrogen, Geothermal Most at Risk for Tax Credit Elimination

EIR analyzed breakevens across nine technologies to assess the risk of Inflation Reduction Act (IRA) credit elimination, comparing them with and without IRA incentives against industry incumbents. These technologies represent $360 billion in planned capital expenditure between 2025-30, with 75% situated in Republican states — a potential boon for their durability.

Of the credits analyzed, the 45Q for blue hydrogen and EOR projects as well as the 45 PTC and 48 ITC for solar and onshore wind are least at risk, in our opinion. Without subsidies, these technologies cost 29%-63% more than incumbents, but with incentives, costs range from a 13% premium to a 35% discount. The tax credits enable them to compete with industry today, with the hope that further buildout will reduce costs and increase their unsubsidized competitiveness. In contrast, the 45V PTC for green hydrogen and 48 ITC for geothermal face higher risks, with unsubsidized breakeven premium ranges of 205%-310% dropping to 103%-135% when subsidized, highlighting their limited competitiveness. Landfill and manure RNG projects without credits outcompete the voluntary market, potentially making 45Z and 48 credits unnecessary.

Figure 3 | Breakeven Premiums vs. Incumbent Technology Benchmarks With and Without IRA Incentives

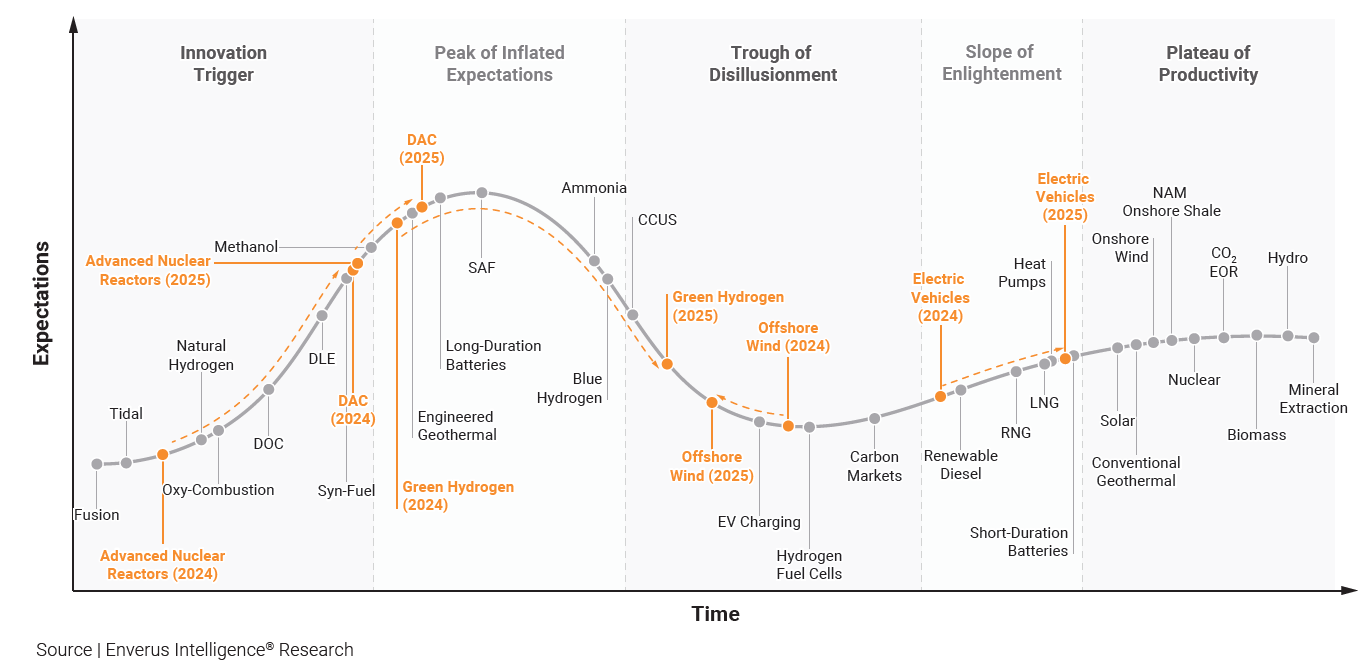

The "Chosen Few" Transition Technologies Build Momentum

2025 Will Be the Year of DAC, EVS and Advanced Nuclear Reactors

The ADVANCE Act of 2024 has boosted momentum for advanced nuclear technologies, especially small modular reactors. However, we recognize that these projects will require significant regulatory reforms to streamline the integration of nuclear technologies into the energy grid and address operational barriers.

