[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories increased by 2.2 MMBbl last week, according to the weekly EIA report. Gasoline inventories increased 1.9 MMBbl while distillate inventories decreased 2.5 MMBbl. Total petroleum inventories posted a decrease of 5.9 MMBbl. US crude oil production increased 200 MBbl/d from the previous week, per EIA, while crude oil imports were down 0.37 MMBbl/d to an average of 5.8 MMBbl/d.

- WTI prices extended the recent range that has held the market for the last few weeks, closing near the highs for the week. Some of the optimism was generated from comments from Fed Chairman Jerome Powell outlining a healthy US job market and projections for continued economic expansion. The news on Friday regarding the potential for the Phase 1 trade agreement getting close to finalization also provided optimism in the crude and equity markets. These comments on the trade agreement are subject to some skepticism, as the market was aware of a similar expectation last May, only to have that agreement blow up.

- Optimism is supported by the ongoing declining rig counts as US E&P companies are shifting drilling to the most economic and efficient areas, confirming the third quarter earnings calls that pointed toward lower capex plans in the coming year.

- The IEA World Energy Outlook release last week showed little adjustment to demand growth expectations in 2019 and 2020, keeping the previous growth in 2019 at 1.0 MMBbl/d and 1.2 MMBbl/d in 2020. Non-OPEC output growth expectations increased from 1.8 MMBbl/d to 2.3 MMBbl/d in 2020.

- Doubts have started to develop on the upcoming OPEC meeting and whether there are commitments for deeper production cuts in 2020. These doubts have been tempered by the expectation of lower production from US E&P companies.

- The CFTC report released Friday (showing positions from November 12) showed a shift from expecting lower prices by the speculative trade, with the Managed Money long sector decreasing positions by 9,922 contracts and the Managed Money short positions reducing positions significantly by covering 43,239 contracts. This shift shows that during this extended period of range trading, concerns about global demand are starting to recede in the speculative sector.

- Market internals last week continued to be neutral with a distinctly bullish bias — with prices closing up, near the highs of the week — with higher volume and gains in open interest as prices extended the recent range between $53-$57 (now nearing $58.00). Prices closed the week above the commonly traded 200-day moving average ($57.33 on Friday), leading to continuation of the short covering trade. The rally at the end of the week, along with the close above the moving average, may lead to additional advances this week. Rallies will challenge the highs from September between $58.49-$59.39. Bearish input from a potential breakdown of the US-China trade deal could bring another test at the low end of the range at $55 this week, which will likely find buyers.

NATURAL GAS

- Natural gas dry production increased 0.21 Bcf/d last week. With the colder weather and increased demand, Canadian imports increased by 0.56 Bcf/d.

- Res/Com demand increased 9.17 Bcf/d due to the colder-than-normal weather, while power and industrial demand increased 0.86 Bcf/d and 1.06 Bcf/d, respectively. LNG exports gained 0.19 Bcf/d, while Mexican exports increased by 0.16 Bcf/d on the week.

- These events left the totals for the week showing the market gaining 0.77 Bcf/d in total supply, while total demand increased 11.79 Bcf/d.

- The storage report last week showed the injections for the previous week at 3 Bcf. Total inventories are now 491 Bcf higher than last year and 2 Bcf above the five-year average. Current weather forecasts from NOAA have below-average temperatures from the Southwest up the Mississippi Valley to the Northeast region in the near term, while the 8-to-14-day forecast shows a warming pattern, limiting below-average temperatures to the Rocky Mountains and South Central US. The highly populated Northeast is forecast to be near normal.

- The CFTC report released last week (dated November 12) gave a peculiar reading on expectations of future movements, as the Managed Money short position, benefiting from the “island top” (bearish), covered 24,604 contracts as prices declined to $2.62. The Managed Money long position sold 14,044 contracts.

- The market internals confirmed a neutral to negative bias, as prices rallied to test the island top three different times and on Friday managed to pierce the gap by nearly a penny, but failed to close the gap. Volume was lower than the previous week but still above the recent week’s average. Open interest gained week over week.

