[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories increased by 1.6 MMBbl last week, according to the weekly EIA report. Gasoline and distillate inventories increased 5.1 MMBbl and 0.7 MMBbl, respectively. Total petroleum inventories posted a slight increase of 0.1 MMBbl. US crude oil production rose 100 MBbl/d, per EIA, while crude oil imports were up 0.22 MMBbl/d to an average of 6.2 MMBbl/d.

- WTI prices started the week firm and remained at the high end of the recent range, around $58. The trade seemed to be waiting for additional news regarding China-US trade negotiations. Positive news that China’s top negotiator (Liu He) had phone conversations with Treasury Secretary Steven Mnuchin and Trade Representative Lighthizer brought optimism regarding the negotiations. The Chinese commerce ministry was quoted as saying, “Both sides discussed resolving core issues of common concern.” These developments were dealt a possible blow by the news of Trump signing into law a bill backing the Hong Kong protestors. This will likely pressure the parties trying to push the phase 1 deal.

- As the week progressed, trade received some bearish news as the OPEC+ meeting, coming later this week, changed the expectation of deeper cuts by the groups to one of just extending the existing agreement. Saudi Arabia indicated to other OPEC members that it will no longer facilitate the excessive production by others. Adding to this news was the Russian oil minister’s suggestion of postponing the new supply caps until April.

- The CFTC report was not released on Friday due to the holiday. The precipitous decline in prices on Friday was likely stemmed from renewed trade war concerns following President Trump’s signing of the Hong Kong Human Rights and Democracy Act supporting Hong Kong protesters.

- Market internals last week developed a neutral to bearish bias going into this week. The high at $58.68 was met with selling last week, and the selling accelerated during the Friday trade day. The declines held the lows of the recent range at $55.00. A nearly $3.00 drop on Friday is a bearish indicator long term for the week, but it also will provide a counter bounce during the week. The inability of the market to extend the gains or losses beyond this range ($54-$59) suggests that trade will need a significant event or news to drive the speculative trade to shift positions.

- Similar to last week, rallies will challenge the highs from September of between $58.49 and $59.39. Should there be additional news of the tariff stalemate continuing this week, it is likely prices will bring another test at the low end of the range, at $55.

NATURAL GAS

- Natural gas dry production increased 1.11 Bcf/d last week with the South Central accounting for most of the gains (+0.90 Bcf/d), while Canadian imports decreased by 0.75 Bcf/d.

- Demand showed the Res/Com market sector increasing 0.77 Bcf/d, while Power demand decreased 2.71 Bcf/d and Industrial demand increased by 0.07 Bcf/d. LNG exports decreased 0.27 Bcf/d on the week, while Mexican exports decreased 0.08 Bcf/d.

- These events left the totals for the week with the market increasing 0.36 Bcf/d in total supply, while total demand decreased 2.21 Bcf/d.

- The storage report last week showed a withdrawal of 28 Bcf. Total inventories are now 548 Bcf higher than last year and 31 Bcf below the five-year average. The current weather forecasts from NOAA, in the near term (coming week), show normal to above-average temperatures throughout the US. The 8- to 14-day forecast is similar to the short-term forecast, showing normal to above-average temperatures throughout the US.

- The CFTC report was not released last week due to the holiday. With prices falling during the week and significant gains in total open interest, expect a gain in the Managed Money short position when the data is released today.

- The market internals developed a more bearish bias as prices failed on the rally and declined below the support zone around $2.50. These events occurred with strong gains in total open interest, but volume was below that of the previous week due to the holiday.

- Prices have defined the area at the island gap ($2.724) as major long-term resistance and will continue to find sellers on any challenges. The January contract held support at $2.50 for a brief period, but with the expiration of the December contract below the key area, it was only a matter of time before the January contract broke down below the December contract. With this breakdown last week, the lows established in October, around $2.20, will be targeted by the bears.

NATURAL GAS LIQUIDS

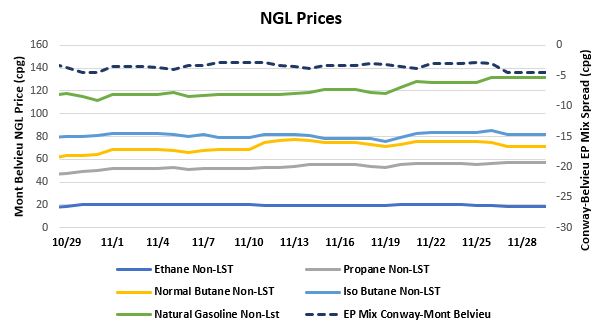

- Purity product prices were both up and down last week. Ethane was down 4.6% to average $0.189/gal for the week, while normal butane was down 0.8% to average $0.729/gal. Propane gained 3.7% to average $0.567/gal, isobutane gained 3.6% to average $0.827/gal, and natural gasoline increased by 6.7% to average $1.313/gal.

- Propane continues to be supported during the winter heating season, but is also being supported by international demand. Natural gasoline prices did see an uptick, but we suspect this was due to short covering and low trading volume around the Thanksgiving holiday. Butane prices didn’t see too much price action on a weekly average, although the fire at TPC Port Neches took down a butadiene unit, causing prices to decline on a daily basis.

