[contextly_auto_sidebar]

CRUDE OIL

- Crude oil futures started the week off on poor footing, with May WTI falling into unprecedented negative territory Monday, two days before contract rollover, and June WTI trading in the low teens that morning. The US Oil Fund, a large exchange-traded fund that invests in crude oil futures, announced that it would be exiting its long position in the June WTI contract because of “evolving market conditions.” While it is yet to be seen whether the June contract will come under the same pressures near expiry that the May contract did, the exit of a major speculative long position will certainly do a lot to take the wind out of the June contract’s sails. Other non-commercial market participants would be wise to follow suit, or at the very least not wait until a few days before expiry to roll their positions forward.

- Last week the Energy Information Administration reported an increase in commercial crude inventories totaling 15 MMbbl. Total gasoline stocks increased by 1 MMbbl and distillate stocks rose by 7.9 MMbbl. Total petroleum inventories rose by 25.5 MMbbl.

- The Commodity Futures Exchange Commission reported a net increase in managed-money long positions in NYMEX light crude oil futures. Long positions increased by 28,797 contracts to stand at 324,667 while short positions dropped by 23,326 contracts to stand at 77,189.

NATURAL GAS

- US Lower 48 dry natural gas production decreased 0.76 Bcf/d for week ending April 24 largely due to drops of 0.48 Bcf/d in the Mountain region and 0.28 Bcf/d in the South Central region, based on modeled flow data analyzed by Enverus. Net imports from Canada decreased 0.53 Bcf/d, with smaller volumes crossing the border into the northern Midcontinent and the Pacific Northwest. Res/Com, industrial and power demand saw decreases of 4.61 Bcf/d, 0.65 Bcf/d and 0.17 Bcf/d, respectively. LNG export demand decreased 0.51 Bcf/d due to decreases at Corpus Christi, Sabine Pass and Freeport, while exports to Mexico increased 0.28 Bcf/d. Weekly average totals show the market dropping 1.04 Bcf/d in total supply while total demand increased by 5.86 Bcf/d.

- The EIA storage report for the week that ended April 17 showed an injection of 43 Bcf. Total inventories now sit at 2.140 Tcf, which is 827 Bcf higher than at this time last year and 364 Bcf above the five-year average for this time of year. With the decrease in demand outpacing the decrease in supply, expect the EIA to report a stronger injection this week. The ICE Financial Weekly Index report currently predicts an injection of 74 Bcf for the week that ended April 24.

- Gas prices are struggling to find traction to get above $2.00/MMbtu. However, storage contracts are showing significant value for this time of year compared to recent years. A key way to determine the value of owning a storage option is to look at the October-to-January price spread, or the spread from the end of injection season to the peak of winter demand. A wider October-to-January spread indicates fear in the market that storage will fill to capacity, making storage option ownership more valuable. That fear made itself felt as the COVID-19 pandemic sent the markets into a whirlwind, and as of April 24 the October-to-January spread was sitting at $0.672/MMbtu after reaching as high as $0.742/MMbtu earlier in April. The last time this level of spread was seen this early in the year was 2012-2013, when the spread was $0.762/MMbtu; in comparison, in 2016-2017 it fell slightly lower at $0.665/MMbtu. The five-year average of the spread at this time of year is $0.377/MMbtu.

- While this wide spread incentivizes traders to put gas into storage and capture the large spread later during the winter, natural gas demand will still need to be met this summer. As producers shut in wells because of poor oil economics, natural gas production will also decline, meaning less gas available for injection over the summer. Despite the expected production decreases, storage inventories will be average to above average by the end of injection season. However, these inventories aren’t expected to be enough to overcome the supply drop, and natural gas prices will need to increase to incentivize production.

NATURAL GAS LIQUIDS

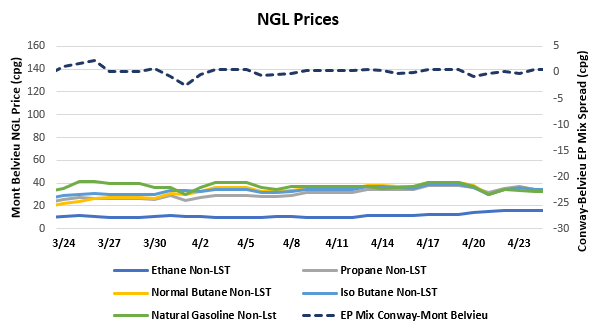

- C3+ liquids all saw declines in prices week over week: Propane fell $0.003/gallon to $0.349, normal butane fell $0.034/gallon to $0.347, isobutane fell $0.027/gallon to $0.341, and natural gasoline fell $0.038/gallon to $0.334. Ethane saw the only jump in pricing for the week, gaining $0.036/gallon to $0.153.

- The EIA reported a build in propane/propylene stocks (excluding propylene at terminals) for the week that ended April 17, showing inventories gaining 662,000 bbl. Stocks now stand at 57.44 MMbbl, which is 5.65 MMbbl higher than the same week in 2019 and 8.60 MMbbl higher than the five-year average for this time of year. The five-year average for next week’s report shows a build of 1.35 MMbbl, while the same week last year saw a build of 1.47 MMbbl.

SHIPPING

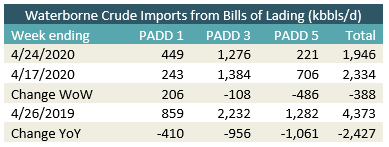

- US waterborne imports of crude oil fell last week, according to Enverus’ analysis of manifests from US Customs and Border Patrol. As of today, aggregated data from customs manifests suggested that overall waterborne imports fell by 388,000 bbl/d from the prior week. PADD 3 imports decreased by 108,000 bbl/d and PADD 5 imports decreased by 486,000 bbl/d. PADD 3 imports rose by 206,000 bbl/d. This represented the lowest overall level of imports since the week of Jan. 6, 2017.

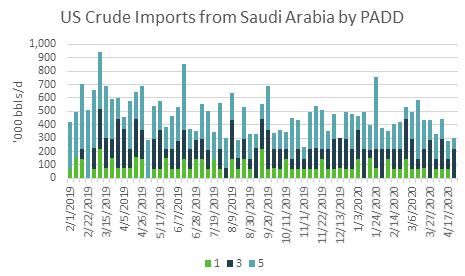

- Imports from Saudi Arabia rose last week with 218,000 bbl/d imported to PADD 3 and 86,000 bbl/d heading to PADD 5. Among these imports, Arab Light and Arab Medium were received by Motiva Port Arthur in PADD 3; Arab Light was received by Chevron Richmond in PADD 5.