DAC has gained momentum in 2024 with Climeworks’ Mammoth project becoming the world’s largest DAC facility at 36,000 tpa, soon to be surpassed by 1PointFive’s 500,000 tpa Stratos facility expected in mid-2025. DAC faces growing challenges associated with its energy-intensive nature, as highlighted by the withdrawal of Project Bison in Wyoming. Additionally, the future of the DOE’s Regional DAC Hubs program and any future funding for DAC is uncertain under the new administration. High capital costs and energy demands remain significant hurdles as DAC approaches the peak of inflated expectations.

Electric vehicle (EV) adoption in the U.S. is accelerating as improved infrastructure and diverse models make them more accessible. EV battery costs will fall below the $100/MWh cost parity milestone next year, meaning they will outcompete fossil fuel vehicles on affordability. Achieving cost parity is a clear signal that tax credits are no longer required to incentivize demand. Domestic manufacturing is also expected to grow, driven by content regulations, tariffs and reshoring efforts.

Figure 4 | Projected 2025 Energy Transition Technology Hype Curve

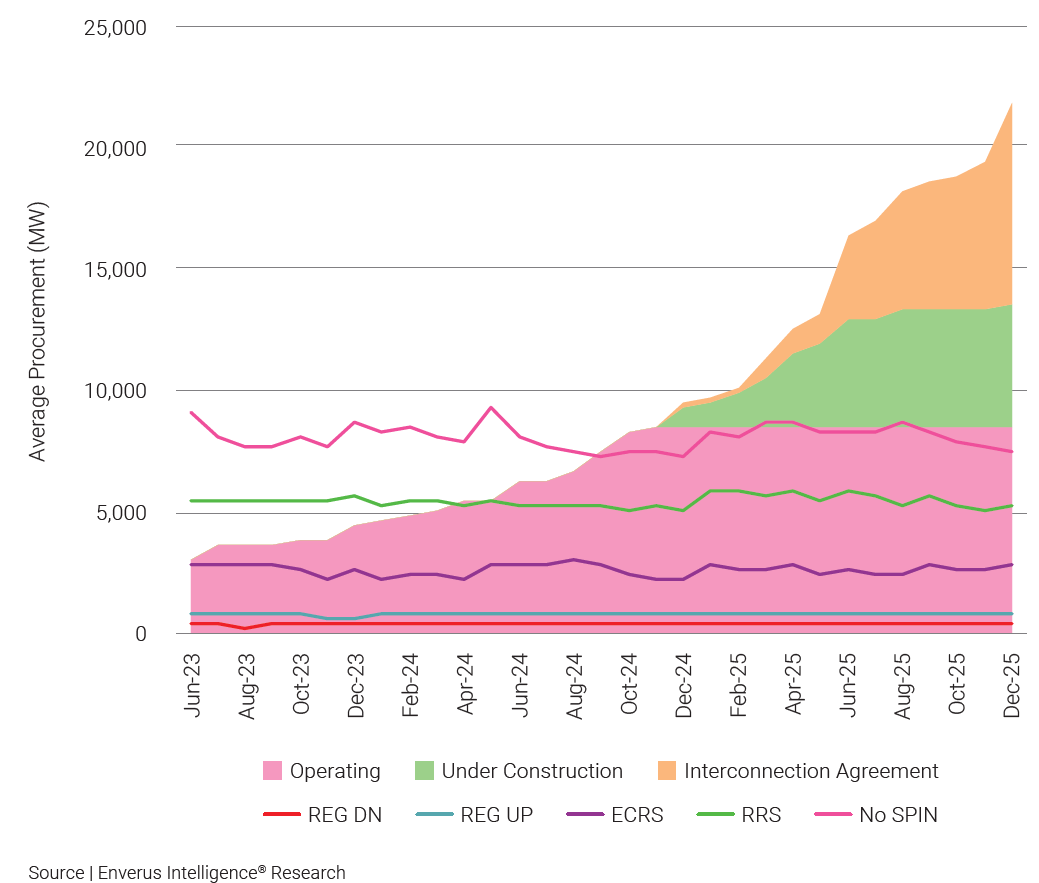

Battery Storage Will Increasingly Disrupt Power Markets

Markets with high battery storage adoption are set for a significant transformation in battery operations that will drive the need for ancillary market adjustments, reshaping revenue streams and grid dynamics. ERCOT’s market provides a glimpse of this evolution, with battery capacity surging 237% since early 2023. While battery revenues traditionally depended on ancillary services and energy arbitrage, growing storage saturation is changing the landscape.

