Rob McBride is the Sr. Director of Strategy and Analytics at Enverus. He previously managed natural gas trading at Hess and BNP Paribas, and served as the director of business development of energy markets products at Bloomberg LP.

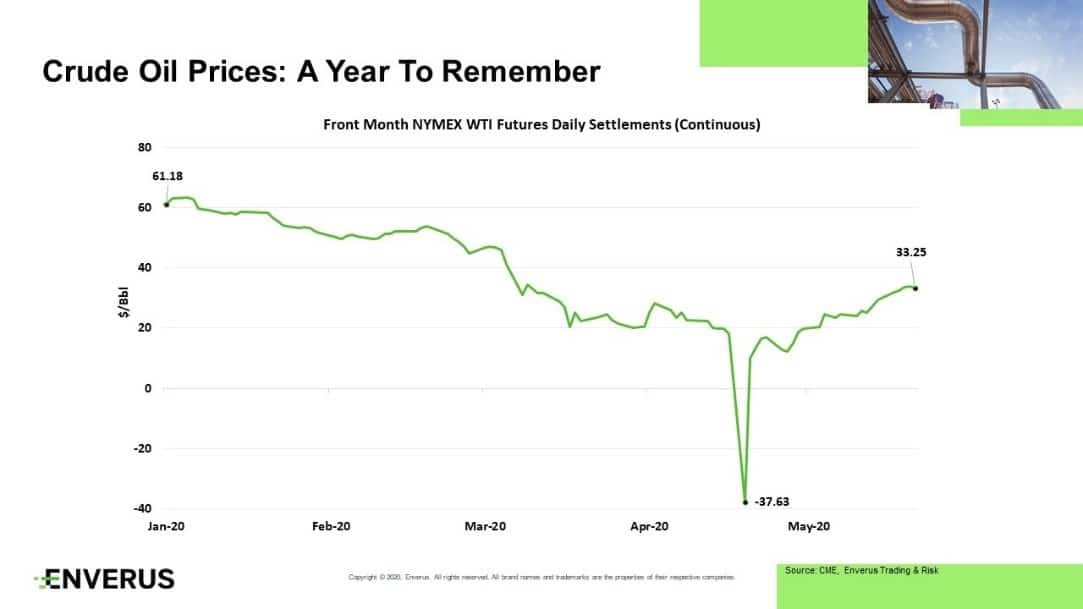

2020 has been quite a roller coaster ride—and it’s not even halfway over yet. To be sure, in recent weeks WTI crude reached a little bit of oil price stability compared to what we have been experiencing. But by no...

Recent commissioning activity on the Kinder Morgan’s new Gulf Coast Express (GCX) project led to a small increase in natural gas deliveries from producers in the Permian Basin. What does that signal for these producers over the short- and long-term?...