[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories posted an increase of 2.4 MMBbl last week, according to the weekly EIA report. Gasoline inventories increased 4.4 MMBbl, while distillate inventories increased 1.5 MMBbl. With all these increases, total petroleum inventories posted a large build of 10.4 MMBbl. US crude oil production increased 100 MBbl/d, while crude oil imports were up 0.49 MMBbl/d to an average of 7.1 MMBbl/d.

- Prices were down all week as the market continued to struggle with the tariff and trade issues between the US and China. The prior week, the Trump administration’s announcement of an additional 10% tariff on $300 billion of Chinese goods, effective September 1, added more skepticism of any agreement between the world’s largest economies. WTI then had to absorb the trade news of China devaluing its currency (the yuan) to nearly a 10-year low. Adding to the WTI trade woes was the China announcement to state-run companies to halt the imports of US agricultural products. In response to these events, the US promptly branded China a currency manipulator.

- If that bearish news weren’t enough, the inventory release on Wednesday added fuel to the collapse. The large gains in total petroleum inventories forced selling that took prices to the lows of the week, just above that critical area of support around $50 that had held the market twice in early June.

- The only reprieve the market got from the bullish side was at the end of the week when Saudi Arabia announced it was going to be contacting other OPEC participants to develop a plan to offset the decrease in global demand growth. This news brought prices back above $54, but with no plans announced yet, it is unlikely to support additional gains, with global economic issues exerting pressure on prices. The only other bullish issue for the market to consider is the Iranian meddling in the Strait of Hormuz, which was dormant last week.

- The CFTC report released Friday (dated August 6) provides little new information, as the report date was before the inventory release and the positions had not shifted in any dramatic form. The Managed Money long sector (speculating on higher prices) added 5,124 contracts. The Managed Money short positions increased by 7,095 contracts.

- Market internals shifted to a negative bias with the declines to $50 as volume gained (Wednesday was the highest daily volume since May 29) week over week and open interest declined, suggesting that a large portion of the losses associated with the inventory release were speculative longs aborting positions. This week’s CFTC report will likely confirm the exodus.

- Even with the substantial fall of WTI prices in the past couple of weeks, the market continues to trade in a range between $50 and $61. Depending on the outcome of the Saudi talks with other OPEC nations, and without additional substantive aggression by Iran forcing a conflict, it is unlikely that prices will garner the support to trade up to the April highs of $66.60. Should China cease buying oil from the US in retaliation for the tariffs and reinitiate buying oil from Iran, the global market could be flooded going into an already oversupplied 2020. This event would pressure prices below the key $50 area, possibly taking prices down to December ’18 levels of around $47 and the same month’s lows of $42.36.

NATURAL GAS

- Natural gas dry production showed an increase of 0.49 Bcf/d, while Canadian net imports increased 0.20 Bcf/d.

- Res/Com demand decreased 0.16 Bcf/d on the week, while the power demand sector increased by 1.46 Bcf/d. Industrial demand was up slightly on the week, gaining 0.19 Bcf/d. LNG exports fell 1.78 Bcf/d due to maintenance at Sabine Pass, while Mexican exports gained 0.08 Bcf/d. These events left the totals for the week showing the market gaining 0.69 Bcf/d in total supply while total demand decreased by 0.21 Bcf/d.

- The storage report last week showed injections for the previous week at 55 Bcf. Total inventories are now 343 Bcf higher than at the same time last year and 111 Bcf below the five-year average. Current weather forecasts for the coming two weeks are indicating warmer temperatures from the Rocky Mountains to the East, which will enhance some late-summer demand.

- The next-two-week weather forecasts have a chance to support prices throughout this week, but additional tests of $2.00 are likely coming as the market remains in a historically bearish period and the opportunity for late-summer demand is nearing an end. Without late summer demand, ending storage inventories should be more than 3.6 Tcf.

- The CFTC report was released last week (dated August 6) and provides little indication of any shift in the speculator’s directional bias. The Managed Money short position increased exposure by adding 2,149 contracts, while the long position increased by 4,144 contracts. Last week’s low range trade between $2.029 and $2.155 gave no indication of a directional change in the speculative trade.