As capacity outpaces ancillary market eligibility, operators will shift toward arbitrage-driven models, competing with dispatchable capacity such as natural gas-fired generation. Negative pricing hours will further enhance batteries’ competitiveness, allowing them to outbid natural gas plants and lowering bid prices. ERCOT currently has 8,374 MW of operating storage capacity, with 5,201 MW under construction and 8,244 MW with signed interconnection agreements set to come online by 2025 – a 160% increase over today’s already saturated levels. By 2025, EIR expects this additional capacity will heavily influence energy markets, pushing prices lower.

Figure 5 | Forecast of Ancillary Service Procurement and Storage Project Capacity

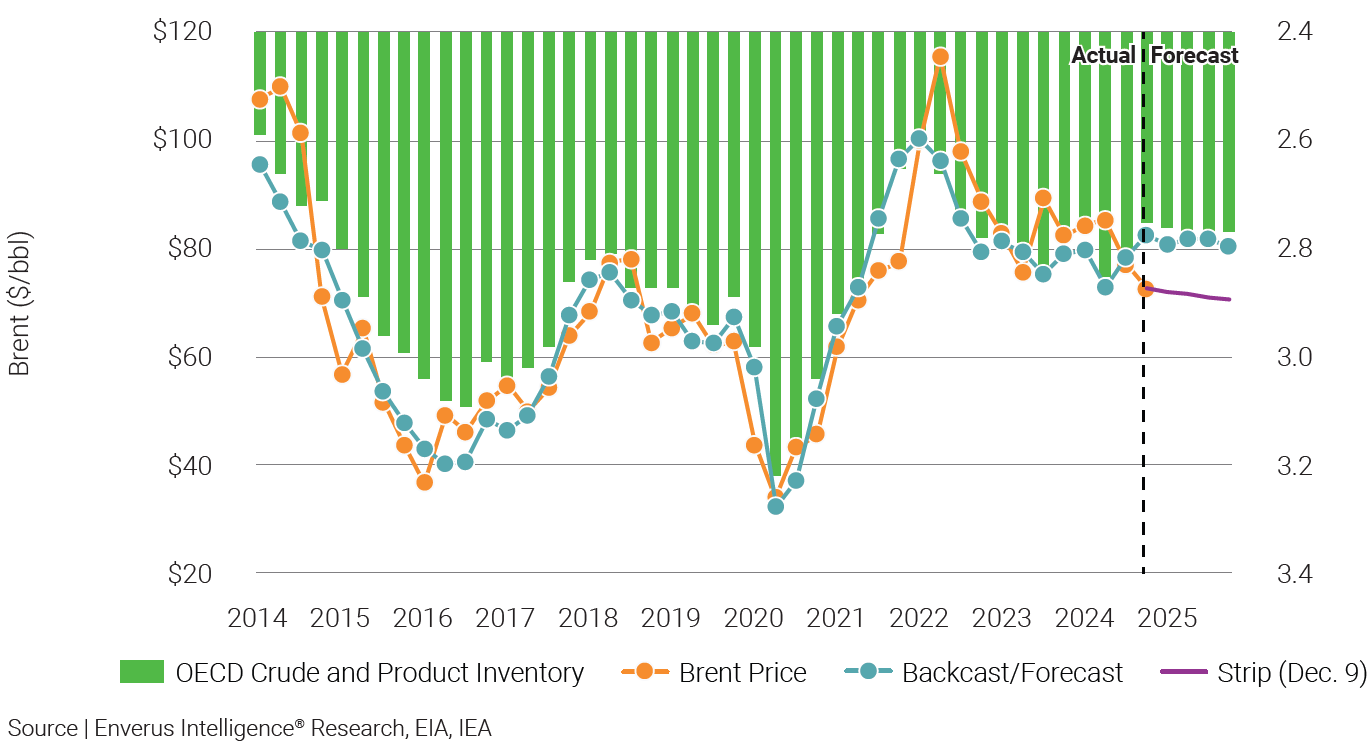

EIR forecasts 2025 Brent prices will average $80/bbl. Our outlook assumes OPEC+ will unwind cuts only if they do not pressure prices downward (favorable market conditions) and Chinese liquids demand will be flat Y/Y. We are conservative on global liquids demand growth (+0.7 MMbbl/d Y/Y), as an increasingly unstable trade environment further complicates Beijing’s task of stabilizing China’s economy.

