I became very familiar with the vagaries of initial potential (IP) test data reporting when I set a number of horizontal wells during the first wave of horizontal drilling in the Austin Chalk in the Dilley, Texas-area in the early ’90s.

We’d be drilling a hole and off in the distance I’d see a large plume of smoke coming from a location two miles away. In those days, the Austin Chalk was drilled underbalanced to encourage fluid flow into the wellbore since we were still 10 to 15 years away from large-scale hydraulic fracturing.

As is always the case in the manic phase of drilling booms, the best rumors about what was happening with all the surrounding operators were always circulating from the “experts” at the local coffee shop.

Operators were reporting IP rates of 2,000 to 3,000 BOPD. Promoters in the play were talking up these numbers as they sold their deals, and professionals who were familiar with chalk porosities of 7% to 8% and lower couldn’t help but wonder what was going on and where all that fracturing was located since they never had enough calcite-filled fracturing in their own drilling samples to imply that wells with high-flow rates could be tapping large fracture networks.

Once people began to dig into the data a bit and had a few beers with the local tool pushers, it all began to be a bit clearer. Essentially, operators would report an IP rate that reflected two or four or six hours of flow, shut it in before the well showed a water cut, and then gross the IP up to a “24-hour” test rate.

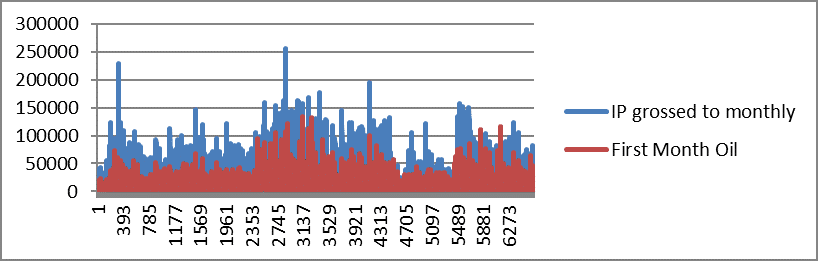

The chart below is from the Eagle Ford with first production dates from Nov. 10, 2014, to Nov. 10, 2019. Check out how IP rates overestimate the metric used in most operator PSA or 10Q statements for first-month oil & gas.

Not a big surprise, since wells that go on production are usually choked back to preserve reservoir pressure and proactively manage production operations.

Still, it’s a cautionary note to not accept IP volumes at face value as a way to differentiate good wells from average or poor wells.

Obviously, the goal is to be able to use early test and production information to gauge or assess the future value of production.