- The action last week, trying three times to attack the gap from the Monday open, has reinforced that area of resistance to future gains in prices. That gap (now at $2.724 to $2.755) will continue to provide selling opportunities in the coming week. Should the forecasts continue to moderate, expect the support from last week at $2.570 down to $2.52 to find buyers.

NATURAL GAS LIQUIDS

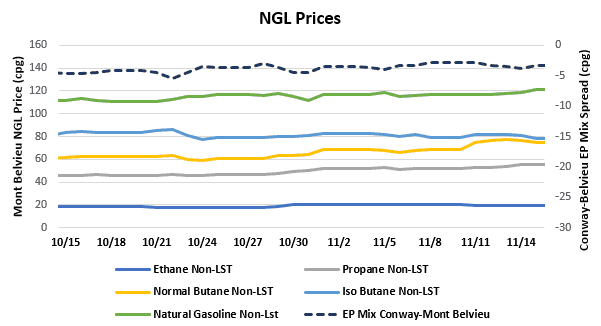

- NGL prices were mostly up week-over-week. Propane gained $0.022 to $0.538, normal butane up $0.081 to $0.760, and natural gasoline up $0.015 to $1.182. Ethane was down $0.010 to $0.193, and isobutane fell $0.005 to $0.808.

- Propane and normal butane prices have climbed over the last month. Since October 17, propane and butane have gained 8.5 cpg and 11.9 cpg, respectively. Normal butane prices have increased due to seasonal gasoline blending requiring more butane to meet higher RVP specs as well as increased export demand. Propane is being supported mainly by seasonal demand from residential heating.

- US propane stocks dropped ~2.52 MMBbl for the week ending November 8, as cooler weather hit the US. Stocks now sit at 97.65 MMBbl, roughly 13.89 MMBbl and 22.97 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

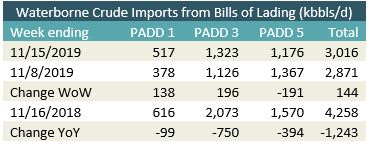

- US waterborne imports of crude oil rose for the week ending November 15, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of November 18, aggregated data from customs manifests suggested that overall waterborne imports increased by nearly 150 MBbls/d from the previous week. The increase was driven by higher imports into PADDs 1 & 3, which were up by 138 MBbls/d and 196 MBbls/d, respectively. PADD 5 waterborne imports declined, down by 191 MBbls/d.

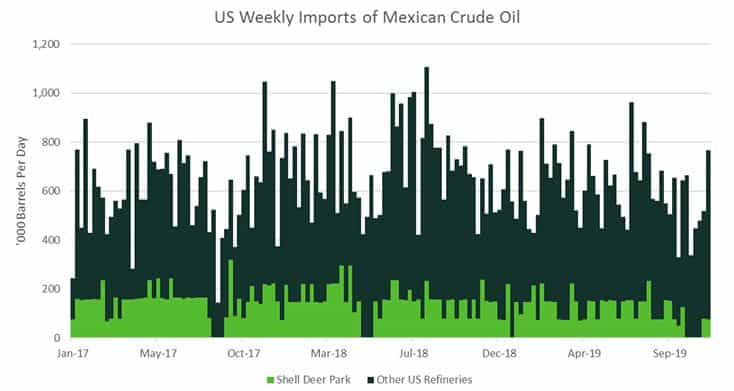

- US crude imports from Mexico for the week are at their highest level since early August. The decrease we observed was partially attributable to a drop in imports at the Shell Deer Park refinery, which is a joint venture between Mexican National Oil Company Pemex and Shell. Reuters reported that the refinery shut down a crude distillation unit on September 23. Enverus’s data shows that starting the week of October 11, the refinery did not receive any Mexican crude oil. Reuters reported the crude unit restarted on November 12. Enverus’s vessel tracking data shows a nearly 1-month gap in crude tanker arrivals to the Deer Park refinery, with the Paramount Hanover arriving from Mexican loading terminal Dos Bocas on October 3 and leaving on October 5. The next crude tanker to arrive was the Paramount Hamilton, which arrived on November 1.