Brent prices are currently in the low $70s, a level below fundamental fair value based on OECD crude and product stocks. Despite Brent prices’ knee-jerk reaction to geopolitical tensions, there is no sustained geopolitical premium embedded in current oil prices, especially considering the U.S. Strategic Petroleum Reserve is half empty.

Figure 6 | EIR's Brent Price Forecast

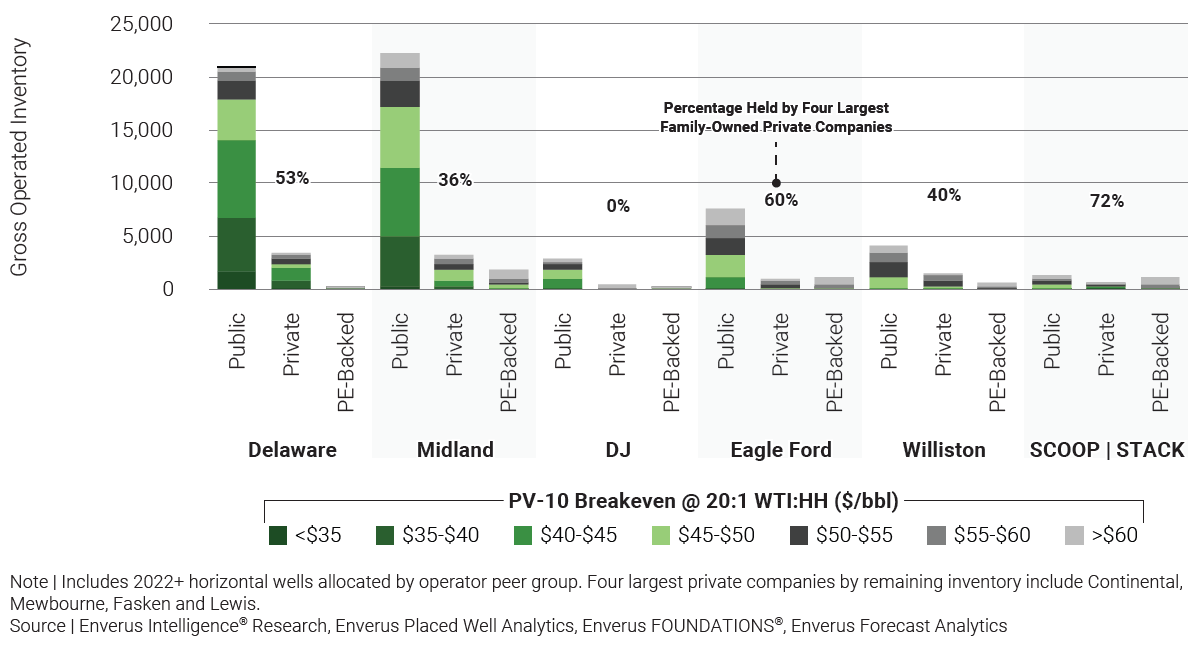

U.S. E&P Acquisitions Will Get Smaller, Less Economic

EIR expects average deal size to fall and breakevens of acquired inventory to rise in 2025 as $300 billion of upstream M&A during the last two years has consolidated the best available targets. The quality of acquired inventory has already declined, averaging a $50/bbl breakeven in 2024 versus $45/bbl in 2022-23. The pool of available remaining private equity assets is largely smaller, higher on the cost curve or both. Despite quality concerns, a need for scale and duration will motivate SMID-cap E&Ps to pursue these opportunities. Operational synergies like long laterals will be critical to improving economics on the available marginal acreage, with an estimated ~$5/bbl breakeven benefit to an incremental mile.