- The EIA reported a draw in propane/propylene stocks of ~0.68 MMBbl last week. Stocks now stand at 93.5 MMBbl, which is roughly 12.38 MMBbl higher than the same week in 2018 and 20.37 MMBbl higher than the same week in 2017.

SHIPPING

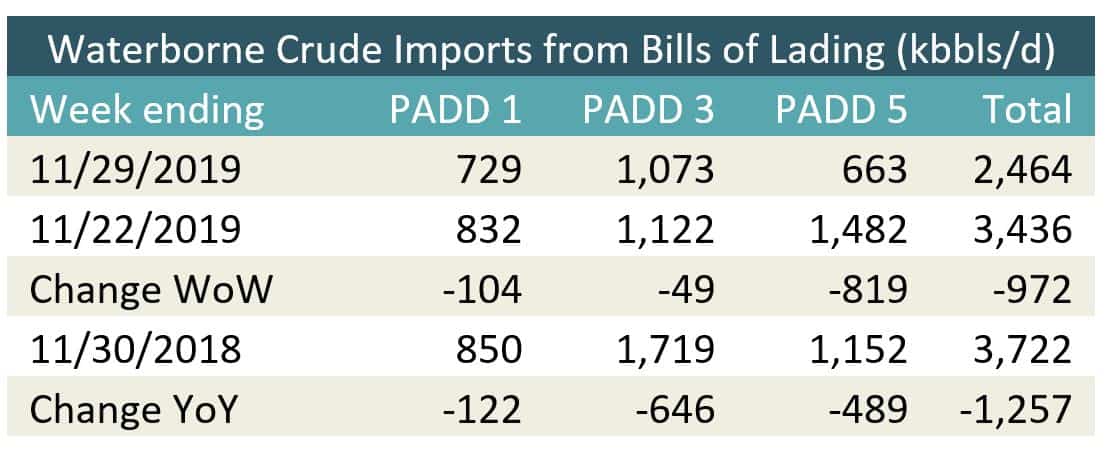

- US waterborne imports of crude oil fell for the week ending November 29, 2019, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of December 2, aggregated data from customs manifests suggested that overall waterborne imports decreased by nearly 1 MMBbl/d from the previous week. The decrease was driven by lower imports across the board, with the largest decrease happening in PADD 5, which fell by nearly 820 MBbl/d. PADD 1 imports dropped by 622 MBbl/d and PADD 3 imports fell by nearly 50 MBbl/d. At 1.946 MMBbl/d, waterborne imports based on bills of lading are at their lowest weekly level since at least 2017.

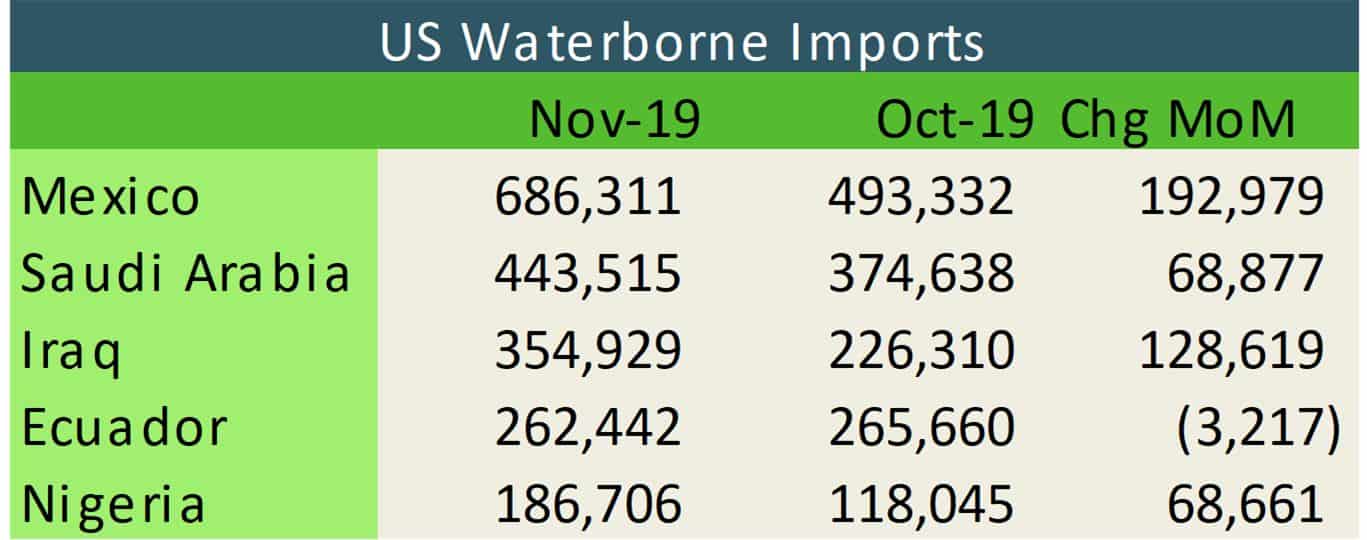

- With November now complete, total waterborne imports of crude oil per analysis were 2.89 MMBbl/d for the month, higher than October’s level of 2.68 MMBbl/d but the second lowest since at least 2017. See below for the top sources of daily barrels of crude in November.