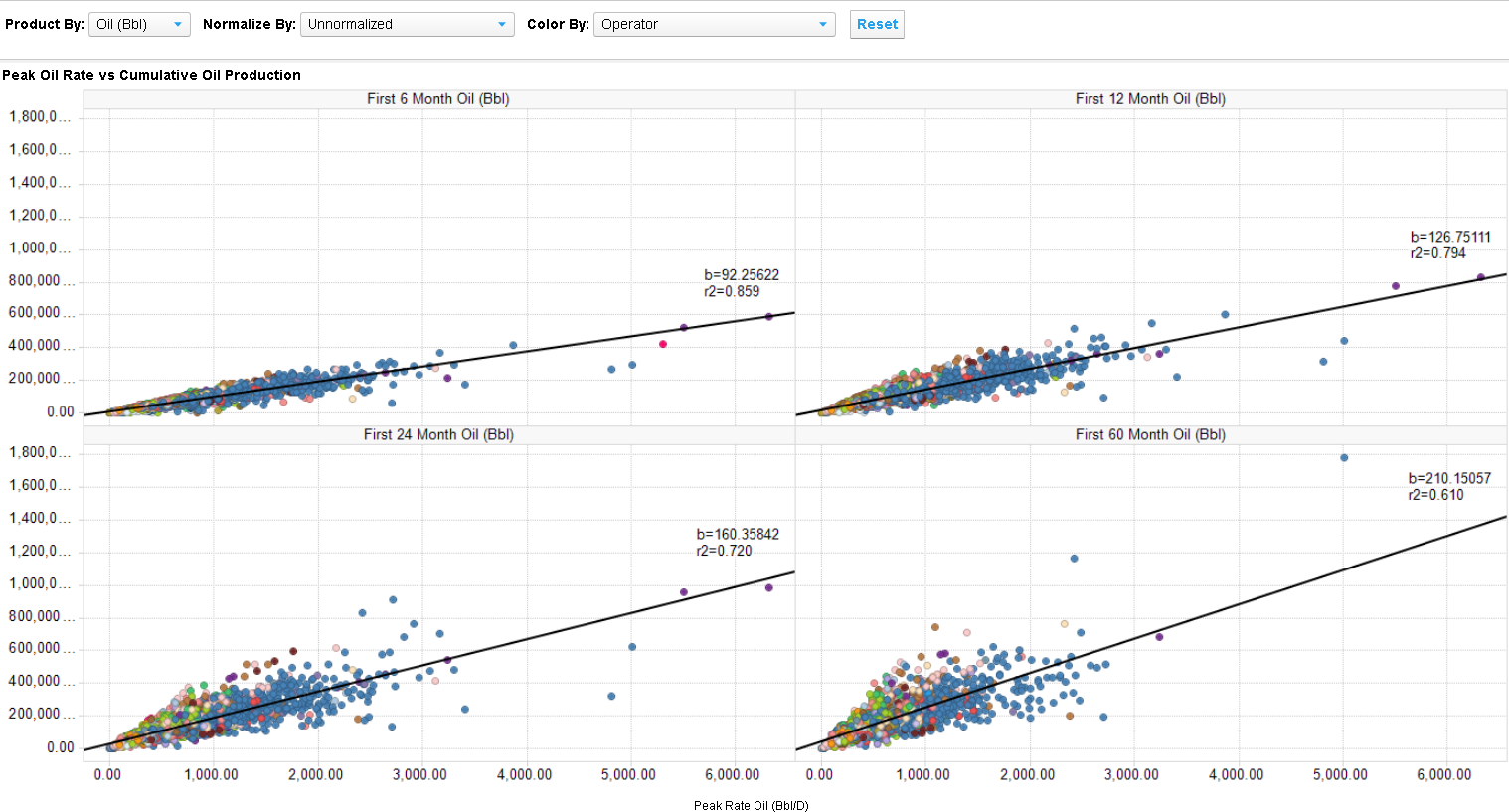

However, to get a sense of the embedded variances in time-gated cumulative production plots that occur for identical peak rate oil & gas values, look at the plots below of cumulative production versus peak rate oil, in the oily part of the Eagle Ford play (reservoir=Eagle Ford 1, Eagle Ford 2).

Note that six-month and 12-month cumulative oil production have pretty similar correlation coefficients and behaviors. Even so, there can be large excursions from the mean for similar peak oil rates.

For example, in the six-month graph, at a peak oil rate of nearly 1,500 BOPD, the cumulative oil production volume values range from 48,500 to 194,007 bbl. In the 12-month graph, at a peak rate of about 2,000 BOPD, the cumulative volumes of oil produced range from 149,000 to 352,000 bbl. The differentials can be even larger when looking at 24-month cumulative production volumes. At a 2,700 BOPD peak rate, the variance/spread is between a max of 910,000 bbl to a minimum of 132,000 bbl.