We expect public-to-public mergers will slow in 2025 from the recent average of five per year. While public companies hold nearly 90% of the remaining operated sub-$50/bbl breakeven inventory in oil-weighted major U.S. basins, ~85% of this inventory is held by operators with enterprise values exceeding $20 billion. These companies are not near-term motivated sellers for either corporate or asset deals. SMID-cap corporate deals offer suppressed valuations relative to private opportunities, but the lack of a strategic fit and agreement on go-forward management teams present headwinds.

Figure 7 | U.S. Oil-Weighted Inventory by Play and Peer Group

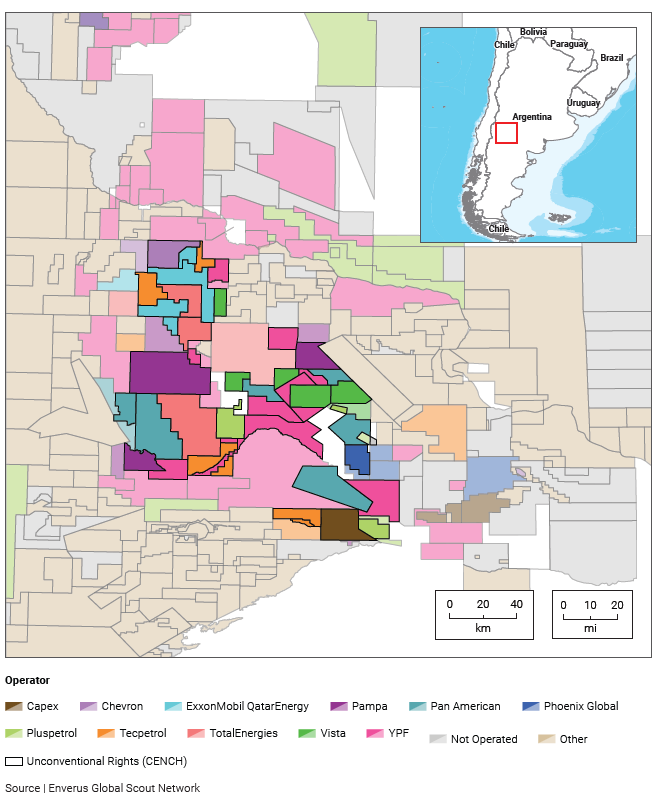

Argentina Shale Development Takes Center Stage

Argentine President Javier Milei’s ambitious agenda is bearing fruit. The Vaca Muerta will dominate Latin America in 2025 as one of the world’s top-ranked shale plays flexes its muscles. State-run YPF is likely to aggressively pursue monetization efforts, so expect lots of headlines. Perez Companc will return to E&P as an operator; Vista Energy will strike a path toward expansion; and Pluspetrol, with six of seven licenses divested by ExxonMobil and QatarEnergy, will hit the ground running. Newcomers will look for lower-cost entrances like the Palermo Aike.

Strengthening U.S.-Argentine relations may benefit the country’s campaign to boost midstream infrastructure, needed to ensure the South American country can become a net exporter by the close of the decade.

