[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories increased by 5.7 MMBbl last week, according to the weekly EIA report. Gasoline inventories decreased 3.0 MMBbl while distillate inventories decreased 1.0 MMBbl. Total petroleum inventories posted a decrease of 2.2 MMBbl. US crude oil production was unchanged from the previous week, per EIA, while crude oil imports were up 0.84 MMBbl/d to an average of 6.7 MMBbl/d.

- WTI prices spent most of the week giving back the gains made from the previous week that were based on the upcoming OPEC+ meeting in December that may add more production cuts and may result in the Chinese increasing oil import quotas. There are conflicting reports on whether Russia will be interested in participating in additional production cuts, and lingering concerns regarding global economic growth seemed to fuel the selling until Friday. Good economic news from the Labor Department on the US economy, surprising positive manufacturing data released from China, and supportive news on the upcoming signing of the initial phase of the trade deal between the US and China sent both the US equities market and the crude market up on the bullish economic outlook. By the end of the day, crude had regained most of the losses from earlier in the week and closed the week just below the previous week.

- Regardless of the spot price action during the week, the spot contract is holding a significant premium to the 2020 strip. While the January contract continues a slight premium to December, the rest of the year represents discounts, as the trade remains concerned about global economic demand and the potential for a supply glut during 2020.

- The CFTC report released Friday (showing positions from October 29) showed little change in the expectations of price direction by the speculative sector. The Managed Money long sector reduced positions by 2,706 contracts, while the Managed Money short sector reduced positions by 14,307 contracts. The current speculative sector is noncommittal to the crude oil trade.

- Market internals last week also confirmed a nondirectional neutral bias, with prices closing just $0.46 below the previous week’s high close on higher volume and slightly lower open interest (according to preliminary reporting from the CME).

- Prices continued in the recent mini-range of $53-$57, waiting for the development of a trend for near-term prices. Bullish news will take prices upward toward the commonly traded 200-day moving average ($57.15 today), and a breakout above that level on a daily closing basis will send prices toward the highs from September between $58.49 and $59.39. Bearish input from the declining rig count and concerns about the global economy could bring another test at the low end of the range, at $53, which will likely find buyers.

NATURAL GAS

- Natural gas dry production decreased 0.93 Bcf/d last week, largely due to weather issues in the Rockies, while Canadian imports increased 0.12 Bcf/d.

- Res/Com demand increased 6.47 Bcf/d, while power demand decreased 5.83 Bcf/d and industrial demand increased by 0.93 Bcf/d. Secondary components had LNG exports gaining 0.26 Bcf/d, while Mexican exports decreased 0.07 Bcf/d on the week.

- These events left the totals for the week showing the market dropping 0.81 Bcf/d in supply while demand increased by 2.34 Bcf/d.

- The storage report last week showed the injections for the previous week at 89 Bcf. Total inventories are now 559 Bcf higher than last year and 52 Bcf above the five-year average. The current near-term (coming week) weather forecasts from NOAA show below-average temperatures from the Rockies to the East Coast (including the TX area), while there are above-average temperatures in the West. The 8-to-14-day forecast continues the pattern.

- The CFTC report released last week (dated October 29) showed initial stages of a short covering process by the Managed Money short position, as they reduced positions by 21,951 contracts, while Managed Money long positions increased by 12,085 contracts. This short covering is due to the weather forecasts bringing higher Res/Com demand in the coming two weeks.

- The market internals now have a neutral to positive bias, as the market gained during the course of the week on large weekly volume gains, but with a reduction in total open interest (according to preliminary data from the CME). The falloff in total open interest is the result of the contract expiration and the continued short covering. Rallies based solely on short covering are historically short in duration. If the market is to maintain a longer-term bullish bias into the winter season, it will need to be based on gains in total open interest, offsetting the short covering losses.

- The market blew through several areas of resistance last week and now seems poised to continue gains above the September high of $2.71 (on daily close), which will catch additional short covering by the speculative sector. Expect additional volatility this week with short covering, depending on how the weather forecasts play out. Momentum indicators are becoming overbought, but that will not dramatically affect short covering. Additional gains may take prices to the February and March highs between $2.824 and $2.908. A reversal in the forecasts and adjustments to demand will pressure prices down to a key area around $2.50.

NATURAL GAS LIQUIDS

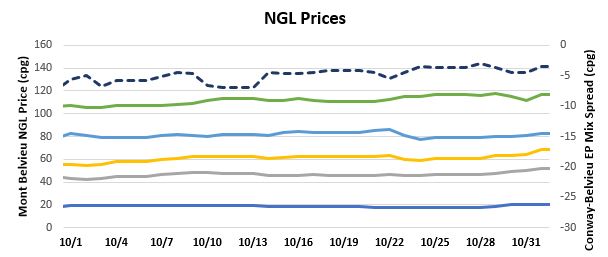

- Purity product prices were mostly up week-over-week, with the exception of isobutane. Ethane was up $0.014 to $0.193, propane was up $0.033 to $0.493, normal butane was up $0.031 to $0.641, and natural gasoline was up $0.014 to $1.155. Isobutane dropped $0.011 to $0.806.

- US propane stocks fell ~137 MBbl for the week ending October 25. Stocks now sit at 99.85 MMBbl, roughly 16.83 MMBbl and 21.50 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

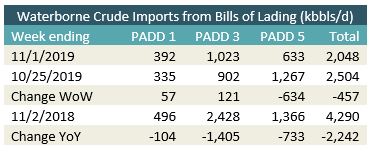

- US waterborne imports of crude oil fell for the week ending November 1, 2019, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of November 4, aggregated data from customs manifests suggests that overall waterborne imports decreased by more than 450 MBbl/d from the previous week. The decline was driven by lower imports into PADD 5, which fell by more than 630 MBbl/d from the prior week. PADD 1 rose slightly, up by more than 50 MBbl/d, and PADD 3 increased by more than 120 MBbl/d.

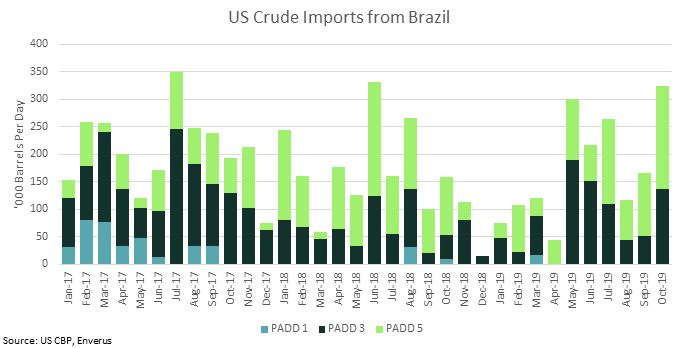

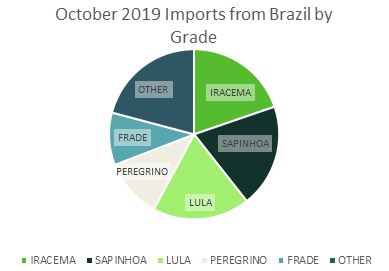

- October’s imports of Brazilian crude oil reached the highest level since June 2018, with the biggest driver being PADD 5 imports. The grade with the highest share of imports was Iracema, with Sapinhoa second and Lula third. The biggest importers of Brazilian crude were Marathon Carson and Chevron El Segundo.