A plain-English guide to where capital is moving in global energy — and where it isn’t yet

A year ago, Enverus Intelligence® Research (EIR) argued global energy was being structurally repriced. In early 2026, that thesis stopped being theoretical. In a single thirty-day window: Israel and Iran moved into open military escalation, drone strikes hit Qatar’s Ras Laffan LNG complex, war-risk insurance collapsed in the Strait of Hormuz, and the IEA coordinated a 400-million-barrel reserve release. Oil pushed toward $90 to $100. Global LNG repriced sharply higher. U.S. shale did not bail out the market the way past cycles trained investors to expect.

In April 2026, the next layer showed up at the S&P Global Commodities conference: gas M&A is back but only for cash-flowing assets, hyperscalers are paying record premiums for nuclear, investors have replaced “baseload good, variable bad” with a strict IRR-and-contract lens, and cheap Permian gas is pulling oil and gas operators into the merchant power business.

Seven themes follow. Some are priced in. Several are not.

The popular trade — buy anything that produces power because AI needs it — was half right. Demand is real. But the ceiling sits inside the chip factory, not on the grid. Extreme ultraviolet (EUV) lithography tools (made only by ASML), advanced chip packaging (“CoWoS”), and high-bandwidth memory are all fully booked through the decade.

Updated estimates: roughly 10 gigawatts of global AI compute capacity in 2026 and 13 gigawatts in 2027, excluding China. ERCOT (Texas) is forecasting 15% annual load growth and PJM (Mid-Atlantic) 6% — both well above what chip supply and hyperscaler capex can support near-term. OpenAI and Oracle scrapped a 600-megawatt Stargate expansion. Google bought Intersect Power and relaunched it as IPX Power to build generation directly behind data centers. Hyperscalers have announced 40-plus gigawatts of “behind-the-meter” capacity — power built next to the customer rather than running through the public grid. The industry is calling it BYOG: Bring Your Own Generation.

WTI pushed toward $90 to $100. The IEA’s 400-million-barrel release (172 million from the U.S. over 120 days) did not cap it. U.S. rig count is responding, albeit cautiously. Total horizontal footage drilled was essentially flat, so far. Expected production growth appears less compared to equivalent prices in prior years. After years of consolidation, public producers’ shareholders reward capital discipline, not growth at any cost.

A surprising side effect: Permian gas is so cheap (Waha hub averaged minus $6.83/MMBtu the week of April 14, 2026) that producers are burning it on-site to generate electricity for ERCOT. Riley Permian and Conduit Power are deploying four sub-10-megawatt sites. Continental Resources and Mercuria announced a 452-megawatt project in Pecos County converting roughly 80 million cubic feet per day of associated gas into power.

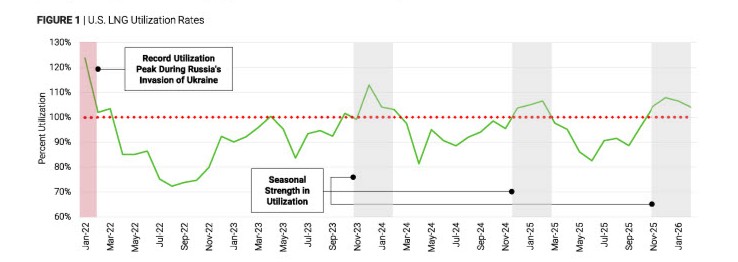

On March 2, 2026, QatarEnergy declared force majeure after strikes on Ras Laffan and Mesaieed. That single event removed roughly 10.2 billion cubic feet per day of natural gas from the global market — one of the largest single-source LNG disruptions in history. Unlike oil, LNG has no global cushion. U.S. terminals are already running near full capacity (peaked at roughly 122% of nameplate in January 2022, not sustainable indefinitely).

Capital is voting with its feet. TotalEnergies exited U.S. offshore wind and explicitly redirected the $930 million lease-fee refund into Rio Grande LNG (29 million tons per year) and U.S. oil and gas — citing European energy security and U.S. data-center demand.