Figure 8 | Neuquén Basin Rights Holders

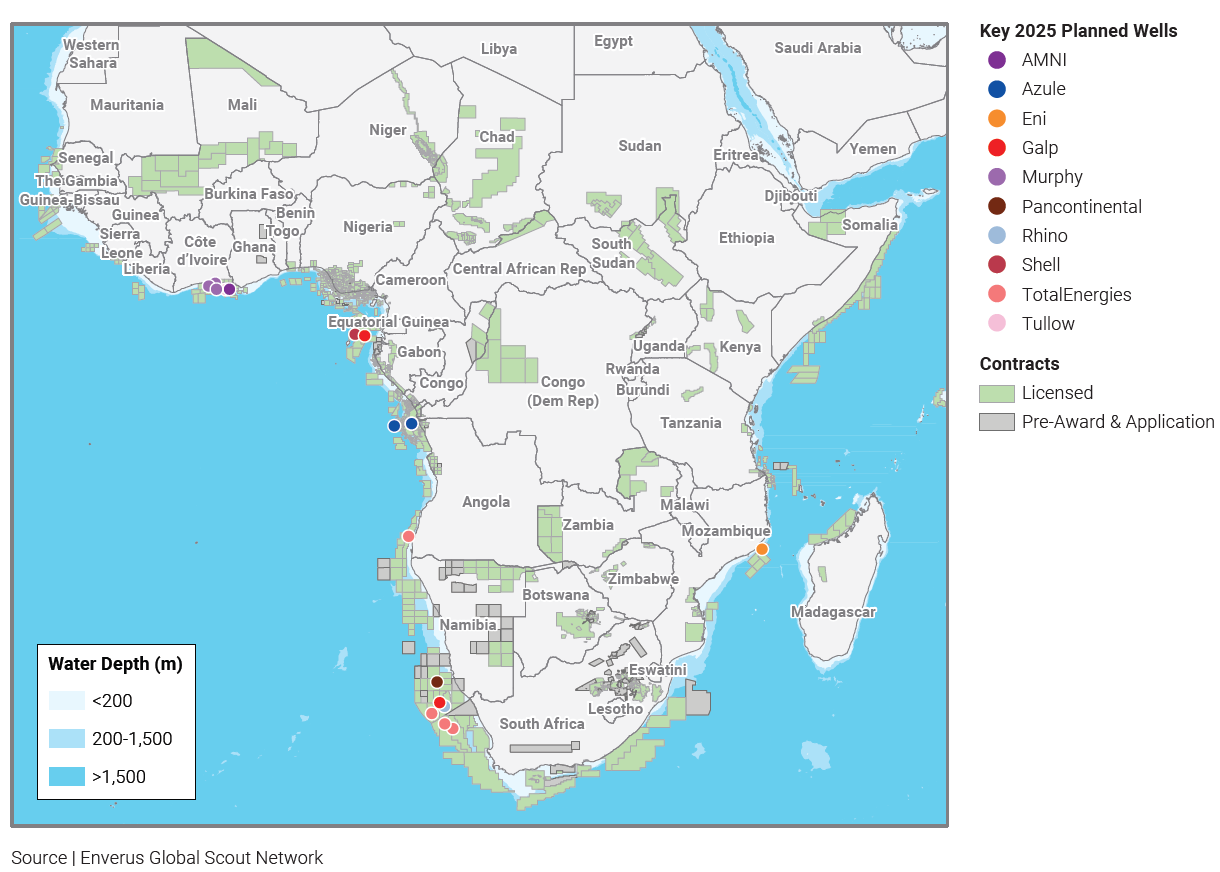

Orange and Ivory Will Remain in Vogue

Current Orange Basin explorers will be joined by Rhino and Chevron for wildcat drilling in Namibia. The sanctioning of the giant Mopane Complex and Venus development may occur in late 2025. Environmental pressures will continue obstructing exploration drilling in the basin’s South African portion.

Côte d’Ivoire will remain Africa’s second-most desirable exploration postal code. Eni will continue leading the E&P charge with Murphy planning exploration drilling and other majors acquiring acreage.

Figure 9 | West African Wildcats Will Continue Grabbing the Spotlight in 2025

Efficiency Gains Remain in Focus: Upstream Industry to Grind Away at Costs

U.S. Well Costs Will Stabilize as Tariffs Offset Efficiencies

After a ~10% decline in per-foot well costs in 2024, we forecast well costs will hold flat in 2025. We expect rigs and completion crews will continue making efficiency gains in 2025, placing downward pressure on overall equipment utilization. Lower-tier rigs and crews will be especially exposed to price reductions. Most activity, however, is weighted to public companies that prefer top-spec rigs and electric frac equipment. Steel prices had already bottomed and affected OCTG and tie-in costs even before the U.S. increased tariff risk from the presidential election. The 25% tariffs on steel in 2018 caused a 30% spike in the pipe PPI. Additional headwinds – like South Korea’s OCTG import allocation shrinking ~50,000 tons and potential penalties for Thailand import violations – reduce supply.

