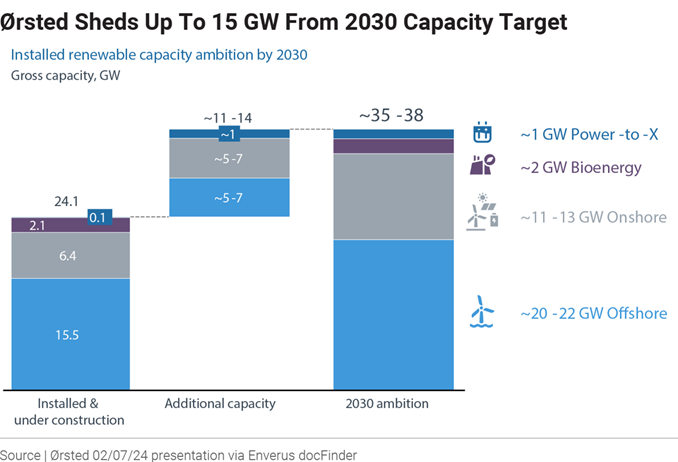

Ørsted took a blade to its project pipeline, reducing its ambition to 35-38 GW of installed capacity by 2030 from the previous 50 GW. The Danish renewables developer described the revamp as part of an effort to apply “learnings” from its November cancellation of two Ocean Wind projects offshore New Jersey, one of which cost it DKK 29.5 billion ($4.2 billion) in 2023 impairments and cancellation fees.

Project cancellations and the revised phasing of capex across the portfolio will result in Ørsted spending DKK 130 billion in capex during 2024-2026, a DKK 35 billion reduction. The overall capex plan through 2030 was cut by a third to DKK 270 billion.

The moves resulted from a comprehensive portfolio review in the wake of the Ocean Wind fiasco. CEO Mads Nipper detailed the many lessons from the project during Ørsted’s Feb. 7 earnings call.

The Ocean Wind 1 and 2 projects lacked inflation indexing, and the “immature” U.S. market exacerbated capex inflation, he said. Despite these warning signs, Ørsted committed significant capital into the projects before an official FID to keep on track for the company’s construction timeline, which had first power being delivered in late 2024 or early 2025, Nipper said. Amid a lack of qualified labor, suppliers struggled to ramp up and missed commitments. Ørsted was unable to come up with backup suppliers in time for a 2025 installation.

There were “a couple of local construction permits that turned out to be more challenging and a bigger risk for the project than assumed. And we also had a further delay on the air permit for the project, which again posed additional uncertainty,” Nipper said.

Vows to be more careful investing capex on pre-FID projects like Ocean Wind.

In addition to insisting on inflation protection in offtake agreements in future projects, Nipper said Ørsted will “further scrutinize and further limit the risks of those pre-FID commitments. Same thing, we want to have all critical local permits in place before we take FID and/or do capital commitments. And finally, we will clearly prioritize projects with a flexibility” to delay operations one or two years so there are more capex options. “That is even better for the offtaker of this power because it’s a lot better that a project gets built a year later than it doesn’t get built at all,” he added.

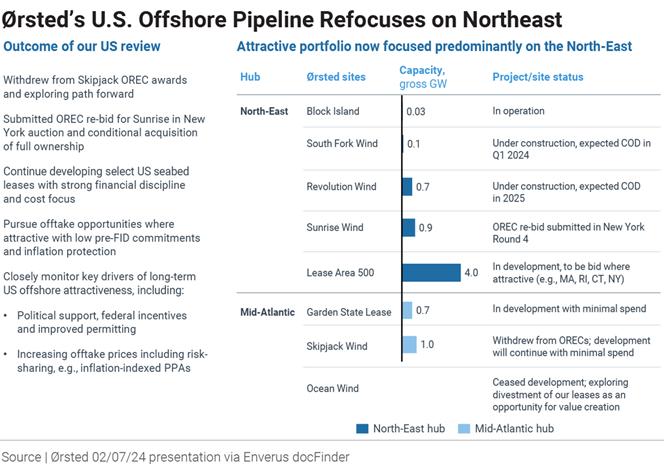

Among the projects that Ørsted kicked to the curb is 966 MW Skipjack Wind off Maryland. The company withdrew its offshore wind renewable energy certificate in late January because its terms no longer ensured an investable project, the company said. Ørsted will continue to advance development and permitting for Skipjack in hopes of a more favorable market, but at minimal spend.

Because Ocean Wind 1 was more advanced, that project accounted for DKK 19.9 billion of Ørsted’s DKK 26.8 billion in impairments and all the DKK 9.6 billion in cancellation fees. Between the Ocean Wind projects and Skipjack, Ørsted has removed 3.2 GW of potential capacity from its pipeline.

Despite all this, Ørsted doesn’t intend to completely eliminate offshore wind projects in the U.S. In addition to the two offshore wind projects already under construction – 700 MW Revolution off Connecticut and Rhode Island and 100 MW South Fork off New York – Ørsted still has the pre-FID 900 MW Sunrise Wind project off New York on its to-do list, albeit at rebid terms. The company also intends to participate in the New York 4 wind auction with up to 4.2 GW up for sale in new or rebid projects.

Ørsted is exiting several offshore markets, including Norway, Spain and Portugal, while remaining in their onshore markets, and is deprioritizing development off Japan. It also intends to slow spending on “power-to-X” systems, such as green hydrogen, and floating offshore wind because the market has been slow to develop those technologies. Ørsted also intends to accelerate drop-down divestments of projects and pursue new partnerships, looking to raise DKK 70-80 billion between 2024 and 2026.

Cost-cutting measures also include dividend pause, cutting 600-800 positions.

The company has set a target to reduce its fixed costs by DKK 1 billion by 2026 compared to 2023, on a like-for-like basis. This will include a reduction of 600-800 positions globally, with 250 leaving the company in the coming months. Ørsted also will not issue dividends following 2023, 2024 and 2025 results, with the intent of resuming them in 2026.

The project review and the impairments overshadowed a generally positive 2023 earnings report. Excluding the cancellation fees and DKK 4.2 billion contributed by new partnerships, EBITDA amounted to DKK 24.0 billion, above Ørsted’s guidance of DKK 20-23 billion. EBITDA from offshore sites more than doubled to DKK 20.2 billion in 2023 because of the ramp-up at Hornsea 2 off the U.K. and Greater Changhua 1 and 2a off Taiwan.

Ørsted also announced that chairman Thomas Thune Andersen will step down at the annual general meeting in March. This comes after CFO Daniel Lerup and COO Richard Hunter stepped down in November.

This story was published in the latest edition of Energy Transition Pulse.

About Enverus Intelligence Publications

Enverus Intelligence Publications presents the news as it happens with impactful, concise articles, cutting through the clutter to deliver timely perspectives and insights on various topics from writers who provide deep context to the energy sector.