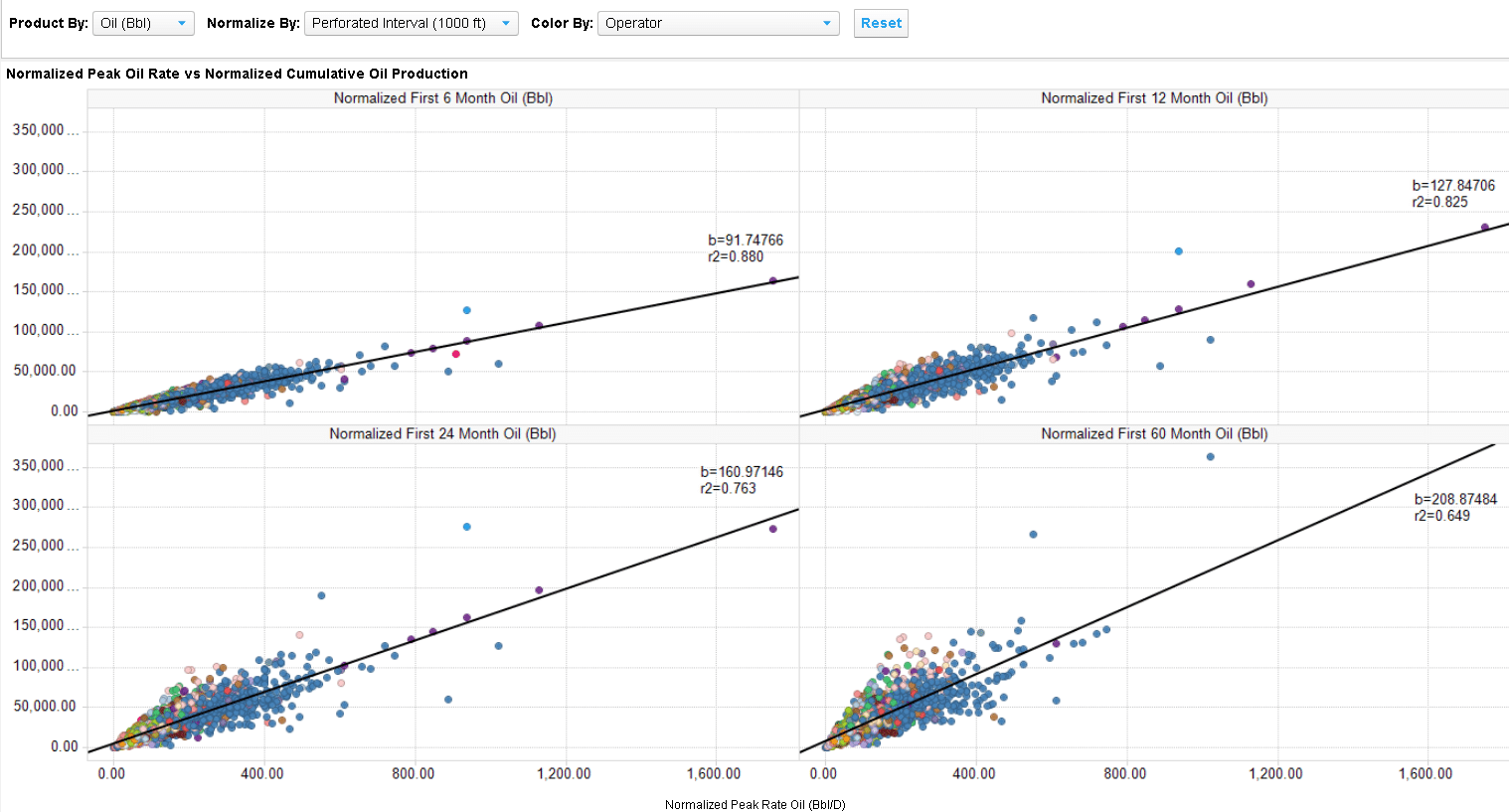

However, these cumulative production values are totally blind to differences in completion techniques. Let’s see what happens when we normalize by gross perforated interval.

Again, six-month and 12-month cumulative oil versus peak rate is reasonably well correlated, but we can see the same spread of 12-month maximum-minimum values—24,500 bbl to 62,000 bbl at a peak rate of approximately 300 BOPD, and 24-month oil maximum-minimum values of 30,000 to 106,000 at a peak rate of approximately 400 BOPD.