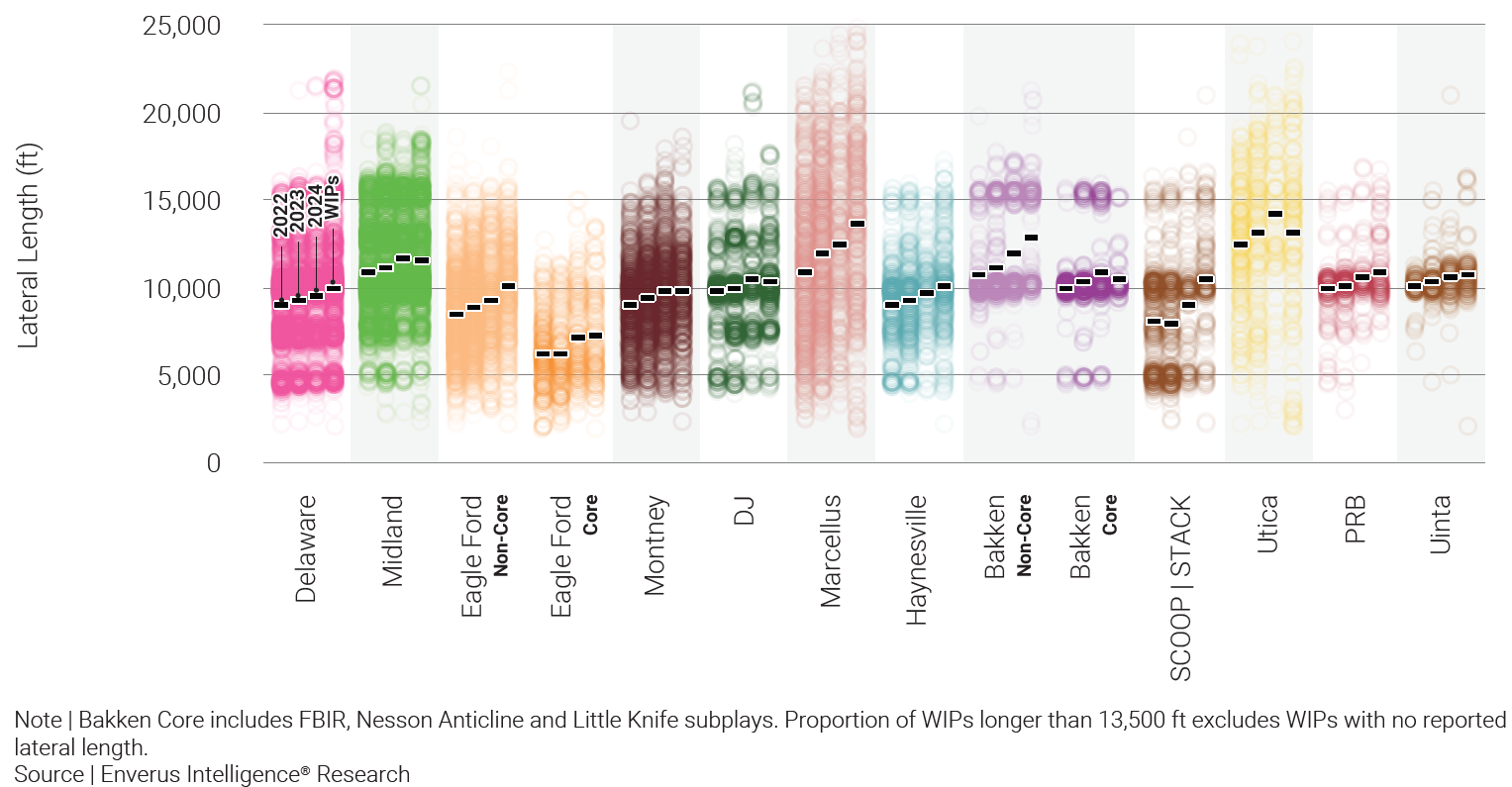

More 4-Mile Laterals Across North America

Long laterals driving down well costs have been a major catalyst for improving economics in 2024. We expect the trend will accelerate in 2025 with broader utilization of 3-mile laterals and a pivot to 4-mile wells by select operators.

Figure 10 | Lateral Length Trend by Play

Talk to an Expert to Unlock EIR’s In-Depth 2025 Outlook Reports

Talk to an Expert to Unlock EIR’s In-depth 2025 Outlook Reports

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Let’s get started!

We’ll follow up right away to show you a quick product tour.