Renewables are not retreating; the basis of competition has changed. AES Corporation is moving toward a $10.7 billion take-private. Cypress Creek acquired a 3.17-gigawatt solar-plus-storage portfolio in Arkansas. Zelestra broke ground on 441 megawatts of solar dedicated to Meta. RWE’s six-year U.S. plan added gas-fired generation.

Gas M&A is back, but only for cash-flowing assets. Blackstone’s recent Hill Top acquisition cleared at roughly $1.6 million per megawatt — versus $2 to $3 million per megawatt to build new — at an implied 12.2% weighted average cost of capital. When operating multiples push that close to new-build costs, greenfield economics start working again. Across the five publicly-traded independent power producers (IPPs), valuations are dispersed: durable contracts are rewarded, exposure to capital cost inflation and regulatory risk is discounted.

Average wait from queue entry to commercial operation now exceeds 2,100 days — up roughly 60% since 2017 — and only about 10% of queued capacity actually gets built. GE Vernova and Siemens Energy hold a combined 125-gigawatt backlog, but more than half is non-binding slot reservations. The line for new H-class turbines stretches past 2029.

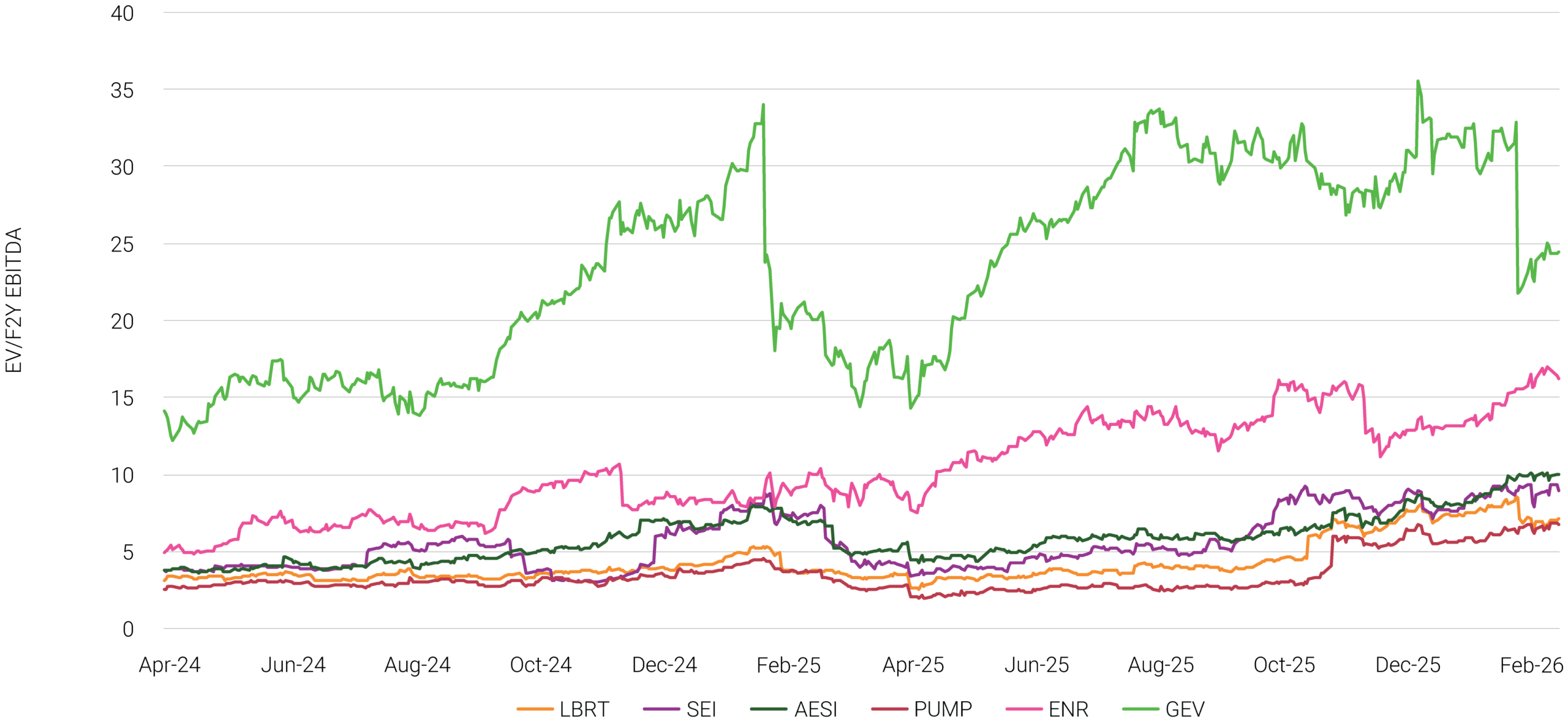

That has opened a window for distributed power: fuel cells (fastest, with a price premium), aggregated reciprocating engines (best near-term economics), and aero-derivative gas turbines (10-to-15-year contracts). Oilfield services companies — Liberty Energy, Solaris, VoltaGrid — could meet roughly 25% of behind-the-meter data center load growth. Power-exposed OFS trades around 6× forward EV/EBITDA; turbine OEMs trade closer to 17×. Our view: as long-term contracts become a bigger share of OFS revenue, the multiple should re-rate toward 8–10×.

Utilities are getting in too. AEP’s deal with Bloom Energy structures up to 1 gigawatt of fuel cell capacity through an unregulated subsidiary, earning private-equity-style 12–15% returns instead of the regulated 9–10%. Virginia, Texas, and Georgia utilities are studying the model.

Through 10-to-15-year power purchase agreements, hyperscalers are locking in stable, carbon-free electricity and sidestepping gas price volatility. Recent deals priced by EIR: Susquehanna at roughly $65/MWh, Comanche Peak at $90, Crane Clean Energy Center at $101. Across the six disclosed agreements, the uplift over forward power prices runs $22 to $49/MWh, averaging $34. That premium has expanded roughly 73% since March 2024 and is still widening. For utilities and IPPs with existing nuclear capacity, this is a pricing event, not just a demand event.