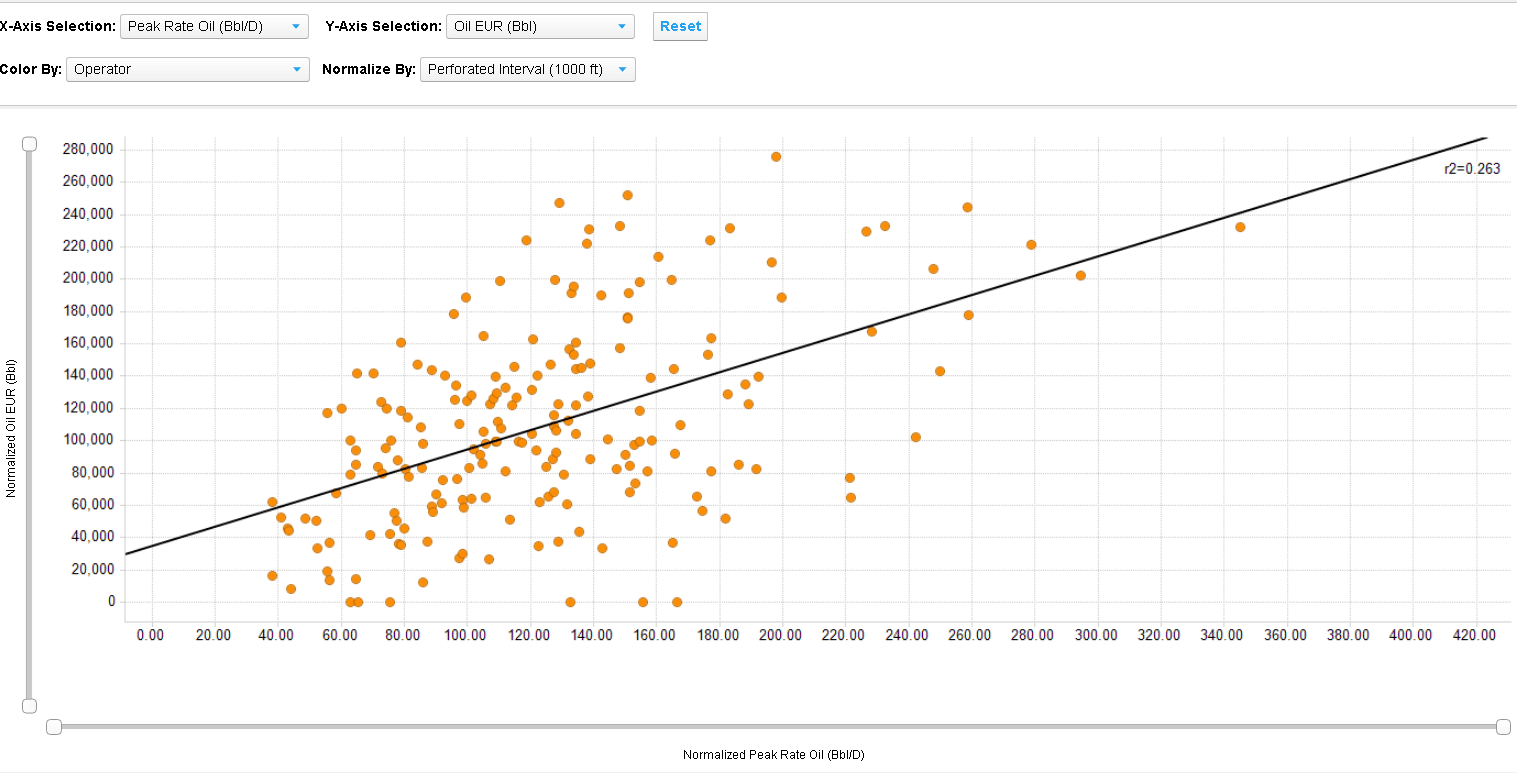

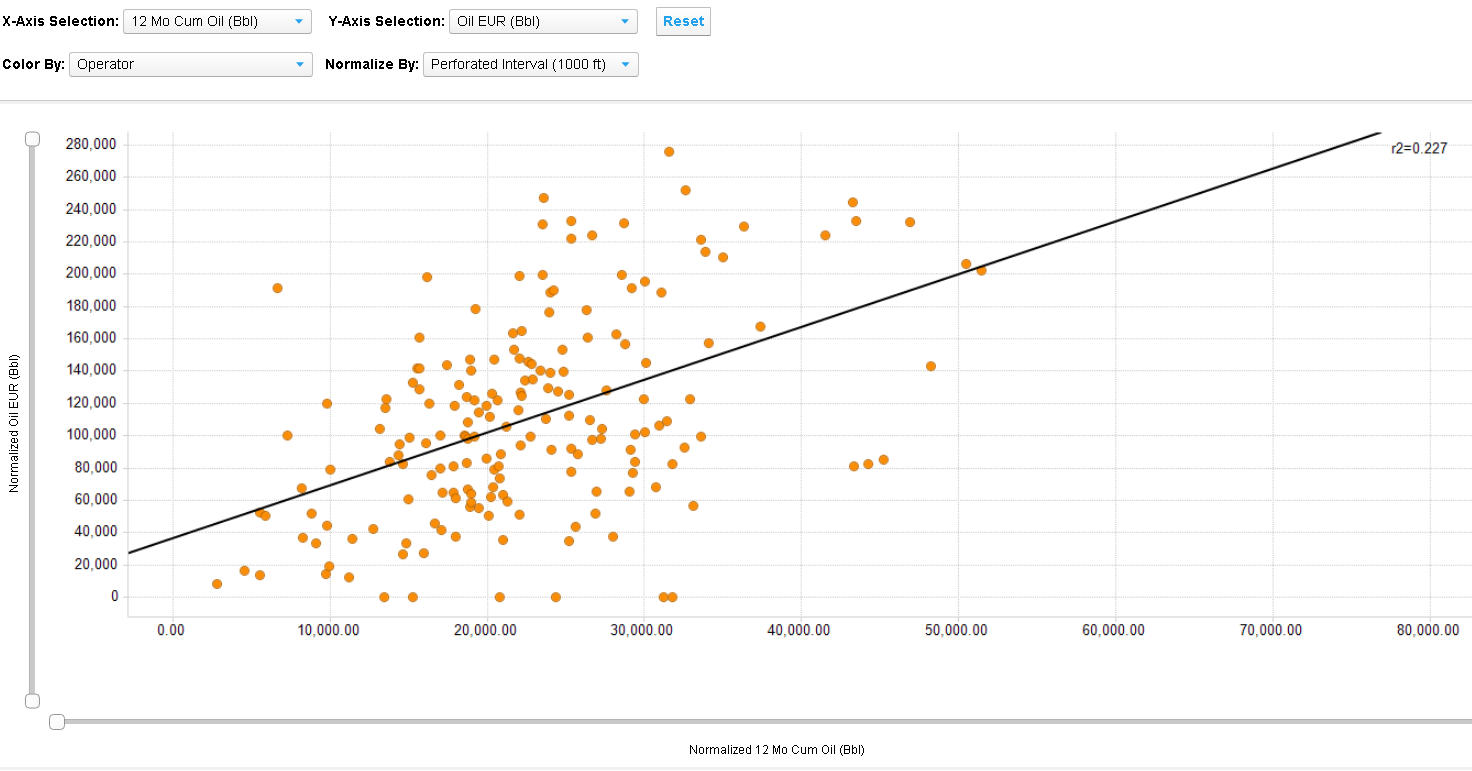

As peak oil rate increases, the predicted estimated ultimate recovery (EUR) values, even when normalized, show a very low correlation coefficient between peak rate oil and EUR, as seen in this graph for one well-known operator in the Delaware Basin.

