[contextly_auto_sidebar]

CRUDE OIL

- US crude oil inventories posted an increase of 3.1 MMBbl last week, according to the weekly EIA report. Gasoline and distillate inventories decreased 0.2 MMBbl and 2.4 MMBbl, respectively. Total petroleum inventories decreased 0.9 MMBbl. US crude oil production decreased 100 MBbl/d, per EIA, while crude oil imports were down 0.9 MMBbl/d, to an average of 6.3 MMBbl/d.

- Crude spent the week expanding the declines before finding some support from employment numbers on Friday. Earlier in the week, economic news signaling a potential weakening US economy pressured prices. With the partial ceasefire with the Houthi rebels in Yemen, the market diminished the geopolitical risks associated with attacks on the Saudi installations and production. This production is now back online, sooner than some had expected. This placed the majority of trade emphasis on the macroeconomic woes for global demand and the ongoing US–China trade war.

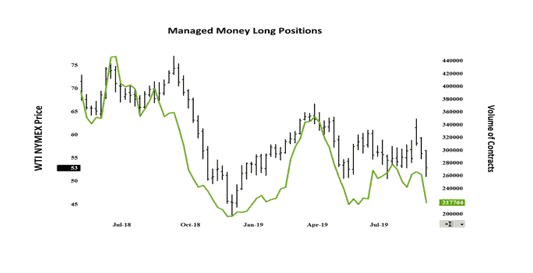

- The CFTC report released Friday (showing positions from October 1) showed a substantial shift in the expectations of speculative trade. The Managed Money long sector sold off 44,012 contracts, while the Managed Money short positions increased by 23,477 contracts. The two charts below show that these speculative expectations have remained in a comparatively tight range since the collapse in April.

- The Managed Money long positions had remained between 350,000 and 250,000 contracts until last week. The Managed Money short position has remained between 40,000 contracts and 90,000 contracts, and last week showed a substantive gain. The market has been trying to establish a directional bias but instead has developed a consolidation phase throughout the summer. These charts confirm a lack of directional bias needed by the speculative element for a breakout or breakdown from this consolidation.

- Market internals last week confirmed a negative bias as prices declined on higher volume and gains in open interest. The higher-volume days were Wednesday and Thursday, as prices broke below the levels when the attack on Saudi facilities occurred.

- The break below $53.00 signals the focus on trade is concentrated on the economic woes of the global economy and the lack of any development between the US and China in the tariff battle. A break below last week’s low at $50.99 opens the possibility of tests down to $50.00, which has held the market since early January. Rallies in price will be met with selling from $57.50, up to $59.00, as long as there aren’t any additional regional conflicts developing that counter the global economy narrative.

NATURAL GAS

- Natural gas dry production increased 0.36 Bcf/d last week while Canadian imports increased 0.22 Bcf/d.

- Res/Com demand increased 1.95 Bcf/d while power demand increased 0.02 Bcf/d, as the first cooler weather of the season made it into the Lower 48. Industrial demand gained 0.17 Bcf/d. LNG exports were flat on the week, while Mexican exports increased slightly, gaining 0.03 Bcf/d.

- These events left the totals for the week showing the market gaining 0.58 Bcf/d in total supply while total demand increased by 2.24 Bcf/d.

- The storage report last week showed the injections for the previous week at 112 Bcf. Total inventories are now 465 Bcf higher than last year and 18 Bcf below the five-year average. It could be an early indication of future prices that the market rallied on what was widely viewed as a bearish report. The NOAA’s current weather forecasts for the near term (coming week) have a cooling change to the central US, while the 8-to-14-day forecast has the cooling limited to North Dakota and Montana.

- The CFTC report released last week (dated October 1) showed the Managed Money long positions selling 20,909 contracts, while the Managed Money short position added 24,601 contracts. This activity suggests that speculative traders were expecting further declines on the storage release. With the price rally after the storage release, the CFTC report should provide additional shifts in the report published later this week.

- With the price rebound off the test of $2.207, the market internals changed slightly to a more neutral-to-bullish bias, as volume increased (especially at the end of the week) and open interest showed gains.

- While the internals may support additional increases this week, the weakness at the close on Friday signals the potential for additional declines early this week. Look for buying at the $2.20 area, while rallies will find selling at $2.40 up to $2.44.

NATURAL GAS LIQUIDS

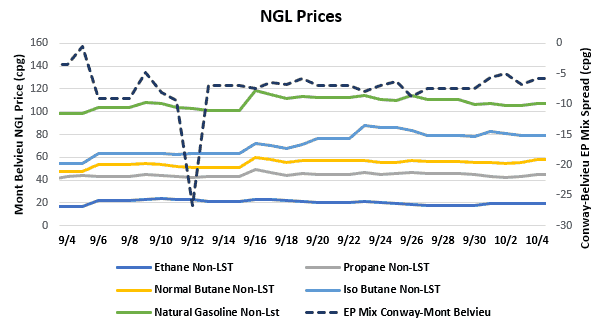

- Prices were down across the board last week. Ethane was down $0.002 to $0.191, propane was down $0.021 to $0.439, normal butane was down $0.006 to $0.557, isobutane was down $0.046 to $0.801, and natural gasoline was down $0.057 to $1.063.

- US propane stocks gained ~971 MBbl for the week ending September 27. Stocks now sit at 100.64 MMBbl, roughly 21.92 MMBbl and 22.64 MMBbl higher than the same week in 2018 and 2017, respectively.

SHIPPING

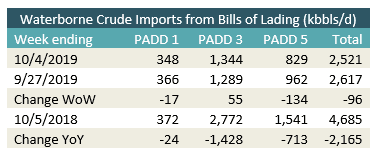

- US waterborne imports of crude oil fell for the week ending October 4, 2019, according to Enverus’s analysis of manifests from US Customs & Border Patrol. As of October 7, aggregated data from customs manifests suggested that overall waterborne imports decreased by 96 MBbls/d from the previous week. The drop was driven by declining imports in PADD 1 and PADD 5. PADD 1 waterborne crude imports fell by more than 15 MBbls/d, while the drop for PADD 5 was nearly 135 MBbls/d. PADD 3 imports increased slightly, up by 55 MBbls/d.

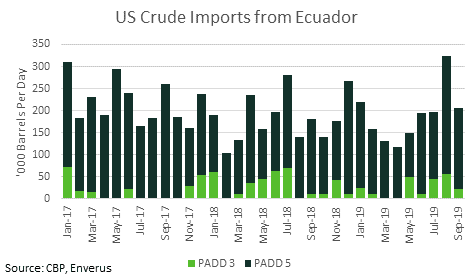

- Last week, Ecuador announced that it would quit OPEC effective January 1, 2020, as it seeks an increase in revenue from selling its crude. According to our data collected from US customs manifests, imports of Ecuadorian crude to the US reached nearly 325 MBbls/d in August before falling in September. That would be the highest since January 2016. Ecuador’s heavy sour grades Napo and Oriente have long been a main component of the crude diet for West Coast refineries like Chevron El Segundo and Marathon Carson, but in 2018 and 2019, Ecuadorian barrels have increasingly found their way to the Gulf Coast. On the Gulf Coast, those barrels are likely replacing lost Venezuelan barrels, with some of the biggest processors of the grades being Phillips 66 Lake Charles and Citgo Corpus Christi.