- Market internals maintained the bearish bias on the week, as volume was higher than that of the previous week. Total open interest also gained week over week, according to preliminary data from the CME.

- The fundamentals will allow for some late-summer demand to support prices. However, with the summer season nearing an end, the possibility of extended heat is minimal, which will limit any price run. Expect another test of the $2.00 area either this week or later in the September contract’s life. Should prices break below $2.00, additional declines will push prices lower to support dating back to May ’16 of between $1.952 and $1.909. Any rally will run into selling at the July expiration at $2.29, up to the July expiration high of $2.324.

NATURAL GAS LIQUIDS

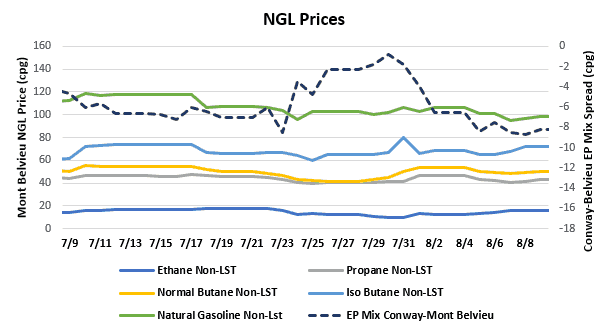

- NGL prices bounced around this week between the products. Ethane was up $0.037 to $0.150, propane down $0.014 to $0.421, normal butane up $0.001 to $0.493, isobutane down $0.009 to $0.685, and natural gasoline down $0.050 to $0.985.

- US propane stocks increased ~2.85 MBbl for the week ending August 2. Stocks now sit at 83.30 MMBbl, roughly 16.92 MMBbl and 15.67 MMBbl higher than the same weeks in 2018 and 2017, respectively.

- Targa last week reported the startup of its Grand Prix pipeline, which runs from the Permian in West Texas to Mont Belvieu. The pipeline has capacity of 300 MBbl/d out of the Permian and can be expanded to 500 MBbl/d. Targa reported in its 2Q2019 earnings release that Grand Prix is currently flowing 150 MBbl/d to 170 MBbl/d into Mont Belvieu, and flows are expected to increase through the remainder of 2019 as additional pipeline extensions are completed.

SHIPPING

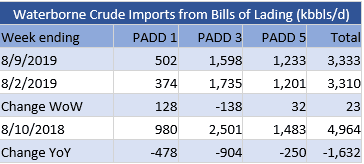

- US waterborne imports of crude oil rose slightly for the week ending August 9, according to Drillinginfo’s analysis of manifests from US Customs and Border Protection. As of August 12, aggregated data from the customs manifests suggested that overall waterborne imports rose by 23 MBbl/d from the previous week. PADD 1 imports rose by a little over 125 MBbl/d, and PADD 5 imports were up by more than 30 MBbl/d. Imports to PADD 3 fell by nearly 140 MBbl/d.

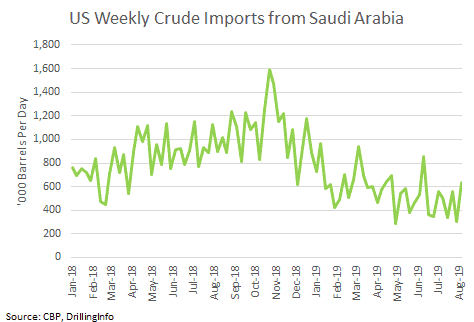

- Last week’s EIA weekly preliminary imports placed crude imports from Saudi Arabia at 277 MBbl/d. That is the lowest level since the EIA started reporting this level of granularity in 2010. Our customs manifests had imports from Saudi Arabia at nearly 303 MBbl/d for that week. One important driver of this was a lack of Saudi imports by Motiva Port Arthur. That refinery, owned by Saudi Aramco, is the biggest US refinery for Saudi crude. This week indicates we should see that number rise, with imports tallying roughly 638 MBbl/d for the week and imports returning to Motiva Port Arthur.