Other well-known operators in the basin show correlation coefficients between EUR and peak rate ranging from .145 to .577, all of which imply low predictive value.

Even with the benefit of 12-month cumulative production values as a correlation factor, the same operator as shown above has a low correlation between 12-month normalized cumulative production and EUR.

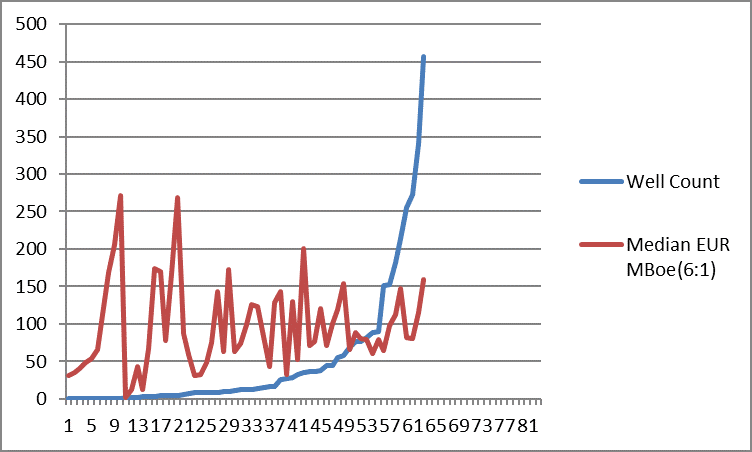

Tellingly, a large footprint of operated wells doesn’t necessarily translate into best-of-breed results, as shown in the graph below for operators producing in the Wolfcamp in the Delaware Basin.

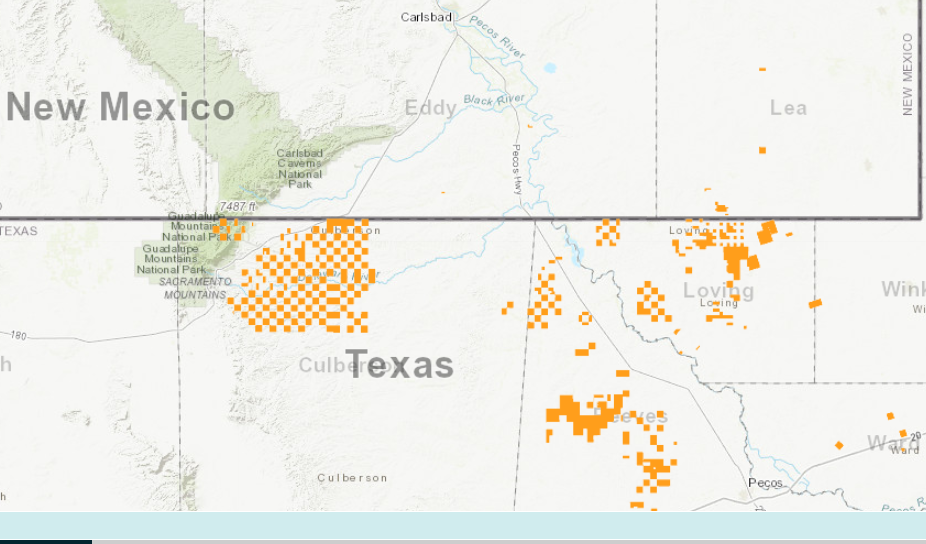

Of course, in basins with fragmented acreage positions like the Delaware, it’s very hard to normalize for geology, as this Enverus Drillinginfo LandTrac™ map of a different operator’s lease position implies.

Final message: it’s critical to look beyond IP and peak rate data to get a sense of how an operator’s total drilling inventory will add reserves to its bottom line.

Do you have any thoughts on early production metrics as predictors of reserve values? Shoot me an email at mark.nibbelink@enverus.com.

If you’d like to get more sophisticated insight into specific play productivities as analyzed in Enverus Basin Reports, contact businessdevelopment@enverus.com, or Tyler Krolczyk at tyler.krolczyk@enverus.com.