March 2026 — the Iran war, roughly 20 vessels attacked in Hormuz, Borr Drilling halting four jackups, SLB evacuating personnel, Qatari LNG force majeure. Geopolitical risk related to oil and product stocks seem underpriced relative to history, while global LNG has shifted to coal with no immediate comparable cushion. Three places markets still haven’t caught up: duration of disruption (assumes a quick Qatari restart), fragility of replacement supply (no global spare LNG, U.S. above-nameplate isn’t indefinite), and secondary effects (fuel switching, renegotiated offtake, coal-retirement reversals). North American oil and gas, secure, mapped, contractually mature, has a wider basin advantage than at any point in recent memory.

Oil and crude product inventory value the public market is uncertain to the ultimate draw.

Duration-of-disruption risk in LNG priced as if outages are short and replacements are easy.

IPP and developer dispersion — durable contracts and credible execution paths are being rewarded; the rest is being discounted.

Greenfield gas economics that quietly improve as operating multiples push toward new-build costs.

Power-equipment delivery speed — OFS-delivered distributed generation is mispriced relative to slow-delivery OEMs.

Nuclear pricing power, where the hyperscaler premium is still expanding.

Watch: Qatari restart timeline, Hormuz/OPEC+ resolution, EUV/CoWoS/HBM throughput vs. the 10–13 GW chip ceiling, U.S. rig and completion response at sustained higher prices, and each new hyperscaler nuclear or BTM deal as a pricing print.

Enverus Intelligence® | Research, Inc. (EIR) is a subsidiary of Enverus that publishes energy-sector research focused on the oil, natural gas, power and renewable industries. EIR publishes reports including asset and company valuations, resource assessments, technical evaluations, and macro-economic forecasts and helps make intelligent connections for energy industry participants, service companies, and capital providers worldwide. See additional disclosures here.

Let’s get started!

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Ready to Subscribe?

Ready to Get Started?